- Published on

Pinnacle @Duxton is an HDB project that was mooted by the late Lee Kuan Yew. It is located in downtown Singapore. Photo: Khalil Adis Consultancy

Ask any young Malaysians and chances are many are still unsure if they can buy their first home.

Their lack of knowledge, financial literacy, inability to get a loan and the lack of supply of such homes across Malaysia are further exacerbating the Malaysian housing issue.

From Johor to Kuala Lumpur, there is currently a demand-supply mismatch whereby most new launches in the market are priced above RM500,000.

This is far beyond what the average Malaysian can afford.

According to the first quarter of 2018 data from the National Property and Information Centre (NAPIC), Selangor has the highest number of existing stock of residential units followed by Johor and Kuala Lumpur at 1,516,960, 795,363 and 471,475 units respectively.

With Budget 2019 to be announced in November, perhaps the Malaysian government can take a cue from Singapore how the city-state is able to house 80 per cent of its population.

Step 1: Have a single affordable housing agency

The Singapore government's housing agency's The HDB Hub is located at Toa Payoh. Photo: Khalil Adis Consultancy

In comparison, in Malaysia, there are so many affordable housing programmes being rolled out by the state and federal governments such as Rumah Milik Mampu, Rumah Selangorku, PR1MA, My First Home, Program Perumaha Rakyat and the list goes on.

This confuses the public.

The government should consolidate the affordable housing segment under one single government agency much like the HDB model.

Recently, Zuraida Kamaruddin, the Minister of Housing and Local Government, was in Singapore to study the HDB model.

By having it under one government agency umbrella, this will enable the federal government to better gauge demand from the public.

This leads to the next point.

Step 2: Build demand-driven homes

Applicants who have successfully balloted for their flats are then invited to choose their units at the HDB Hub. Photo: Khalil Adis Consultancy

The public is then invited to apply for the various homes that are on offer in different parts of Singapore.

By doing so, this enables the HDB to gauge demand from the public and allocate homes using a balloting system.

The balloting system will then inform applicants of the status of their application.

If Malaysia were to follow such a system, this will help to solve the current demand-supply mismatch in the market and build homes according to demand.

Step 3: Introduce grants and subsidies

Singapore's Central Provident Fund (CPF) operates very much like Malaysia's EPF where there are various schemes for housing applicants to enjoy subsidies. Photo: Khalil Adis Consultancy

To qualify for the AHG, applicants must apply for a 2-room flat or larger with an income ceiling of S$5,000 per month,

Applicants must also be employed at the time of application and be at least in employment for the past one year during the housing application.

On top of that applicants must not be an owner of any other properties in Singapore or overseas.

Applicants can also qualify for additional grants under the SHG here or if they live close to their parents.

By introducing such grants, it lowers the entry price to buy a home.

Likewise, if similar grants are introduced in Malaysia, it will mean more Malaysians can afford to buy their first home.

You can read more about the scheme here:

Think about it.

Step 4: Introduce housing loans direct from the housing ministry

Singaporeans viewing the masterplan for an upcoming HDB township called Tengah. In Singapore, its citizens can get a housing loan direct from the HDB. Photo: Khalil Adis Consultancy

This means, regardless of the economy, the interest rate will remain the same unlike taking a bank loan.

In addition, the HDB is more compassionate if say, one is unable to service their loans.

The HDB will still require you to pay your monthly mortgage but will work out a plan that will ensure you will still have a roof over your head.

However, banks are less forgiving when you take a bank loan and will not hesitate to repossess your flat if you do not pay your mortgages on time.

In Malaysia, applicants must apply for a bank loan.

However, due to non-payment of PTPTN as well as bad credit, some applicants find their loans being rejected.

Perhaps, a way to get around it is to have a housing loan disbursed by the housing ministry with its own set of rules similar to the HDB.

