- Published on

By Khalil Adis

Wat Arun at dusk. Photo: Khalil Adis Consultancy.

However, beyond the familiar narrative of affordable shopping, street food, floating markets and Chatuchak Weekend Market, the city is quietly building something more substantial.

During my recent trip to Bangkok as part of my '18 Years On The Ground' series, I sat down with two people who know this city from the inside, Dr. Ploylada Thanapaisanvorakul, dermatologist and founder of Lollana Clinic, and Kanchana Paha, former Associate Editor of Property Report and former Head of Consumer Marketing at DDProperty Thailand.

What they told me cuts through the marketing narrative and gets straight to what's actually happening on the ground.

Medical tourism is no longer just about hospitals

Aerial view of Sukhumvit. Photo: Khalil Adis Consultancy.

Yes, world-class hospitals like Bumrungrad, Bangkok Hospital and Samitivej have built international reputations over decades and continue to draw patients from across the region.

However, according to Paha, who has watched Bangkok evolve through multiple economic cycles, the story has moved well beyond the hospital campus.

"I started to realise that Bangkok has become a world-class medical tourism destination when it's not just about the hospitals anymore," she said.

What she's describing is an ecosystem.

Around Bangkok's major medical centres, a supporting economy has grown up with specialist clinics, recovery-focused serviced apartments, extended-stay accommodation, wellness facilities, F&B and retail catering specifically to patients and their accompanying family members who may stay for weeks at a time.

This ecosystem generates property demand that is distinct from conventional residential or commercial demand and shows up in specific districts rather than across the city uniformly.

Dr. Ploylada Thanapaisanvorakul sees this from inside the clinic.

With 17 years of experience building a regional clientele at Lollana Clinic, she has watched Bangkok's medical reputation evolve from a domestic healthcare story into a genuinely international one.

"Most people are still surprised at how advanced medical technologies are in Thailand," she said.

The surprise factor she identifies is significant.

Many Singaporeans still carry an outdated perception of Bangkok's medical capabilities, assuming that a lower price point reflects lower quality rather than lower overhead costs, different regulatory structures and a competitive private healthcare market that has invested heavily in technology and talent.

Dr. Thanapaisanvorakul's regional patient base, many of whom fly in from Singapore specifically, tells a different story.

The cost differential is real and significant

Screengrab of my interview with Dr. Ploylada Thanapaisanvorakul, dermatologist and founder of Lollana Clinic

Dr. Thanapaisanvorakul was direct about what the gap actually looks like.

"It's double the price to do Rejuran in Singapore than in Bangkok," she said.

For the uninitiated, Rejuran is a popular skin rejuvenation treatment with strong brand recognition among Singapore's professional demographic.

At double the Singapore price, the cost differential is enough to cover your flight, hotel stay and a few days in the city and still come out ahead.

When you factor in that the treatment is being performed in a clinic with 17 years of experience and an established regional patient base, the value proposition becomes clearer.

Dr. Thanapaisanvorakul's observation about cost connects directly to Paha's point about the broader ecosystem.

Patients who fly to Bangkok for treatments like Rejuran aren't just spending money at the clinic.

They're staying in serviced apartments, eating at restaurants, shopping at Nana Beauty Village and generating economic activity across multiple districts.

That aggregate demand is what makes medical tourism a property story, not just a healthcare one.

Medical tourism drives rental demand, not buying

Grande Centre Point Lumphini Bangkok, a luxury hotel in Bangkok near to many hospitals. Photo: Khalil Adis Consultancy.

"Medical tourism affects property demand through renting and hospitality rather than direct buying," she said.

This is the insight that most developer roadshows and investment seminars presenting Bangkok property to Singaporean audiences either miss or deliberately sidestep.

Medical tourists are temporary by nature.

The patient journey is weeks or months, not years.

The demand they generate is for short-term and extended-stay rental accommodation such as serviced apartments near major medical centres, recovery-focused hospitality, furnished units on flexible lease terms, rather than for ownership.

Investors approaching Bangkok's medical tourism corridor expecting direct buying demand from patients are likely to be disappointed.

The opportunity is real but it sits in rental yield and hospitality-adjacent assets rather than in residential ownership demand from medical visitors becoming permanent residents.

Paha was equally specific about where this demand shows up geographically.

"There are some areas that are shaped by it," she said, identifying districts that have physically emerged around Bangkok's medical tourism economy with their retail, accommodation and F&B all oriented around the patient recovery journey rather than conventional residential life.

The growth areas most investors haven't found yet

Wat Phra Sri Mahathat interchange station with the Pink MRT Line and BTS Sukhumvit Line. Photo: Khalil Adis Consultancy.

"Ram Intra and Fashion Island along the Pink MRT Line are growth areas," she said.

These are not names that appear in most developer roadshows targeting Singaporean investors.

They represent something different.

These are districts where the infrastructure story is still being priced into the market, with spillover impact on surrounding areas.

The Pink MRT Line, which opened in 2023, connects Nonthaburi to Minburi through Bangkok's northern corridor.

The infrastructure story is similar to how the RTS Link is reshaping property demand in Johor Bahru and how the Cross Island Line is repricing estates along its corridor in Singapore.

Infrastructure precedes demand.

Demand precedes price appreciation.

"The Pink Line is a growth area," Paha confirmed, expanding her observation beyond individual districts into a structural thesis about Bangkok's northern corridor as a whole.

Her framework comes from years of watching Bangkok's property market evolve.

"Thailand was a good classroom for me. Those experiences taught me that property is not just buildings. It is about timing, infrastructure, confidence and policy," she said.

Applied to the Pink Line corridor, the timing is now.

What this means for Singaporean investors

Traffic jam in Bangkok. Photo: Khalil Adis Consultancy.

Medical tourism is a genuine driver of property demand but through rental and hospitality rather than direct buying and in specific districts shaped by proximity to medical infrastructure rather than uniformly across the city.

The growth areas most worth watching are not the ones being marketed most aggressively to foreign investors.

They're the ones where the infrastructure has arrived and the market hasn't fully caught up yet.

The starting point for any serious engagement with Bangkok property is what Paha said to anyone considering the city whether for property, medical treatment or simply a new experience: "Come to Bangkok with curiosity, not with assumption."

Watch the full series here.

- Published on

By Khalil Adis

Anita Kapoor and I recently met up over a meal to talk about housing anxiety among Singaporean freelancers. Screengrab from our video interview.

A former journalist turned TV host, Anita radiates authenticity and that shines through every time she tells someone else's story in front of a camera.

But sitting across from me at Bangalore Cafe in Little India over thosai and masala tea, she had her own story to tell.

Twenty over years of friendship made it easy to skip the pleasantries and go straight to what really mattered - housing anxiety, especially as a freelancer in Singapore.

"Tara Barker gave me my very first opportunity to write for Women's Weekly. I was writing about interior decoration because I knew a little bit about it and I just kind of had a feel for it. And then one thing led to another and I started working in the industry," she said, on how she transitioned from print to on-camera work. (See the full interview in Part 1 here.)

From hosting acclaimed shows on Discovery, TLC and Channel NewsAsia, Anita became one of the region's most recognised faces.

For someone who knew her back in our writing days, attending the same press conferences together, she became, at least in my eyes, larger than life.

She built an incredible career as a freelancer, travelling the region and becoming one of Asia's most beloved TV hosts.

But despite that illustrious career, Anita was surprisingly candid about her struggles as a freelancer and her own home buying journey.

"In the good times, no," she said, when asked if she'd ever thought about getting a full-time job. "But when you're having bad times, or when you don't know where your next pay cheque is coming from — or, for example, when my mum got ill and I had to become a caregiver and think about somebody more than just myself, those are the times I thought, oh my god, I'm going to go get a regular job."

Anita's story echoes what a significant number of Singaporean freelancers such as content creators, independent consultants and gig workers can identify with.

What followed over the next two hours was one of the most candid conversations we've had so far.

Here are ten things Anita wants every Singaporean freelancer to know.

1. Housing anxiety is real but freelancers feel it differently (Part 2)

Anita Kapoor gets candid about her housing anxiety in Part 2. Screengrab from our video interview.

But unlike salaried employees, the anxiety hit Anita on three fronts at once - what she calls a "triple whammy": single, a freelancer and in her 50s.

"The anxiety was that I had sold my mum's flat. There's a certain amount of money that comes back, and I was thinking, should I buy a flat? Really only in my 50s, which is a very different situation. Single, 50 and wanting to buy a flat."

That anxiety only sharpens when it comes to applying for an HDB Flat Eligibility (HFE) letter, a system generally built around couples and families.

If you're single and freelance and reading this: the first thing Anita wants you to know is that you are not alone in feeling it.

See the full interview in Part 2 here.

