|

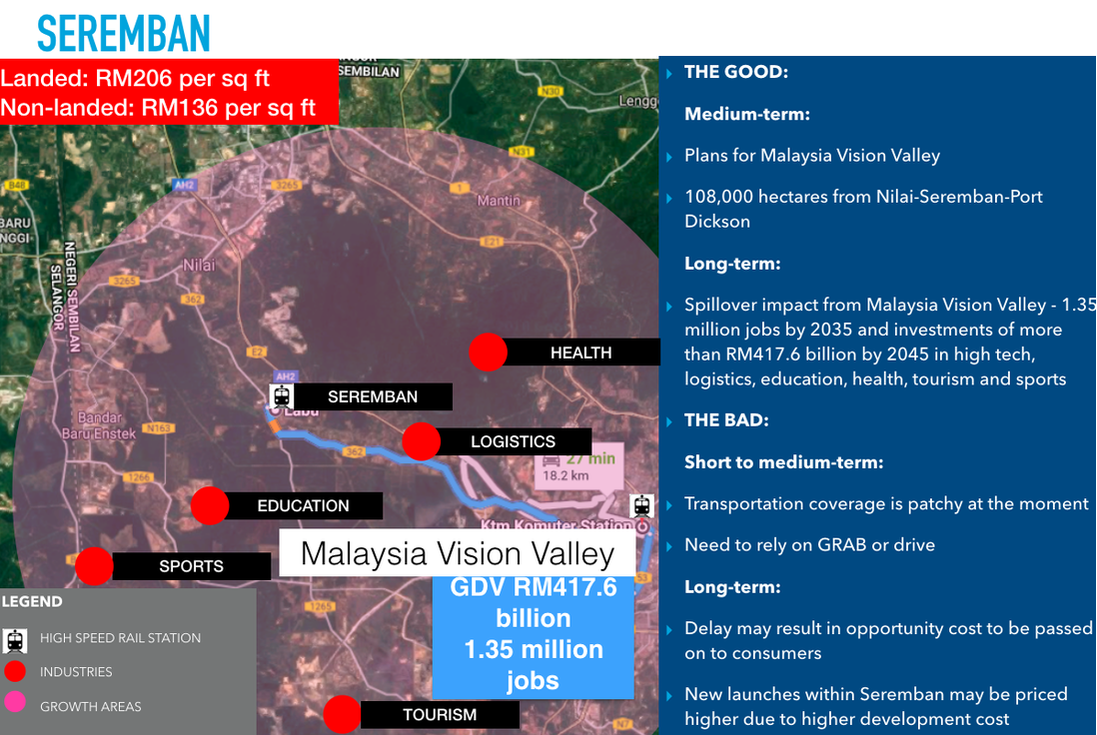

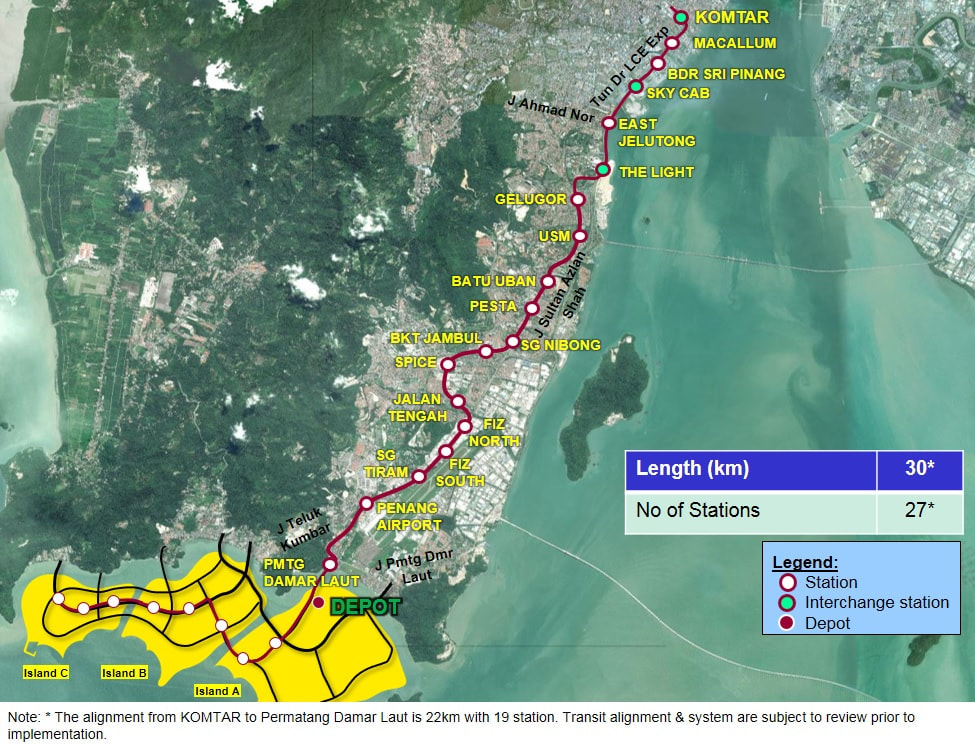

Mass market launches and rental markets in key urban areas are expected to see strong demand in 2024. By Khalil Adis  Kuala Lumpur city skyline. Photo courtesy of Pok Rie via Pexels. In 2023, the Malaysian property market saw significant trends and developments that have set the stage for the outlook and predictions for 2024. The huge mismatch between what Malaysians can afford to buy versus what developers are building has become increasingly apparent, leading to a shift in consumer behaviour towards renting instead of buying. With affordable housing in short supply, especially in highly urbanised areas like Kuala Lumpur, Johor, Penang, and Selangor, demand for rental properties surged in 2023. This increased demand for rental properties has led to a notable shift in the market dynamics, with renters seeking affordable and well-maintained units in desirable locations. In response to the changing market dynamics, developers in Johor, Selangor and Kuala Lumpur focused on catering to the mass market segment by launching new residential projects priced below RM300,000. These mass-market homes aimed to address the growing demand for affordable housing options among Malaysian buyers. On the other hand, the overhang market in Johor, Selangor, Kuala Lumpur and Penang was dominated by residential properties priced between RM500,000 to RM1 million. This suggests that there is a surplus of mid-range properties in these areas, which may take longer to sell due to affordability constraints and oversupply issues. Johor  Johor Bahru as seen from the Straits of Johor. Photo courtesy of Alix Lee via Pexels. In Johor, the property market is expected to continue facing challenges in 2024, particularly in areas with a high concentration of oversupply. The mass market segment, which saw an abundance of new launches priced below RM300,000 in 2023, may experience slower growth as developers adjust to the changing demand landscape. However, growth areas such as within Iskandar Malaysia may still present opportunities for investors, especially in well-planned integrated developments that cater to both residential and commercial needs. Selangor  Petaling Jaya in Selangor. Photo courtesy of Deva Darshan via Pexels. Selangor, being one of Malaysia's most populous states and a major economic hub, is expected to maintain its position as a key player in the property market. While the demand for affordable housing is likely to remain strong, developers may shift their focus towards more sustainable and inclusive development strategies. Growth areas such as Cyberjaya, Shah Alam and Subang Jaya are expected to continue attracting interest from both buyers and developers, with a focus on mixed-use developments and transit-oriented projects. Kuala Lumpur  Merdeka 118 tower in Kuala Lumpur. Photo courtesy of Jackson Tee via Pexels. In Kuala Lumpur, the