Step 5: Introduce a rent-to-own scheme (for those who can't afford downpayment)

Ayer Holdings, formerly known as TAHPS Group, has introduced the ‘Stay & Own' scheme for their Epic Residence and Foreston projects to help first time home buyers. Photo: Khalil Adis Consultancy

For example, Ayer Holding introduced a ‘Stay & Own' scheme for their Epic Residence and Foreston projects whereby part of the rent will be converted to the downpayment.

This not only provides a temporary solution for those who urgently need a home but also a form of security

You can read more about the scheme here:

- Published on

By Khalil Adis

GSK Asia House headquarters for Asia located at 23 Rochester Park, Singapore. Photo: GSK Asia

“At GSK, we often ask ourselves, “do we have the right properties?” In Asia, it is all about growth. Asia is a huge piece of our future,” said Simon French, GSK’s Workplace and Design Director, Worldwide Real Estate and Facilities, United Kingdom.

French was speaking at the CoreNet Global Summit 2018 held in Singapore in March.

Titled Beyond the Horizon – The 2030 Workplace, GSK’s Asia headquarter office at Singapore’s research & development hub at one-north features intuitive workspaces that promote human interaction and collaboration while being culturally sensitive.

For example, its food offerrings at the premises are halal, keeping in mind the city-state’s multi-racial and multi-religious society. “Bacon & eggs won’t work in Singapore,” quips French.

The design process behind its GSK Asia House at Rochester Park in one-north involves looking at commercial drivers, behaviours & culture and design thinking

What results is an open office space spanning four floors of 14,330 sq m with plenty of natural light and ventilation.

In addition, it also has four layers of invisible security barriers before you get to see the actual work space.

Indeed, the ground floor is open to the public while the entire building is designed to bring in natural light.

“In Singapore, outdoor areas are under- utilised. We, therefore, have used the outdoor space in the western part of the building as

it affects employees’ behaviour - happy staff equals a more engaged people,” says French.

Commerce and value creators

GSK Asia House has been designed with plenty of light and natural ventilation. Photo: GSK Asia

GSK estimates that the Asia Pacific region will become its largest regional market by 2020. As such, greater emphasis has been placed on those who bring value or are generating revenue.

“We call this smart working where no leaders and directors have an office. It is about transparency, being able to see leaders and seeing them working. Constant sharing of ideas is relevant to the scientific industry,” explains French.

To make the workspace conducive to allowing open communication, seeing different perspectives and the exchanging of ideas, GSK Asia has created ‘neighbourhoods’ where there are no specific desks for anyone.

“There are no specific desks for anyone with fluid sitting areas and workspaces. This means you can work anywhere while promoting the exchange of ideas,” notes French.

Even the ground floor, which is not considered GSK’s working space, has created revenue.

“By having a concierge, we realised ownership of open space increases quickly. As such, Google is using the space and leasing from us,” reveals French.

GSK Asia features flexible, open spaces to encourage collaboration and the exchange of ideas. Photo: GSK Asia

“We are in the process of developing this whereby your laptop is recognised, and your presentation will automatically come out. In short, the building knows who you are,” he declares.

A record 740 corporate real estate professionals attended the CoreNet Global Summit 2018 which features more than 40 thought leaders shedding light on the critical relationship between an organisation’s productivity, bottom line, and effective CRE management.

The two-day summit revolved around nascent and current developments such as geopolitical shifts and technological disruption, which have complicated decision-making in many organisations across the Asia Pacific.