2. Keep really good records of your invoices (Part 3)

Anita Kapoor shares how she created her own financial ecosystem in Part 3. Screengrab from our video interview.

"Keep really good records of your invoices. It's really a good idea to get the client to sign the invoice, or have a 'paid' stamp on it," said Anita.

Why does this matter?

Because your invoice records are the closest thing a freelancer has to a payslip.

When a bank or HDB assesses your income, they need to see that money came in consistently over a sustained period.

For a salaried employee, that evidence exists automatically through CPF statements and employer records.

For a freelancer, it only exists if you've created and maintained it yourself.

That means issuing proper invoices for every piece of work.

Keeping copies of every payment received.

Building a paper trail that tells the story of your income in a language financial institutions can actually read.

Most freelancers only find out how important this is when they're already in the middle of a loan application, scrambling to reconstruct records they should have been keeping for years.

Build your own system.

Start now, not when you're ready to buy.

Now.

See the full interview in Part 3 here.

3. "The hardest part was discovering how resistant I was to owning something" (Part 4)

Anita Kapoor gets candid as she shares her psychological resistance to owning a home. Screengrab from our video interview.

Why would someone be resistant to home ownership, especially in Singapore, where tenants are largely at the mercy of their landlords?

"When you have conversations with people, they're like, huh, you're resistant to owning it? I'm like, yeah, because I've rented for 20 years, and the freedom to just pick up and go was always there," she said.

Freelancers are wired for mobility.

The ability to pivot, to take the next project, to move toward the next opportunity without institutional constraint is part of what makes independent work sustainable and meaningful in the first place.

Home ownership can feel like the opposite of that.

"Home ownership in Singapore is a very big deal, because there are a lot of ways to live here. You can either live in an HDB or in private property, and the difference is several hundred thousand dollars. It just became a very practical thing. Okay, I've rented for many, many years. Is it time?" she asked.

What she wasn't prepared for was the psychological resistance to commitment, especially in a life built around professional flexibility and personal freedom.

With some money already sitting in her CPF Ordinary Account (OA) from the sale of the flat she had co-owned with her late mother and with rental rates climbing, Anita felt the time had finally come.

See the full interview in Part 4 here.

4. Applying for the HFE as a freelancer? OMG (Part 5)

Navigating the HDB Flat Eligibility (HFE) letter application was an arduous process for Anita Kapoor. Screengrab from our video interview.

"The terminology, figuring out that this site isn't really set up for my set of circumstances, and then trying to find out how to navigate it. What documents are needed. It's very different because you have to prove how your income came into being," said Anita.

For anyone thinking of buying an HDB flat, the HFE letter is the gateway document, whether you're going for a Built-To-Order (BTO) or resale flat.

For many, it's their very first rung on Singapore's property ladder.

For salaried employees, the application is relatively straightforward: payslips, automated CPF contributions pulled through Singpass and an employer letter.

The system is built around conventional employment.

Anita had to figure the whole process out on her own, which made it arduous.

She had to build a system from scratch, assemble documentation that doesn't exist automatically, and present her income in a format the system could actually assess.

Nobody had explained any of this to her beforehand.

She has since gotten her HFE approved.

But she still wishes someone had told her what to expect before she started.

See the full interview in Part 5 here.

5. Reserve your CPF before 55 (Part 6)

Did you know you can reserve your CPF OA before you turn 55? Anita Kapoor found that out when applying for her HFE letter. Screengrab from our video interview.

Most Singaporeans know CPF can be used toward housing.

Fewer know you can proactively reserve your CPF OA savings before age 55, specifically for your housing payment.

This is a step that's rarely explained proactively. Many buyers only discover it too late - after their OA savings have already been transferred to their Retirement Account.

At that point, they're paying in cash.

If you're under 55, planning to buy a home and intending to use your CPF OA, do your CPF reservation [at least two weeks before your 55th birthday here] .

The CPF system has more flexibility than most people realise.

See the full interview in Part 6 here.

6. Clean up your credit history at least three months before applying (Part 7)

Want to get your HFE approved? Anita Kapoor wise advice is to clean up your credit history at least 3 months before your application. Screengrab from our video interview.

Your credit rating determines whether HDB or the banks will lend you money for your home.

If you've got outstanding credit card bills or other instalments, it's worth cleaning up your credit history at least three months before applying for your HFE.

"If you've taken up a lot of loans before, if your credit card has a balance, you're going to see all of that, and it does affect your credibility," said Anita.

See the full interview in Part 7 here.

7. Show proof that you got paid (Part 8)

Want to get your HFE approved? Show proof that you got paid and get clients to sign your invoice advised Anita Kapoor. Screengrab from our video interview.

Three words that summarise the entire freelancer home loan application.

Not a payslip. Not an employer letter. Not a neat monthly CPF contribution.

Just proof that is self-assembled, self-organised, clearly presented.

One that showed that money came in and came in consistently enough to service a mortgage.

Anita's approach was to build her own financial system.

"If you issue invoices, and I know not everybody does, some people just get receipts depending on the type of freelance work, you need something that says, 'I got paid,'" said Anita.

It is a way of organising and presenting your income that tells its own story, in a format HDB and the banks can follow.

None of this is complicated.

But it requires an intentionality and discipline that most freelancers do not apply to their finances until they actually need to.

See the full interview in Part 8 here.

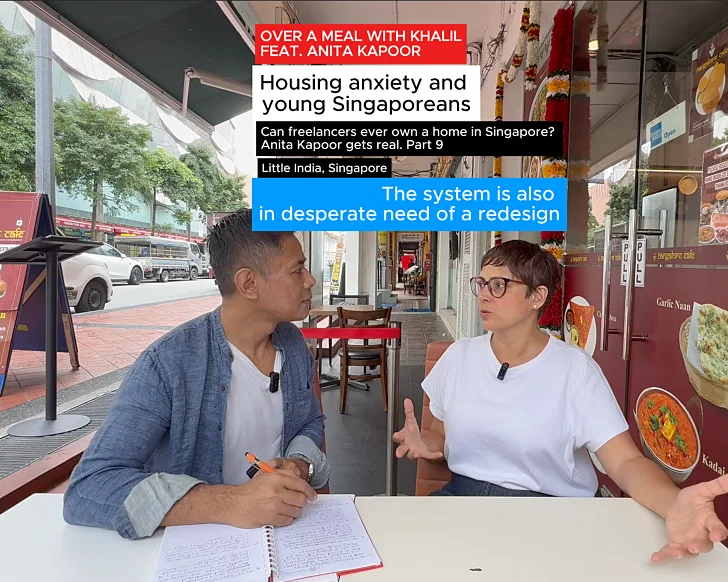

8. The HDB system is in desperate need of a redesign (Part 9)

Having gone through the HFE system, Anita opines that the system needs further refining. Screengrab from our video interview.

This is Anita's most significant observation and the one that goes beyond personal experience into something bigger.

Singapore's public housing system is one of the most celebrated in the world.

But let's face it, Singapore's workforce is changing.

The gig economy isn't a fringe phenomenon.

According to government data, more than one million Singaporeans are engaged in some form of freelance, self-employed or gig work.

The one-size-fits-all approach needs refining.

"We could increase the cap. The $7,000 could go up for basic BTOs, because there are many people who are self-employed or freelance and there are also many employed people whose first jobs pay them very, very well, but they're still living at home with their parents. So they can't get a basic HDB. They have to go straight to Prime or Plus, which is a lot to start with in your 20s or 30s," said Anita.

A system designed for the Singapore of 1980 is being navigated by the Singapore of 2026.

That gap is where housing anxiety lives for an entire generation of Singaporean freelancers.

See the full interview in Part 9 here.

9. Stop low-balling us (Part 10)

Know your worth, freelancers! That's one piece of advice Anita Kapoor has. Screengrab from our video interview.

That was Anita's answer to a question about whether covering other people's stories of struggle and resilience had shaped how she approaches her own financial and life decisions.

It wasn't the answer I expected.

But it was exactly right.

Two decades of interviewing people across the full spectrum of Singapore society, from the powerful and the vulnerable alike, had taught Anita something specific about her own worth: the market will pay you what you accept.

Your negotiation starts from wherever you position yourself.

Freelancers who undercharge aren't being humble.

They are being complicit in a systemic undervaluation of independent creative and professional work that compounds across an entire career.

Know what you're worth and charge accordingly.

Stop accepting less because the system makes you feel like you should be grateful for whatever you get.

"We've got the goods. We know what we're doing. Pay us better, so we don't have to struggle through life," she said.

See the full interview in Part 10 here.

10. Don't rely on your credit card (Part 11)

Anita Kapoor advises freelancers to build savings and not rely on credit card. Screengrab from our video interview.