property market is expected to see continued interest in high-density urban living, driven by factors such as urbanisation and lifestyle preferences. However, affordability concerns may lead to a greater emphasis on the development of affordable housing and innovative financing solutions. Growth areas within the city centre and its surrounding suburbs, such as KL Sentral, Bangsar and Mont Kiara, are expected to remain attractive to both investors and homebuyers. Penang  George Town, Penang. Photo: Khalil Adis Consultancy. Penang, known for its rich cultural heritage and vibrant lifestyle, is expected to continue experiencing steady demand for residential properties, particularly in sought-after areas such as George Town, Bayan Lepas, and Tanjung Tokong. However, affordability concerns and oversupply in certain segments may lead to a slowdown in the high-end property market. Developers may focus on niche markets and alternative housing options to cater to changing consumer preferences. The growth areas to watch out for on the main island are mainly along the proposed Bayan Lepas LRT. Growth areas  The growth areas in Malaysia are mainly those located near high-impact projects like MRT and transit-oriented developments. Photo: Khalil Adis Consultancy. In addition to established urban centres, growth areas such as transit-oriented developments, industrial zones, and emerging satellite towns are expected to attract interest from investors and homebuyers alike. These areas offer opportunities for sustainable development and investment diversification, while also addressing issues such as urban sprawl and congestion. Johor  Bukit Chagar will be located next to the Sultan Iskandar CIQ. Photo: Khalil Adis Consultancy. In Johor, the growth areas are primarily located in Iskandar Malaysia, especially in well-planned integrated developments that cater to both residential and commercial needs. One such area is Bukit Chagar which will serve as an interchange station Johor Bahru – Singapore Rapid Transit System (RTS) Link. Slated to commence passenger service by end-2026, the RTS Link can serve up to 10,000 commuters during peak periods, for every hour and in each direction. The RTS Link will also have a spillover impact in the nearby JB Sentral area which is home to malls, hotels and the upcoming Ibrahim International District. Selangor  Growth areas in Southern Kuala Lumpur. Infographics: Khalil Adis Consultancy. In Selangor, the growth areas are in Southern Kuala Lumpur, particularly, those near high-impact projects and transit-oriented developments along the Putrajaya Line, Kuala Lumpur–Singapore high-speed rail (HSR) and the Malaysia Vision Valley. Nilai and Seremban are areas to watch out for. Nilai is poised for further growth as it is located within the Malaysia Vision Valley. Covering Nilai to Port Dickson, it will have a proposed area of 108,000 hectares. The upcoming industries include