This story was first published by Asian Property Review in its July-August 2018 issue

- Published on

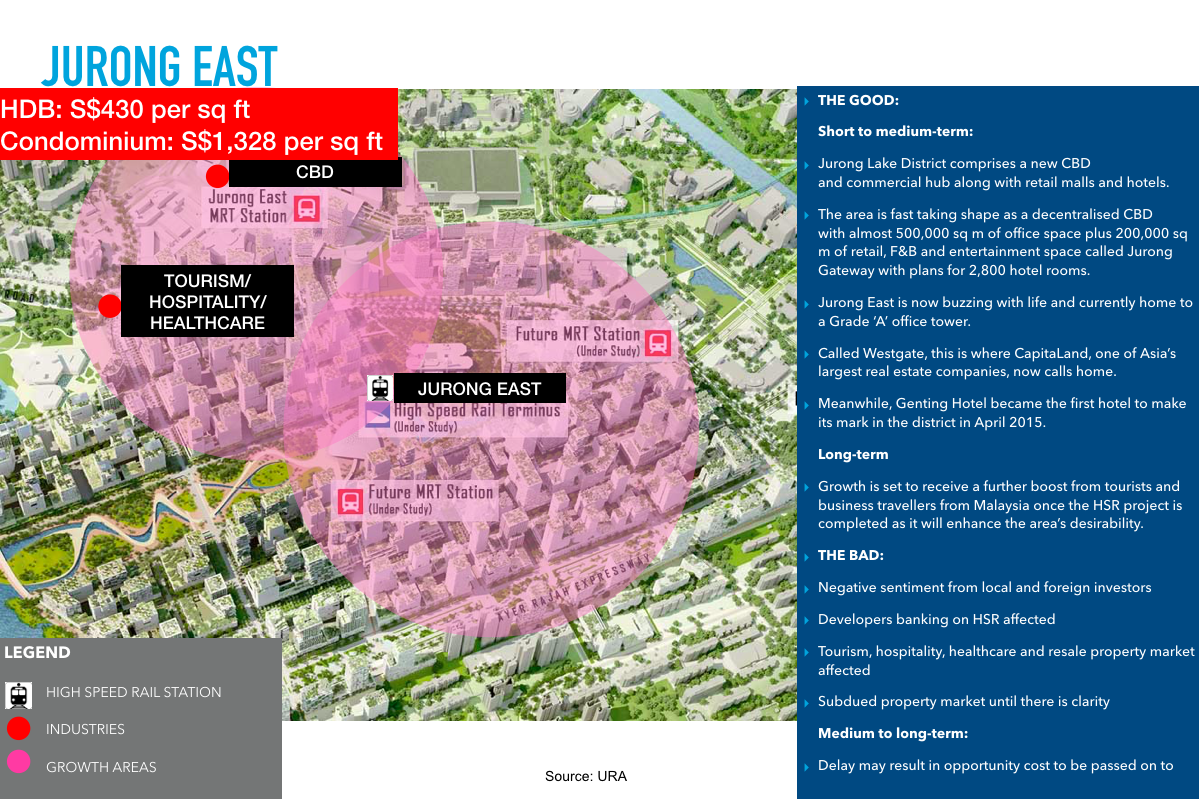

#1: Impact:

Infographic: Khalil Adis Consultancy

#2: Impact:

#3: Impact

#4: Impact

#5: Impact

#6: Impact

#7: Impact

#8: Impact

#9: Impact

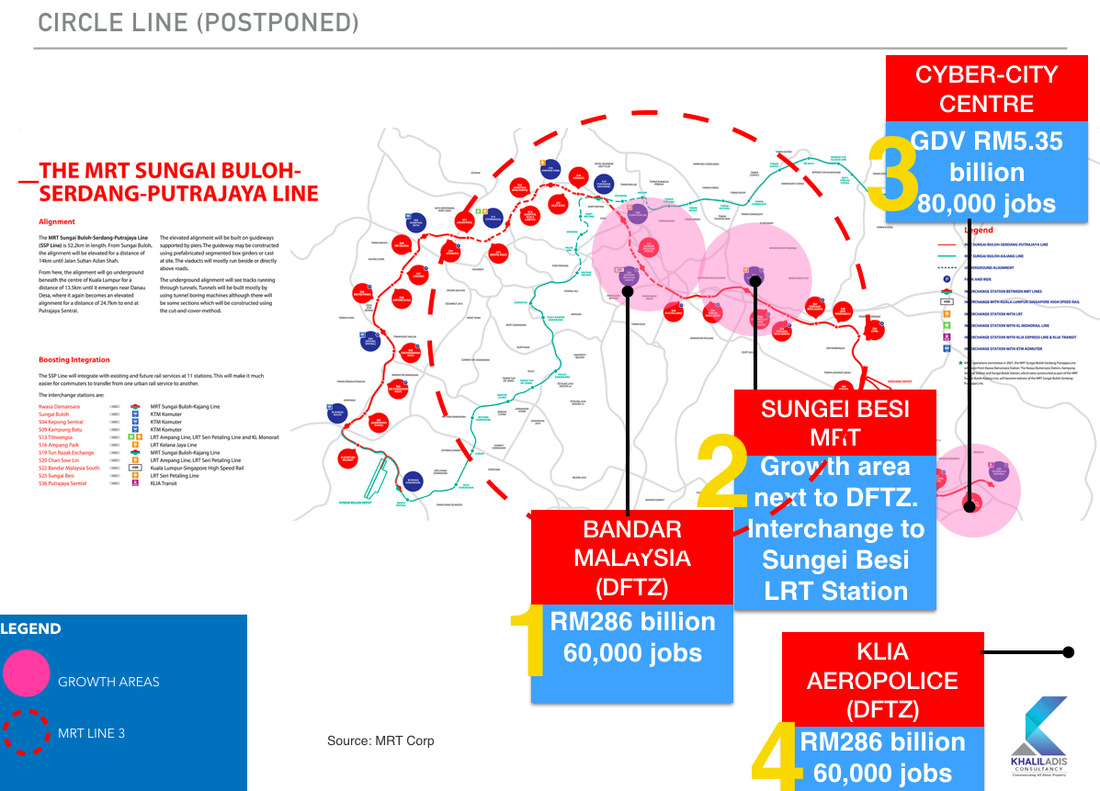

The impact for this postponement will be marginal as this MRT Line will still need to be constructed to connect the SBK Line and SSP Line.

We will most likely see speculators staying away from the market.

This presents good opportunity for genuine homebuyers to start looking in and around the station.

Homes in the secondary market will be the most ideal as they are priced cheaper than new launches.

- Published on

DUO, a joint-venture project between the Singapore and Malaysian government located in the Outside Central Region (OCR). Photo: Khalil Adis Consultancy

By Khalil Adis

The Urban Redevelopment Authority’s (URA) flash estimate of the price index for private residential property for the second quarter of 2018 showed that Singapore’s private property index has increased 4.9 points from 144.1 points in the first quarter 2018 to 149.0 points in the second quarter.

This represents an increase of 3.4 per cent, compared to the 3.9 per cent increase in the previous quarter.

URA’a data showed that private properties in the Rest of Central Region (RCR) increased the most in Singapore - by 5.7 per cent, after registering an increase of 1.2 per cent in the previous quarter.

Meanwhile, those in the Core Central Region (CCR) increased by 1.4 per cent compared to the 5.5 per cent increase while those in the Outside Central Region (OCR) increased by 2.9 per cent after registering a 5.6 per cent increase in the previous quarter respectively.