That was Anita's answer to the final question of our conversation - what would she tell her younger self, just starting out as a freelancer with no guaranteed income, about buying a home in Singapore?

"The things I would have done better? Keep way better records. Not rely on my credit card, because that was so destroying. And think about what I actually really want for my life. Do I want to own a home? If you don't want to own a home, then you've got to make sure you have the savings to cover your rental. If I want to own a home, then these are the steps I need to take as a freelancer," she said.

Anita's answer echoes what many of us navigated during our own financial uncertainties in our twenties and thirties.

Build your savings instead.

See the full interview in Part 11 here.

- Published on

By Khalil Adis

Two cities, one link. Woodlands North Coast (left) sits quietly in wait while Johor Bahru Sentral (right) buzzes with construction activity ahead of the RTS Link's targeted opening in January 2027. Photos taken on May 6 and 11, 2026. Photo: Khalil Adis Consultancy.

The Kuala Lumpur-Singapore High-Speed Rail (HSR), the most obvious example, was announced with great fanfare, then quietly shelved.

But here's one that most people do not know about.

Before the current Johor Bahru–Singapore RTS Link took shape, there was an earlier plan - one that never made the headlines.

Based on my interviews with Malaysian officials and local sources around 2008, the original RTS Link was designed to connect Medini, near Legoland Malaysia, to Tuas Link MRT station - not Woodlands.

At the time, Iskandar Malaysia was in full swing.

Nusajaya (now Iskandar Puteri) and Medini were the centrepieces of the entire development vision, each with dedicated master developers - UEM Sunrise for Iskandar Puteri and Iskandar Investment Berhad (IIB) for Medini - and detailed master plans built around catalytic industries to drive economic activity and property demand.

The Medini-Tuas RTS Link was part of that vision.

Then it was quietly dropped.

Even the revised RTS Link we know today had a troubled journey.

Originally targeted for operations in 2018, it suffered delays and suspensions before being revived in 2020.

With operations now targeted for January 2027, the gateway cities have shifted entirely: from Medini, Gerbang Nusajaya and Tuas, to Johor Bahru Sentral and Woodlands North Coast.

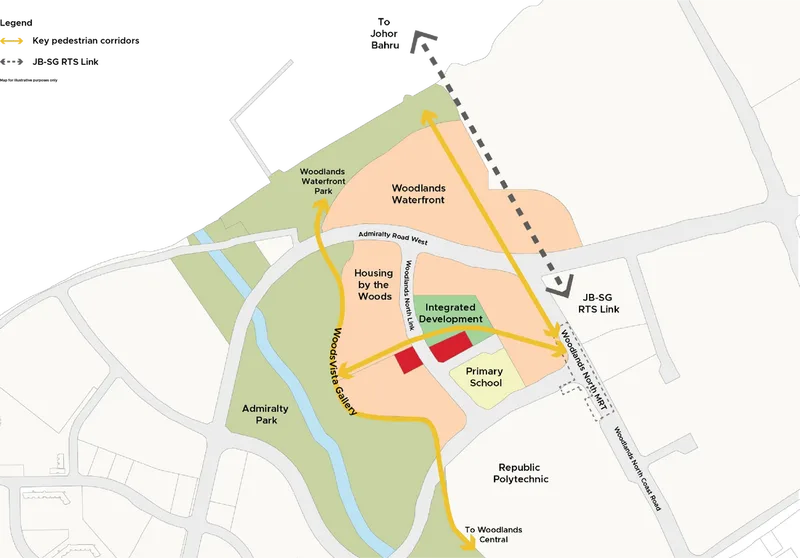

Woodlands North Coast: Singapore's new gateway city

For example, from 2023 onwards, I had noticed that some HDB flats in Woodlands were transacting with a cash-over-valuation (COV) of around $20,000.

I know this based on my ground experience and when speaking to realtors in Woodlands.

Prices were moving faster than HDB's valuations could keep up.

This created a real conundrum for buyers and sellers alike.

Cash-sensitive buyers backed out.

Some sellers facing ethnic quota constraints chose to renegotiate asking prices after receiving initial valuations, hoping a subsequent valuation would close the gap.

The Urban Redevelopment Authority (URA) has since laid out a comprehensive master plan for the area under Woodlands North Coast.

This is a mixed-use precinct featuring offices, business parks and residential developments along green boulevards near Woodlands North MRT station.

Adjacent to the RTS Link interchange station, Woodlands Gateway will serve as an employment and manufacturing hub, with flexible workspaces designed for both SMEs and multinationals across five 'Business 2 - White' and one 'Business 1 - White' sites.

An integrated transport hub will allow seamless transfers between the RTS Link, MRT and bus services.

To complete the live-work-play picture, two residential precincts, Housing by the Woods and Woodlands Waterfront, have been planned with convenient access to amenities and employment nodes.

Connecting both precincts is WoodsVista Gallery, a 1.9-kilometre community link with dedicated pedestrian and cycling paths.

JB Sentral: The old city reclaims its crown

For years, the federal government's budget and planning energy was squarely behind those two precincts.

As fate would have it, a combination of politics and royal endorsement changed everything.

The political upheaval following the 2018 general election effectively killed off the HSR project and disrupted federal development priorities.

Into that vacuum stepped the Sultan of Johor, a long-standing advocate of the RTS Link.

Since land is a state matter in Malaysia, his backing was pivotal and the RTS Link survived where other projects did not.

In anticipation of the RTS Link's launch, a major new gateway district has been planned around JB Sentral - the Ibrahim International Business District (IIBD).

It is worth nothing that it was previously known as the Ibrahim International District.

Developed by Johor Corporation (JCorp), the state investment arm of the Johor government, IIBD spans 240 acres in the heart of Johor Bahru, stretching from the Old Town to land parcels near Jalan Khalid Abdullah.

Envisioned to position Johor Bahru as Malaysia's second city after Kuala Lumpur, IIBD aims to attract tech start-ups, research institutions and businesses across multiple sectors.

It also encompasses existing commercial landmarks including Johor Bahru City Square, Komtar JBCC, Galleria @ Kotaraya, Persada Johor, Puteri Hotel and Menara Landmark.

To see how all of this is taking shape on the ground, I made a site visit on May 11.

The last time I had explored Johor Bahru on foot was in March 2020, just as Covid-19 was beginning to take hold and cross-border travel was still allowed (see article here).

I remember speaking to business owners along Jalan Dhoby and Jalan Tan Hiok Nee who were already reeling from the impact of the virus.

The usually bustling old town was eerily quiet, stripped of tourists.

That image stayed with me.

Almost six years on, the contrast is striking.

Walking from Stulang Laut to Menara Tabung Haji, I have to say the recent city rejuvenation and beautification programme led by the state government is significantly better than what was delivered under the federal government.

It is also worth noting that the Sultan of Johor, Sultan Ibrahim, now serves as Malaysia's 17th Yang di-Pertuan Agong - a role he assumed on January 31, 2024.

With Johor royalty occupying the highest office in the land, it is reasonable to expect that the political will and influence behind IIBD's success has never been stronger.

I still remember when the Johor Bahru Rejuvenation Programme was announced with much fanfare by the Iskandar Regional Development Authority (IRDA) around 2010, at a cost of some RM1.8 billion (I had covered the press conference at Persada Johor).

It included the much-publicised cleanup of Sungei Segget, modelled after the Cheonggyecheon Restoration Project in South Korea.

When it was completed around 2018, I recall feeling underwhelmed.

To be honest, it fell short of what it was supposed to be - a world-class river precinct.

It only reinforced my view that federal-mooted announcements in Malaysia can sometimes be half-baked promises.

Fast forward to today, the state government appears to have gone back and done it properly.

Take a walk along Jalan Wong Ah Fook and you would notice the addition of sculptures, communal spaces and water features that have transformed the stretch into something genuinely vibrant.

This is the Sungei Segget that was always supposed to exist.

Over at Stulang Laut, the marine viaduct is complete.

The RTS Link now traces a path along Jalan Ibrahim Sultan, turns into Jalan Ismail Sultan, then runs alongside Jalan Tun Abdul Razak next to Johor Bahru City Square before terminating at Bukit Chagar RTS station.

Earlier this year, a source from JCorp told me during a talk I was giving in February that Bukit Chagar is being planned as a transit-oriented development, with connectivity to nearby property developments in the works.

On the ground, that appears to be playing out.

For example, a dedicated covered overhead pedestrian link is already visible just beneath the RTS Link.

Construction at Coronation Square along Jalan Gereja is also underway, with Singaporean real estate firms CapitaLand and Ascott involved in what appears to be a mixed-use development.

One of the more telling shifts I observed was in retail.

The centre of gravity has quietly moved from Johor Bahru City Square to Komtar JBCC.