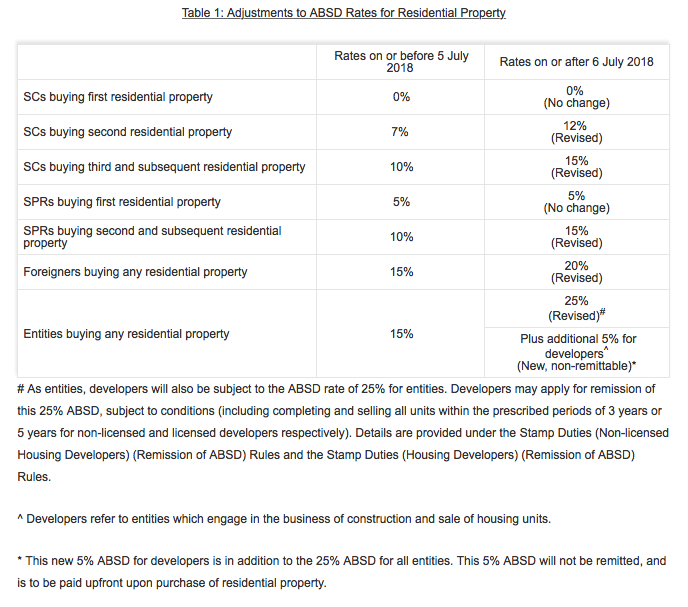

The Monetary Authority of Singapore (MAS) in a statement said the adjustments to the Additional Buyer’s Stamp Duty (ABSD) rates and Loan-to-Value (LTV) limits on residential property purchases were needed “to cool the property market and keep price increases in line with economic fundamentals.”

Additional, MAS said private residential prices have increased sharply by 9.1 per cent over the past year after declining gradually for close to four years.

See table below for the summary:

#1: First time Singaporean private home buyers can heave a sigh of relief

The ABSD measures are aimed at second and multiple property owners to ensure they do not engage in excessive speculation which may bring property prices to unsustainable levels.

Therefore, first time private home buyers will not be penalised as they are deemed as genuine homeowners.

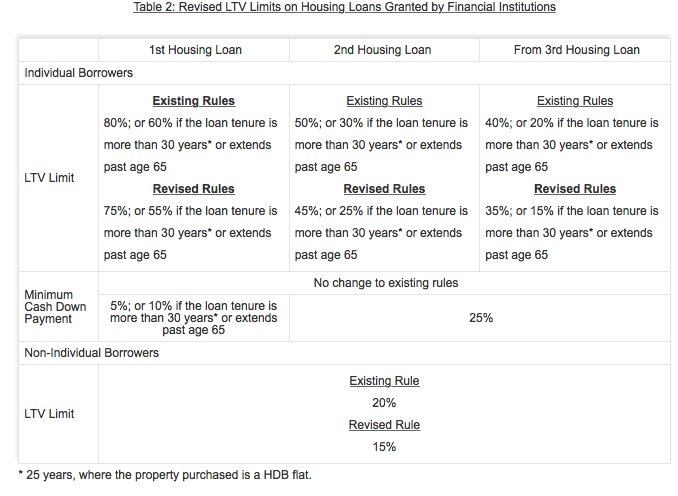

#2: However, bank loan margins for first-timers has been decreased

Be prepared to cough up more cash upfront.

The loan-to-value limit has been decreased from 80 per cent or 60 per cent if the loan tenure is more than 30 years or extends to more than age 65 to 75 per cent or 55 per cent if the loan tenure is more than 30 years or extends to more than age 65.

This means you will need to pay 5 per cent in cash upfront if your loan tenure is 30 years or 10 per cent if it extends to more than age 65. While the remaining will need to be paid in cash and/or CPF.

#3: Be prepared to pay an additional 5 per cent ABSD for second and/or subsequent properties for Singaporeans

ABSD rate for second property has been increased from 7 to 12 per cent.

Meanwhile, the ABSD rate for third and subsequent properties has been increased from 10 to 15 per cent.

#4: Lower LTV ratio for a second property

The loan-to-value limit has been decreased from 50 per cent or 30 per cent if the loan tenure is more than 30 years or extends to more than age 65 to 45 per cent or 25 per cent if the loan tenure is more than 30 years or extends to more than age 65.

The minimum cash downpayment is now 25 per cent.

#5: More cash upfront makes buying in Iskandar Malaysia more attractive

You get more bang for your bucks investing in Iskandar Malaysia than in Singapore with the new ABSD rates.

Assuming you are buying a second property for your own occupation, that 25 per cent cash downpayment for an S$1 million condominium translates to S$250,000 which could easily buy you a freehold landed or condominium development across the causeway.