The latter, a perennial favourite among Singaporeans, had multiple shuttered outlets on the second and third floors, with upgrading works underway at ground level.

Even McDonald's has relocated to Komtar JBCC.

If Johor Bahru City Square feels like a mall catching its breath, Komtar JBCC feels alive and vibrant.

Sitting right next to Bukit Chagar station, it is well-positioned to become the dominant retail anchor in the district once the pedestrian link is completed.

Over in the heritage area, some shophouses are being torn down as part of the IIBD master plan.

My local sources tell me the state government is keen to redevelop JB's historic district into a vibrant precinct but the challenge lies in identifying landowners and getting them on board.

Many of these shophouses currently house migrant workers, adding another layer of complexity to the process.

For all its momentum, JB Sentral still has a fundamental urban planning challenge.

It feels, at times, like a haphazard urban sprawl with new infrastructure being layered on top of an existing city rather than a coherent, integrated vision.

What would be ideal is a single integrated development housing the current CIQ, Bukit Chagar RTS station and the KTM station as well as bus interchange, allowing seamless transfers between lines.

Alas, unlike Singapore, compulsory land acquisition is difficult to execute in Johor due to complex land ownership issues.

That constraint is real and unlikely to be resolved quickly.

What is certain is this: once the RTS Link opens, JB's tourism, retail, commercial, residential and banking and finance sectors are set to see a significant uplift from cross-border traffic.

The only question is how much of that upside you want to be positioned for and how early.

In closing

They are shaped by infrastructure, political will and - as this story shows - sometimes a change in both.

Woodlands North is as close to a sure bet as Singapore's property market offers right now.

The master plan is detailed, the transport connectivity is real and the investment case is clear.

On the Malaysian side, the calculus is more nuanced.

JB Sentral and the IIBD carry genuine momentum, but history reminds us that government-backed projects in Malaysia can shift with the political winds.

That's not a reason to avoid the market.

It is simply a context that every property buyer and investor should carry with them when making decisions based on connectivity and long-term growth.

- Published on

By Khalil Adis

Rendang, ketupat and chicken cooked in a traditional green chilli coconut gravy (Ayam Lemak Cili Padi) - the Hari Raya table that sparked a conversation about LPAs, wills and CPF nominations. Photo: Khalil Adis.

But this year's celebration hit different.

When I visited my elderly relatives, some had just been discharged from hospital.

Others were dealing with chronic health conditions.

The usual pleasantries like "how are you," and "how's the family”, gave way to something heavier.

We found ourselves talking about mental incapacity, death, and whether any of us had made sufficient preparations for when that moment comes.

For the longest time, these were conversations my relatives would avoid.

But with several deaths in the family over the years, there is no sidestepping them anymore.

A greying population

A photo of an elderly man in an HDB flat. Photo courtesy of Lgh_9 by Pexels.

According to the Singapore Department of Statistics, the proportion of citizens aged 65 and above is rising faster than in the previous decade.

The median age of the citizen population edged up from 43.4 to 43.7 years between June 2024 and June 2025.

And the number of citizens aged 80 and above has jumped roughly 60 percent - from 91,000 in 2015 to 145,000 in 2025.

The real question behind these numbers: as our population ages, are our elderly actually prepared?

And when they're not, who bears the burden?

From my Hari Raya visits, it is clear some relatives are not prepared.

A few refuse to face reality altogether, assuming a CPF nomination is sufficient.

Others say they do not need a will and automatically assumes their property will undergo a faraid (not true for a property held under a joint tenancy) and that their beneficiaries will know what to do.

It isn’t - and when the time comes, that gap in planning can cause confusion, disagreements and lasting rifts among family members.

I had seen this all before at the hospital and funerals.

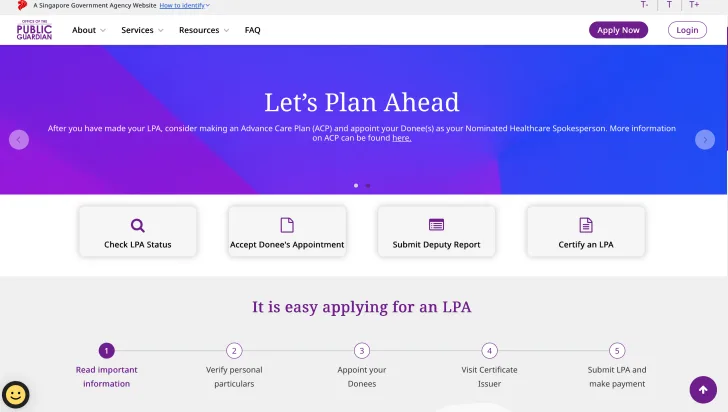

Lasting Power of Attorney

Screengrab for a Lasting Power of Attorney (LPA) online application from the Office of the Public Guardian, Ministry of Social and Family Development, website.

Barely a day goes by without a dramatised segment on Warna, our local Malay radio station, driving home why having one matters.

To push more Singaporeans to act, the government announced that LPA Form 1 applications will be permanently free for all Singapore citizens from April 1.

The move came after Minister of State for Social and Family Development Goh Pei Ming revealed in Parliament on March 5 that only about 404,000 Singapore citizens - roughly one in seven - had made an LPA as of February 20.

Among those aged 65 and above, the figure was slightly better but still sobering: about one in four, or 197,000 people.

But what happens when someone loses mental capacity before an LPA is done?

Then the cost goes up significantly - by up to $9,000.

In such a scenario, the family member will need to apply for a deputyship with the Family Justice Court.

Depending on complexity, it can take up to six months.

Therefore, it is advisable to do an LPA immediately while our loved ones still have mental capacity.

Wills

Photo by Alena Darmel courtesy of Pexels.

Among my relatives, the pushback is real and the misconceptions are plenty.

The most common one: "I don't need a will because my estate will go through faraid anyway."

That's not entirely true.

If you own a property under a joint tenancy, it does not automatically fall under faraid distribution - it passes to the surviving owner.

A will helps clarify your intentions and ensures your assets are distributed the way you actually want.

Then there's the "my family will know what to do" camp.

With respect - they probably won’t and the process will be painful for them.

Without a will, the surviving family members will have to apply for a Grant of Letters of Administration to manage your estate.

That can take up to two years and cost up to $5,000.

Trust me, I have seen friends go through this.

The entire process is stressful, expensive and entirely avoidable.

With a will, the process is significantly simpler - typically around $1,000 and up to three months.

You name an executor and trustee who can then settle your debts, handle Islamic claims, funeral and burial expenses, and distribute your properties, savings and possessions according to faraid and the Inheritance Certificate issued by the Syariah Court.

It is one of the most considerate things you can do for the people you leave behind.

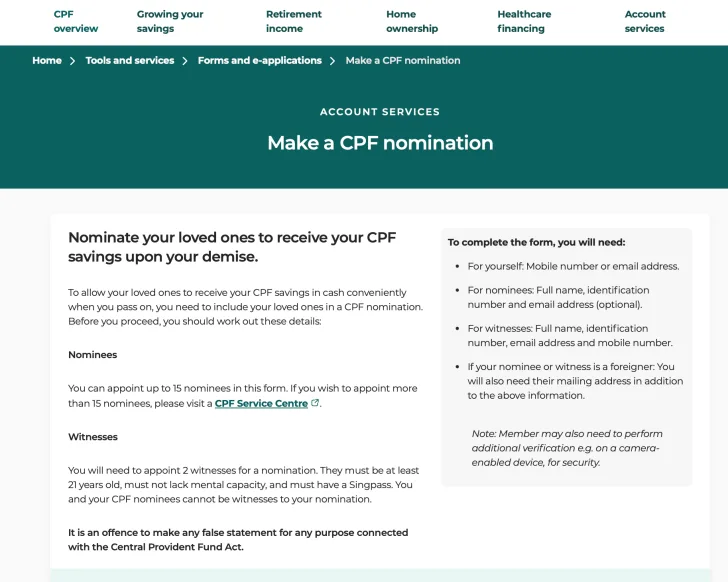

CPF nominations

Screengrab from CPF's website where you can make a nomination online.

A CPF nomination determines who receives your CPF savings after you are no longer around and how much each person gets.

Without one, your CPF savings will be transferred to the Public Trustee's Office, which will then distribute them according to intestacy laws - a process that takes time and comes with administrative fees deducted from the savings itself.

With a nomination in place, your loved ones receive the money directly in cash, faster and without the hassle.

The whole process takes minutes and can be done online via the CPF Board's website.

So here's my question for you and I say this as someone who had these conversations over ketupat and rendang this Hari Raya: have you done your LPA, your will and your CPF nomination?

If the answer is no, or not yet, now is the time.

Not because we are being morbid but because it is one of the most loving and practical things we can do for the people we leave behind.

Death is inevitable.

The confusion, the disputes and the burden on our families - those are optional.

- Published on

By Khalil Adis

A shophouse in Negeri Sembilan with Malaysian flag. Photo: Khalil Adis Consultancy.

"For 2026, Malaysia's economy is projected to grow at a moderate pace of between 4.0 and 4.5 percent, weighed down by prevailing global uncertainties due to ongoing geopolitical and geoeconomic tensions," said Prime Minister Anwar Ibrahim in his Budget 2026 speech in October last year.

On the supply side, affordable housing projects under the Perumahan Rakyat Residensi (PRR) and Rumah Mesra Rakyat (RMR) programmes worth RM672 million are due for completion this year, including PRR Ayer Lanas in Kelantan and PRR Masai in Johor, benefiting some 33,000 residents.

Gig workers get a path to homeownership

A GrabFood delivery person. Photo: Khalil Adis Consultancy.

Malaysia's gig economy counts roughly 1.2 million workers, according to Human Resources Minister Steven Sim Chee Keong, who was blunt about the gap in protections when speaking in Parliament.

"For too long, 1.2 million Malaysians in the gig sector have worked daily without proper labour protection, as if their contributions to the economy did not deserve recognition. This bill ends that injustice," he said.

To make homeownership more accessible for this group, the government has doubled the Syarikat Jaminan Kredit Perumahan (SJKP) guarantee ceiling from RM10 billion to RM20 billion, enabling an additional 80,000 first-time buyers to access mortgage guarantees.

This comes on the heels of the Gig Workers Bill 2025, passed in August last year, which for the first time requires platforms such as Grab and Foodpanda to provide formal contracts covering payment terms, insurance and termination procedures.

The law also bans arbitrary account deactivations and unilateral rate changes, and establishes a tribunal to handle disputes.

Workers will also be covered under Socso and EPF for the first time.

Stamp duty relief extended

Photo by Nataliya courtesy of Pexels.

Those purchasing homes priced up to RM500,000 will continue to enjoy stamp duty exemptions on transfer deeds and loan agreements, with the relief extended to December 31, 2027.

Taken together, these measures point clearly in one direction: the property market in 2026 will favour affordable properties.

Johor: Malaysia's hottest investment corridor

View of JB Sentral. Photo: Khalil Adis Consultancy.

According to the Malaysian government, the Johor-Singapore Special Economic Zone (JS-SEZ) recorded RM37.1 billion in approved investments in the first half of 2025 alone - representing 66 percent of Johor's total investments - with a further RM29 billion in new investment commitments secured.

In his Budget 2026 speech, Prime Minister Anwar Ibrahim said the JS-SEZ "has strengthened investor confidence in Johor as Malaysia's strategic gateway.”

Supporting this momentum, the Iskandar Malaysia Facilitation Centre is streamlining approval processes through the Johor Super Lane, cutting local authority approval timeframes.

The Johor Talent Development Council is also working to link universities with industry to build the skilled workforce needed to sustain long-term growth - a factor that typically anchors residential demand around economic zones.

Johor Bahru Sentral, in particular, will be an area to watch due to the planned opening of the Johor Bahru–Singapore Rapid Transit System (RTS) Link in January 2027.

Key sectors set to enjoy the economic spillover include real estate, tourism, retail, food and beverage, financial services and transportation.

Growth areas: Rail connectivity opening up new property corridors

Butterworth KTM Station will be an interchange station to the Mutiara Line. Photo: Khalil Adis Consultancy.

Several rail projects flagged in Budget 2026 are either recently operational or nearing completion - and history shows that rail connectivity consistently lifts surrounding property values.

In the Klang Valley, the LRT3 connecting Bandar Utama to Johan Setia, Klang - with capacity for over 6,200 passengers per hour per direction - was expected to begin operations by end-2025, opening up the Klang corridor.

The ETS rail service has also extended to Kluang, with the final leg to Johor Bahru Sentral targeted for completion around the same time.

In the north, the Mutiara LRT Line in Penang has commenced construction and is set to benefit an estimated 1.8 million residents and 3.5 million visitors when it opens in December 2031.

The line is expected to unlock property values along its route and drive significant investor interest in Penang's market.

On the east coast, the ECRL Phase 1 from Kota Bharu to Gombak is due for completion by end-2026, slashing travel time between Kelantan and the Klang Valley to four hours.

This will likely sharpen investor interest in properties along the corridor, particularly in areas currently underserved by connectivity.

Longer term, the Klang Valley Double Track Phase 2 (KVDT2) - connecting Bandar Tasik Selatan to Seremban and Simpang Pelabuhan Klang to Port Klang at a cost of RM4.1 billion - is targeted for full completion by 2029.

The big four states among foreign and local investors

The busy intersection at Jalan Bukit Bintang, Kuala Lumpur. Photo: Khalil Adis Consultancy.

For a detailed analysis on the growth areas, refer to my article here.

Increase in stamp duty for foreign buyers and companies

Photo by Nataliya Vaitkevich courtesy of Pexels.

The move is aimed at keeping house prices competitive for Malaysians.

Individuals with permanent resident status in Malaysia will be exempted.

- Published on

By Khalil Adis

View of downtown Singapore. Photo: Courtesy of Alesia Kozik from Pexels.

The government has been ramping up the supply of Built-to-Order (BTO) flats and private homes since 2025 in a bid to ease housing pressures across both the public and private markets.

In the HDB segment, authorities announced plans to launch about 19,500 new BTO flats in 2025 alone.

Meanwhile, data from the Urban Redevelopment Authority (URA) shows that the expansion in private housing supply is expected to deliver around 57,000 private residential units over the next few years, including Executive Condominiums (ECs), largely stemming from recent Government Land Sales (GLS) programmes.

Taken together, the growing supply pipeline is expected to gradually shift bargaining power toward buyers.

Opportunities also abound for investors in Singapore-listed real estate investment trusts (S-REITs), especially the office and retail sectors.

Flat buyers lured by new BTO launches

Artist’s impression of the first BTO project in Sembawang North launched in July 2025. Photo: HDB.

“While resale HDB prices grew by 2.9 per cent year-on-year in 2025, it was the slowest annual growth since 2019,” said Wong Xian Yang, head of research, Singapore & Southeast Asia, Cushman & Wakefield.

Property agents say the resale HDB market slowed considerably in 2025 compared with the previous year as buyer urgency eased.

“Previously, a single listing could attract up to ten buyers vying for a resale HDB flat, especially one sold without any extension. Usually they would be sold within a weekend. In the current market, you are lucky to get one or two viewers, and even then it may take time to sell the unit,” said Hakim Halim, associate group director at PropNex.

The slowdown could extend into 2026 as new supply enters the market.

Between 2025 and 2027, HDB plans to launch about 55,000 flats, up from its earlier commitment of 50,000 flats, to meet housing demand.

As more buyers divert their attention toward new BTO launches, resale price pressures are expected to ease further, reinforcing expectations of a more buyer-friendly market.

Million dollar HDB flats still active

HDB flats at Dawson Road. Photo: Khalil Adis Consultancy.

According to data from HDB, a total of 1,510 such flats changed hands during the year, including 302 units in Toa Payoh alone.

Toa Payoh recorded the highest number of million-dollar four-room resale flats (195 units), followed by Queenstown (114 units) and Bukit Merah (110 units).

For five-room flats, Bukit Merah led with 106 transactions, followed by Toa Payoh (93 units) and Queenstown (53 units).

Serangoon recorded the most executive flats sold (44 units), followed by Bishan and Hougang (38 units each), Woodlands (29 units) and Pasir Ris (20 units).

Only two three-room million-dollar resale flats were sold island-wide, both in the Kallang/Whampoa area.

Three Multi-Generation resale flats were transacted, with one unit each in Bishan, Central and Tampines.

Softening private property market as buyers gravitate to new launches

Skye at Holland. Photo: Holly Development Pte Ltd.

URA data showed that the private property price index rose 0.6 per cent quarter-on-quarter in the fourth quarter of 2025, compared with a 3 per cent increase in the previous quarter.

For the full year, prices rose 3.3 per cent, marking a slower pace of growth.

“Private residential prices rose 0.6 per cent quarter-on-quarter in the fourth quarter of 2025, or the fifth straight quarter of increase. Full year 2025 growth was 3.3 per cent year-on-year, moderating from 3.9 per cent year-on-year growth in 2024, or the lowest pace of annual increase since the pandemic year of 2020, suggesting overall buyers’ caution,” said Wong.

Sales volumes also declined.