With a minimum purchase price of RM1 million and a 70 per cent loan margin, you might as well convert it to your RM300,000 downpayment, not including stamp duty, state levy, legal fees and so on.

The downside is you will have to make to with the daily commute and traffic congestions until the Johor-Singapore Rapid Transit System (RTS) is ready in 2024.

- Published on

Aerial view of an HDB estate in Singapore. Photo: Khalil Adis Consultancy

In Singapore where 80 per cent of the population lives in government- owned flats, (popularly known as Housing & Development Board or HDB flats), losing the roof over your head is really a big deal.

Being government-owned, there are strict laws and regulations in place governing HDB flats. They include a minimum occupation period (MOP) of five years and a minimum rental period of six months per application when renting out your HDB flats.

According to the Housing & Development Board, this is necessary “as it may disrupt the living environment and pose security concerns for our residents”.

Take the example of two home owners whose flats were seized in 2014 for illegally renting them out to tourists. In both cases, the two owners had openly flouted HDB laws by renting them out on a daily basis.

While there is no latest data as of 2018, the numbers could be higher due to the popularity of AirBnb listings. Between January 2012 to 2014, for instance, the HDB had seized 202 flats for breaking the law.

So what can lead to such confiscations? Here are some of the common scenarios:

#1: You illegally rent out your property

Every HDB flat has a MOP of five years. us, you are not allowed to rent out your flat if you have not reached the MOP.

#2: You rent out for a short-term period

AirBnb type of accommodations are not allowed in HDB flats as the minimum rental period for each tenant must be 6 months per application. us, flat owners are not allowed to rent out their flats or bedrooms on a short-term basis.

#3: You did not register with the HDB after renting out your flat

Granted, you have fulfilled the MOP, it is still against the law if you do not register the particulars of your tenants with the HDB.

#4: Your tenants are involved in illegal activities

Illicit businesses like prostitution in the heartlands have become rife and a common problem nowadays. While the tenants are the ones breaking the law, the onus is on the owners to do regular spotchecks to make sure your tenants are not involved in such illegal businesses as this may affect the harmony of your neighbourhood.

#5: You bought a private property before the minimum occupation period is up

Owning a HDB flat is a privilege and not a right. By buying a private property in Singapore or overseas, before the minimum occupation period is up, you are essentially denying a more deserving Singaporean a roof over their head.

#6: You have not been paying your mortgage

This is a last minute resort if you have persistently not been clearing your arrears despite HDB’s best intentions. In this case, the HDB has the right to confiscate your flat. However, such households will be given alternative accommodation such as downsizing to a flat that they can afford or renting a flat directly with the HDB.

With the exception of the last scenario, losing your HDB flat can have very grave implications. Let’s take a look at them:

Implication No: 1: Financial losses

Assuming you had broken the laws, the HDB has the right to take back your flat at the price that it was purchased after deducting a penalty.

While the HDB does not leave you financially destitute, this also means you will not be able to enjoy the capital appreciation on your flat.

Let’s take the case of a property agent, Poh Boon Kay whose HDB flat was repossessed by the HDB in 2010 after he and his wife was found to have illegally sublet his home.

While they both had bought the HDB flat from the open market at S$150,000, he was reportedly paid S$125,000 after deducting the penalties. At the time of the confiscation, his flat was worth S$320,000. That’s almost a loss of S$200,000!

Implication No: 2 No roof over your head

Unlike the last scenario, because you had broken the law, you’re on your own. This not only creates a huge fiinancial burden as you will now have to either rent or buy a private property, but also deal with the emotional stress and uncertainty of not having a roof over your head.

Takeaways

While HDB is an asset, it can also lead to huge financial losses if you break the law. The takeaway is this, it is always better to err on the side of caution when it comes to government-owned flats in Singapore as the repercussions far outweigh one’s ignorance and financial greed.

This article was first published by Asian Property Review, March-April 2018 issue