“Overall private residential sales volume fell by 9.5 per cent quarter-on-quarter or 9.9 per cent year-on-year to 6,699 units in the fourth quarter of 2025. The decline in overall sales volume was driven by the new sales market, which fell by 10.6 per cent quarter-on-quarter to 2,940 units due to fewer new launches in the fourth quarter of 2025,” said Wong.

There were six new launches in the fourth quarter of 2025 (2,766 units), compared with nine launches (4,146 units) in the third quarter.

Resale transactions fell 9.1 per cent quarter-on-quarter to 3,529 units, while sub-sales declined 2.1 per cent to 230 units.

However, selected new launches continued to see strong take-up rates.

“The robust demand at new launches powered developers’ sales to an 11-month high in October,” said Kelvin Fong, CEO of PropNex.

Projects such as Skye at Holland, Penrith, Faber Residence and Zyon Grand recorded strong launch-weekend sales.

Prime Core Central Region (CCR) launches also saw their strongest monthly sales since 2007, driven largely by Skye at Holland.

With 1,510 million-dollar HDB flats transacted in 2025, analysts say upgrader demand into private housing is likely to persist.

“Barring new cooling measures, we are cautiously optimistic that private residential prices could grow by 2.0 to 4. per cent year-on-year in 2026 supported by low borrowing costs, increasing land prices and resilient buyer confidence, underpinned by still-low unemployment rates. HDB upgrader demand is still expected to persist, though overall momentum could slow.” Wong said.

PropNex echoed this view.

“With moderating price growth and low interest rates, we believe there is a window of opportunity in 2026 for prospective buyers, including HDB upgraders,” Fong said.

S-REITs outlook improving amid stabilising rates and stronger fundamentals

Office and retail space at Changi Business Park. Photo: Khalil Adis Consultancy.

“Lower interest rates matter for REITs because they gradually reduce financing costs as debt is refinanced and make REIT yields more attractive relative to other low-risk investment options such as Treasury Bills,” said Nupur Joshi, CEO of the REIT Association of Singapore (REITAS).

Against this backdrop, S-REITs are expected to benefit from improved refinancing visibility and more predictable funding expenses.

Analyst sentiment has also turned more positive.

“Several research houses now expect the S-REIT sector’s distribution per unit (DPU) growth to resume in 2026, supported by steadier interest rates and resilient asset fundamentals,” Joshi added.

Singapore’s reputation as a well-regulated and transparent market for listed real estate vehicles continues to attract global institutional capital seeking stable, income-generating exposure in Asia.

Market initiatives aimed at deepening equity participation and liquidity could further support listed trusts, particularly those outside the largest benchmark indices.

“The Singapore equity market has also been in a bit of a tear due to international investors seeing Singapore as a safe and well-governed market, resulting in global capital flowing into Singapore, alongside stock-market reforms initiated under MAS’ Equity Market Development Programme. This benefits Singapore-listed REITs,” Joshi said.

Looking ahead, the office and retail segments are showing promising signs, although prospects remain uneven across property types.

“The Singapore office sector is expected to do well due to strong demand and limited supply. Singapore retail scene is also improving. For REITs with overseas properties, it will depend on the asset class and geography, but overall industrial, logistics and data centre REITs are expected to do well due to structural tailwinds,” Joshi said.

- Published on

By Khalil Adis

Young Singaporeans walking along Orchard Road. Photo: Khalil Adis Consultancy.

Married to a permanent resident, the couple had to wait three years before they could even begin their home-buying journey.

Like many young Singaporeans that I had met recently, affordability was a major concern.

The 4-room flats in their preferred areas were priced between $500,000 and $600,000, leaving them wondering if homeownership was financially realistic.

However, after receiving their HDB Flat Eligibility (HFE) letter, their dream began to feel within reach.

Turning dreams into reality

Lower Seletar Reservoir Park Connector. Photo: Khalil Adis Consultancy.

With their finances secured, their maximum loan was approved for the upper $300,000 range, giving them a strong foundation for their home purchase.

Armed with their budget, the couple began house hunting.

Their requirements were clear.

Firstly, the unit needs to have a flexible layout to accommodate their future family needs.

Secondly, it has to be within 4km from Sam's parents.

Thirdly, it has to be within access to park connectors and green spaces - an important factor for their growing child.

After two weeks of viewings, they finally secured their dream home in northern Singapore.

To their relief, the unit did not come with any cash-over-valuation (COV), making it even more affordable.

Housing aspirations are evolving

Scaled model of eco-friendly and sustainable HDB estates. Photo: Khalil Adis Consultancy.

While previous generations also focused on affordability, here are some of today’s additional considerations I noticed young buyers have:

Rising cost of living

With inflation driving up prices, many young Singaporeans are rethinking long-term financial commitments.

As a result, co-living spaces have gained popularity among young professionals.

The flexibility of renting appeals to those who prefer mobility, much like digital nomads..

The gig economy

Unlike previous generations, full-time employment is no longer seen as the only path to stability.

Many now prioritise work-life balance and mental health which affect their housing choices (and how much loan they can get should they decide to switch to freelancing).

Sustainability

There’s a growing emphasis on green developments with many young buyers actively seeking eco-friendly features.

So far, the government has kept pace with these changes, introducing Climate Vouchers, rolling out solar panels in HDB estates and prioritising sustainable town planning.

I would also say, young Singaporeans are also health conscious leading active lifestyles.

This explains why some of them prefer living near to gyms or park connectors.

Shifting family patterns

At the same time, marriage and family patterns are shifting.

Rising living costs and career aspirations are leading many to delay marriage and homeownership.

According to data from the Department of Statistics Singapore (2024), the number of single Singaporeans in their 30s has increased by 13 per cent over the last decade

Housing challenges for singles

Commuters at Punggol Bus Interchange. Photo: Khalil Adis Consultancy.

With these rising costs, some singles are finding it difficult to secure housing.

A friend of mine, for instance, has temporarily relocated to Malaysia while waiting for clearer housing policies.

The government has taken steps to address this issue—since June 2024, singles can now purchase HDB flats in all locations (previously, they were limited to non-mature estates).

However, some still feel that they should be allowed to purchase 3-room flats instead of being restricted to 2-room units.

For low-income earners and freelancers, this limitation makes it harder to afford homes in the resale market.

If you are single and considering homeownership, I would urge you to explore the many available grants.

You can then subsequently upgrade and consider different housing types once you have met your Minimum Occupation Period (MOP).

As we have already seen, the property market is ever evolving and policies may continue to shift post-election.

Government’s response and policy adjustments

Screengrab of a car-lite estate in Bayshore courtesy of HDB.

To address these concerns, the government has introduced various measures.

Firstly, there is greater transparency in pricing and shorter waiting times for BTO flats.

Secondly, since February 14, 2023, the CPF Housing Grants has been increased for first-time resale flat buyers—by up to $30,000. This makes homeownership an even more attainable dream.

Thirdly, as of March 2025, the government had announced an expanded Fresh Start Housing Scheme where first-timer families can now apply. Previously, it was limited to second-timers only.

Last but not least, sustainable housing initiatives such as green townships, car-lite communities (such as Tengah and Bayshore) and recycling rubbish chutes as well as solar panel are now being rolled out in BTO flats.

For those seeking rental options, the Public Rental Scheme (PRS) provides affordable housing for lower-income Singaporeans.

However, for professionals who prefer co-living spaces, the Single Room Shared Facilities (SRSF) Pilot remains one of the few available government-backed options.

As we can see from the above examples, the government has consistently adapted housing policies to meet public demand.

However, balancing affordability and long-term sustainability remains a challenge.

With Singapore’s strong emphasis on homeownership, I would encourage young Singaporeans to consider getting their first step into the property market.

Ultimately, owning your home versus long-term rental will be a more sustainable option.

Conclusion: The future of housing policies in Singapore

An HDB estate in Punggol. Photo: Khalil Adis Consultancy.

As their preferences and expectations evolve, policymakers must respond with innovative solutions to ensure that housing remains accessible, affordable and aligned with modern lifestyles

Having said that, Singapore remains one of the few countries where our government continues to offer assistance to make homeownership attainable.

As a Singaporean, I am proud to say that Singapore has one of the highest homeownership rates in the world at more than 90 per cent, thanks to careful long-term planning.

However, as society evolves, housing policies will also need to keep pace.

- Published on

By Khalil Adis

Kuala Lumpur's city skyline. Photo by Khalil Adis.

“Where should one even begin?” I wondered.

As I navigated the complex property market and started speaking to various analysts and market leaders, I realised there are a few key cities that have seen consistent demand among both local and foreign investors.

I had also assumed that, like Singapore, high-rise residential apartments were the most popular property type in Malaysia.

This is a common mistake that many Singaporean investors make.

However, when you speak to locals, many would prefer living in a freehold landed terraced home.

These are just some of the nuances one must grasp when understanding the Malaysian property market.

Fast forward to 2025, these key cities for property investments remain the same—Johor (including Iskandar Malaysia), Selangor, Kuala Lumpur, and Penang.

Here is a quick review of each market, what happened in 2024 and the predictions for 2025.

Kuala Lumpur: A city of opportunities and challenges

The busy intersection of Bukit Bintang, Kuala Lumpur. Photo by Khalil Adis.

With its favourable exchange rate, exciting nightlife, unrivalled shopping experience, delicious local foods and tourist attractions, it is no wonder Kuala Lumpur remains a perennial favourite among Singaporean and local investors.

However, Kuala Lumpur also has its share of challenges, which many investors may not be aware of.

According to data from the National Property Information Centre (NAPIC), of the total 22,642 overhang units in Malaysia as of the first half of 2024, Kuala Lumpur had the third-highest residential overhang status in the country at 3,051 units.

In Kuala Lumpur, these unsold units are comprised mainly of condominiums and apartments.

According to NAPIC, in terms of value, Kuala Lumpur recorded the highest overhang value, with RM3.06 billion worth of unsold units.

Across Malaysia, properties priced at more than RM1 million contributed to 12.0 per cent (2,719 units) of the national total.

Since the minimum purchase price for a foreign investor in Kuala Lumpur is RM1 million, imagine the intense competition you may face in the resale market if you decide to offload your property.

The sheer number of unsold units compared to what Malaysians can generally afford (below RM300,000) means you might have to either sell your property at a loss or wait a long time for the right buyer.

The oversupply of condominiums and apartments also affects rental income.

Rental market trends in Kuala Lumpur

According to listings on PropertyGuru Malaysia, two-bedroom condominium units in KLCC have an average asking rental price of RM3,000 per month.

Assuming your mortgage payments amount to RM3,700, your rental income alone would not be sufficient to cover your property upkeep and other expenses.

Likewise, rental yields may not be as attractive.

For example, an RM1 million unit rented out at RM3,000 per month would generate a rental yield of 3.6 per cent.

For better rental yields, investors should consider buying near transportation hubs like the newly constructed Kajang MRT Line, Putrajaya MRT Line, LRT stations, and educational institutions.

These areas tend to have high foot traffic and excellent connectivity, making them desirable for renters.

Selangor: The heartland of Malaysia’s property market

Border crossing in Malaysia demarcating the state of Selangor and Kuala Lumpur. Photo by Khalil Adis.

Think of it as Kuala Lumpur’s heartland, similar to Singapore’s Punggol or Ang Mo Kio, where property prices are significantly lower than in the city centre.

Over the years, Selangor has benefited from several federal government-initiated transportation projects that have positively impacted the property market.

These include the Kajang MRT Line and Putrajaya MRT Line.

While property prices in Selangor are more affordable, there is a catch—the minimum purchase price for foreigners is RM2 million.

This presents a conundrum.

If offloading a RM1 million property in KLCC is already challenging, selling a RM2 million one further from the city centre becomes even more difficult.

To put it into Singaporean terms, it is like trying to sell a S$2 million condominium in Punggol and hoping a local buyer living in a S$500,000 four-room flat will upgrade.

Similarly, within Selangor, the price gap between what locals can afford and what foreigners must pay is substantial.

Also, most locals would prefer to buy a freehold landed property for the same price.

Rental market trends in Selangor

Selangor does, however, present a vast rental market.

According to NAPIC, all districts recorded modest growth in rental rates for terraced houses and high-rise units, particularly in Petaling, Klang, Hulu Langat, and Gombak.

Given the preference for landed homes, it is not surprising that such properties in select areas saw higher rental rates.

For instance, NAPIC data showed that double-storey terraces in urban centres such as Mutiara Damansara, Bandar Utama, Subang Jaya, and Bandar 16 Sierra had rental rates ranging from RM2,200 to RM2,800 per month.

Meanwhile, similar houses in Setia Eco Templer, Taman Alam Sari, and Setia Eco Glade recorded higher rental rates between RM2,500 and RM3,900 per month.

Notably, these are all township developments located away from the city centre in Rawang, Bangi, and Cyberjaya, respectively.

Johor: A promising start that fizzled out

Scaled model showing the proposed High-Speed Rail station for Gerbang Nusajaya's master plan. Photo by Khalil Adis.

I recall attending a media site visit where officials from the Iskandar Regional Development Authority (IRDA) and Iskandar Investment Berhad (IIB) presented their master plan for Flagship B, showcasing catalytic industries such as Islamic finance, education, tourism, creative, and high-tech manufacturing.

At the time, the vision was impressive.

Yet, many Singaporeans I interviewed remained skeptical.

By 2013, however, interest in Iskandar Malaysia surged among Singaporean investors, especially after Temasek Holdings announced its investment in Danga A2 Island through CapitaLand Malaysia Pte Ltd.

However, somewhere along the way, the master plan changed beyond recognition.

Massive high-rise developments sprang up along Danga Bay and near the Second Link, particularly with the introduction of Forest City.

Market analysts began sounding alarms about oversupply, questioning the sustainability of Johor’s property market.

Fast forward to 2025, and the numbers from the National Property Information Centre (NAPIC) paint a concerning picture. Johor recorded the second-highest number of overhang units in Malaysia, with 3,219 unsold residential properties valued at RM2.80 billion—mostly condominiums and apartments.

That equates to an average price of RM869,835 per unit, a figure far beyond the reach of most Johoreans.

Johor Housing and Local Government Committee Chairman Datuk Mohd Jafni Md Shukor recently reported that Johor experienced over 15 per cent growth in overall property sales, including sales of previously overhung properties.

As of December 2024, Johor has 102,438 serviced apartment units, with 11,810 remaining unsold.

Despite these challenges, NAPIC data showed strong growth in serviced apartment transactions, with a 47.4 per cent increase in volume (6,804 transactions) and a 68.5 per cent rise in value (RM4.94 billion) in the first half of 2024 compared to the same period in 2023.

By state, Johor and WP Kuala Lumpur led the market, capturing 36.2 per cent (2,465 transactions) and 33.0 per cent (2,245 transactions) of the national total, respectively.

Yet, the 11,810 unsold units will continue to impact the resale and rental markets in the foreseeable future.

Rental market trends in Johor

Data from NAPIC revealed that Johor’s rental market remained stable, with mixed movements in urban centres such as Johor Bahru, Kulai, and Batu Pahat.

Due to their limited supply, landed terraced homes continue to perform better in the rental market.

For instance, double-storey terraced homes in Horizon Hills and Taman Laguna fetch between RM2,200 and RM3,000 per month.

With the upcoming Johor-Singapore Special Economic Zone (JS-SEZ) and the RTS Link, areas like Bukit Chagar, JB Sentral, and the Ibrahim International District may experience renewed investor interest.

However, legal complications in Medini and continued concerns over the oversupply of high-rise units remain as cautionary factors.

Penang: The island effect

Waterfront developments against a hilly backdrop near Gurney Drive. Photo by Khalil Adis.

I remember spending nearly a week on the island, photographing developments and interviewing key developers, including SP Setia and IJM Land (which was then developing The Light).

Previously governed by the United Malays National Organisation (UMNO), Penang’s development accelerated under the Democratic Action Party (DAP).

A small but significant change caught my eye—Penang had started cleaning up its act.

For instance, Gurney Drive, once littered with rubbish, is now clean and well-maintained.

With George Town being recognised as a UNESCO World Heritage Site in 2008 and the launch of the George Town Festival in 2010, Penang’s appeal among tourists and investors has skyrocketed.

There is an unmistakable sense of pride among Penangites in preserving the historic city of George Town.

Similar to Singapore, Penang faces land scarcity and pent-up housing demand, which have driven up property prices—commonly referred to as the “island effect.”

However, unlike Singapore which is relatively flat, Penang has a hilly inner terrain making most parts of it unsuitable for development.

This, together with local regulations that prohibit developments from taking place on these hilly terrains, has resulted in very little land available for housing developments.

The scarcity of land versus the increase in demand for homes in Penang has brought about a spike in prices.

As a result, property prices are increasingly out of reach for locals, while foreign investors view Penang as an affordable retirement destination due to the lower cost of living.

According to NAPIC, recent easing of Malaysia My Second Home (MM2H) requirements has helped attract more foreign investors to Penang.

Key investment hotspots in Penang

Menara KOMTAR in George Town. Photo by Khalil Adis.

- Tanjung Bungah

- Tanjung Tokong

- Batu Ferringhi

- George Town

- Queensbay

- Gurney

Property overhang in Penang

Luxury condominiums along Gurney Drive. Photo by Khalil Adis.

With 8,168 units in the supply pipeline (including overhang, unsold under construction, and unsold not constructed), high-rise residential resale and rental markets are expected to remain competitive.

Penang’s rental market

Data from NAPIC shows Penang’s rental market has remained stable, with mixed movements in various districts.

Notably, single and double-storey terraced houses in Southwest Penang saw rental increases of 4.5 per cent to 10.0 per cent, with rentals reaching up to RM2,000 per month.

Moving forward, landed residential properties in Penang are likely to outperform high-rise units, given the strong local demand and limited land supply.

What happened in 2024?

Low cost housing project in Kuala Lumpur called Program Perumahan Rakyat (PPR). Photo by Khalil Adis.

According to data from the National Property and Information Centre (NAPIC), homes priced at RM300,000 and below accounted for 53.1 per cent of all residential transactions.

Overall, the residential sector recorded 121,964 transactions worth RM49.43 billion in the first half of 2024.

Compared to the same period in 2023, this marks a 6.1 per cent increase in volume and 10.4 per cent growth in value.

The boost in transactions can be attributed to various government incentives under Budget 2024 aimed at promoting homeownership, especially for first-time buyers.

One such initiative is the Housing Credit Guarantee Scheme (HCGS), which saw its funding increase from RM5 million in 2023 to RM10 million in 2024, helping up to 40,000 borrowers—particularly freelancers and gig workers—secure housing loans.

Another key measure was the RM2.47 billion budget allocation for the People’s Housing Project (PPR), also known as Program Perumahan Rakyat. This included RM546 million to continue 36 PPR projects, including a new development in Kluang, Johor.

Lastly, the government introduced a full stamp duty exemption on the instrument of transfer and loan agreements for first-time homebuyers purchasing properties priced up to RM500,000.

This exemption remains in effect until 31 December 2025.

Nationwide market performance

Landed terraced homes in Petaling Jaya, Selangor. Photo by Khalil Adis.

Johor followed, with 15.3 per cent of total transactions (18,648) and 18.2 per cent of total value (RM9.02 billion).

Together, Kuala Lumpur, Johor, Selangor, and Penang accounted for about 50 per cent of all residential transactions in Malaysia.

It is no surprise that landed terraced homes remained the most sought-after property type, making up 43.0 per cent of total transactions.

This was followed by vacant plots (15.3 per cent), high-rise units (14.3 per cent), low-cost houses/flats (10.8 per cent) and semi-detached homes (7.9 per cent)

Kuala Lumpur: Where rental growth thrives

The Oval in KLCC. Photo: Khalil Adis.

According to NAPIC, demand for double-storey terrace homes in premium areas like Damansara Heights, Desa Park City (Casaman), and Desa Sri Hartamas pushed monthly rentals beyond RM5,000.

Similarly, luxury condominiums in prime locations such as U Thant Residence, The Oval, 10 Mont Kiara, and Sunway Vivaldi recorded monthly rentals exceeding RM11,000.

Selangor: A landlord’s market

Cyberjaya in Selangor. Photo by Khalil Adis.

NAPIC data showed modest rental growth across Petaling, Klang, Hulu Langat, and Gombak, particularly for double-storey terraces in urban areas.

For example, Mutiara Damansara, Bandar Utama, Subang Jaya, and Bandar 16 Sierra saw monthly rental rates between RM2,200 and RM2,800.

Meanwhile, Setia Eco Templer, Taman Alam Sari, and Setia Eco Glade commanded even higher rentals, ranging from RM2,500 to RM3,900 per month.

Notably, these are township developments located outside central Kuala Lumpur, in Rawang, Bangi, and Cyberjaya.

Johor: A market under scrutiny

Medini in Iskandar Malaysia, Johor. Photo by Khalil Adis.

At the time, it seemed like a groundbreaking initiative, but over the years, bureaucratic and administrative setbacks began to surface.

In November 2024, I received a tip-off from a Singaporean buyer at Iskandar Residences who revealed shocking issues regarding property ownership in Medini.

In the documents seen, the individual strata titles that was issued nearly a decade later, showed that instead of the buyer being the legal owner, the title was still under Iskandar Investment Berhad (IIB).

This has now escalated into a legal battle, with 63 plaintiffs suing the developer, Distinctive Resources Sdn Bhd and the landowner, IIB, for fraudulent misrepresentation.

According to the source, around 10,000 homes within Medini do not have any strata title.

Given the Johor-Singapore Special Economic Zone (JS-SEZ) is being actively promoted, this controversy could shake investor confidence in Johor’s property market.

Johor’s rental market

An advertisement for a unit at 1 Medini. Photo by Khalil Adis.

Limited supply helped double-storey terraces in Horizon Hills and Taman Laguna fetch RM2,200 to RM3,000 per month.

Penang: Stability in the face of change

Charming shophouses in George Town, Penang. Photo by Khalil Adis.

According to NAPIC, Southwest Penang saw rental increases of 4.5 per cent to 10.0 per cent, with single and double-storey terraced houses fetching up to RM2,000 per month.

Moving forward, landed homes are expected to outperform high-rise units due to strong local demand and limited land supply.

Predictions for 2025: Where should you buy in Malaysia?

Kajang MRT station along the Kalang Line. Photo by Khalil Adis.

Why? This is because history has shown us that when new train lines, highways or economic zones are introduced, property prices in those areas tend to skyrocket.

It has happened before in places like KL Sentral and even parts of Iskandar Malaysia.

However, knowing where to buy is the tricky part.

Some areas will see real growth while others may remain stagnant for years.

That is why I have put together this guide—to help you cut through the noise and make a smart, informed decision.

Let us start with Johor.

Johor: Can it deliver?

Sultan Iskandar CIQ. Photo by Khalil Adis.

Needless to say, while I enjoyed it, it was a frustrating and exhausting experience.

Sometimes, it can take up to five hours just to cross the border.

It also made me wonder—will Johor ever become more than just a commuter town?

Fast forward to today, things are finally starting to change.

For example, the Johor-Singapore Rapid Transit System (RTS) Link is finally taking shape (like finally!), promising to slash travel time between JB and Singapore to just five minutes when it launches in 2026.

No more endless border queues that I used to endure!

If this were to actually happen as planned, areas like Bukit Chagar, JB Sentral, and the Ibrahim International District could see a huge surge in demand —for both homes and businesses.

The Land Transport Authority (LTA) estimates that it will carry up to 10,000 commuters per hour, in each direction, during peak times.

That means a massive boost for businesses, rental demand and home values in the surrounding areas.

Meanwhile, there is another interesting development: a new data center in Iskandar Puteri.

Telekom Malaysia and Singapore’s Nxera are working together to build this next-generation facility, which is set to be completed by 2026.

If Iskandar Puteri positions itself as a tech hub, we could see more high-paying jobs in the area—and with that, a stronger property market.

Broken promises?

The former Pinewood Iskandar Malaysia Studios. Photo by Khalil Adis.

For example, the much hyped about Bus Rapid Transit (BRT) has now been canceled.

Let us also not forget the high-profile government-to-government project, the Kuala Lumpur-Singapore High-Speed Rail (HSR) which has been scrapped (for now).

Finally, the Iskandar Malaysia much anticipated boom has delivered very mixed results.

Remember Sanrio Hello Kitty Town, Lat’s Place at Puteri Harbour and Pinewood Iskandar Malaysia Studios?

They are all gone.

What about the dismal footfall at Mall of Medini and eerily quiet neighbourhoods in certain parts of Iskandar Puteri and Medini when night falls?

Speaking of Medini, the ongoing court case involving Iskandar Residences in Medini has some buyers worried about whether the area is as investment-friendly as once promised.

Should you invest in Johor?

Gated and guarded landed homes called Estuari by UEM Sunrise in Iskandar Puteri. Photo by Khalil Adis.

If you are willing to bet on Johor’s long-term potential, focusing on areas near the RTS Link and major commercial projects could pay off.

Owner-occupied landed terraced homes (particularly gated and guarded) could also provide good capital gains over the long-term.

However, if you’re looking for a safe, guaranteed investment, you might want to wait out until the whole Medini debacle is resolved.

Kuala Lumpur: Is it still worth buying?

KL Sentral Monorail station. Photo by Khalil Adis.

Why? First, property prices here are high, with a median resale price of RM610,000—a steep entry point for most young buyers.

Second, KL is already a mature market, meaning there is limited room for rapid price appreciation compared to up-and-coming areas.

That said, if you are an investor looking for rental opportunities, certain areas—especially those along new MRT lines—still have potential.

My advice? Follow the infrastructure.

Where to look: The Putrajaya Line

Kepong Sentral: A hidden gem with industrial demand

This isn’t just another train stop—it is an interchange for the KTM Komuter Port Klang Line and serves one of KL’s most well-connected suburban hubs.