high-tech, logistics, education, health, tourism and sports. The Malaysia Vision Valley is expected to create some 1.35 million jobs by 2035 and investments of more than RM417.6 billion by 2045. To support the Malaysia Vision Valley, the Seremban HSR station will be situated in Nilai within the Labu and Kirby estates. Major townships in the vicinity include Bandar Enstek, Bandar Ainsdale Property and S2 Height. Seremban will be an interchange station for the Seremban Komuter Line and KTM Electric Train Service. Kuala Lumpur  Bangsar Shopping Centre. Bangsar is one of the growth areas once the Circle Line is completed. Photo: Khalil Adis Consultancy. The growth areas in KL are along the MRT3 Circle Line, namely, Bukit Kiara Selatan, Bukit Kiara, Sri Hartamasa, Mont Kiara, Bukit Segambut, Taman Sri Sinar, Dutamas, Jalan Kuching, Titiwangsa, Kampung Puah, Jalan Langkawi, Danau Kota, Setapak, Rejang, Setiawangsa, AU2, Taman Hillview, Kuchai, Jalan Klang Lama, Pantai Dalam, Pantai Permai and Universiti. Titiwangsa MRT station which will serve as an interchange station with the Ampang and Sri Petaling Line, KL Monorail Line and Putrajaya Line. As the Circle Line is still under construction, this presents a good opportunity for genuine homebuyers to start looking in and around the station. Homes in the secondary market will be the most ideal as they are priced cheaper than new launches. Penang  Screen grab of the Bayan Lepas LRT line. Source: http://pgmasterplan.penang.gov.my The growth areas in Penang remain unchanged in Batu Kawan and some parts of Seberang Perai. Since the opening of the Second Penang Bridge, Batu Kawan has seen rapid developments from several renowned developers such as EcoWorld and Tropicana as well as the opening of IKEA. While connectivity remains patchy at Batu Kawan, there is a planned Bus Rapid Transit (BRT) system for Batu Kawan as part of the Penang Transport Master Plan. In Seberang Perai, the growth areas will be along the planned Raja Uda-Bukit Mertajam Line to connect the northwestern region to the southeastern region. For those who can afford to buy a property on the main island, areas along the Bayan Lepas LRT line will be the new growth corridor. What’s in store for buyers  Landed homes are popular among Malaysians. Photo: Khalil Adis Consultancy. Buyers in 2024 can expect a more diverse range of options in the property market, with an emphasis on affordability, sustainability, and lifestyle amenities. Innovative financing schemes and incentives may also be introduced to encourage homeownership and address affordability concerns. What’s in store for sellers  Aerial view of Medini and Iskandar Puteri. Photo: Khalil Adis Consultancy. Sellers may need to adjust their expectations and pricing strategies to align with changing market conditions. Those with properties in oversupplied segments may need to offer incentives or value-added services to attract buyers, while those in high-demand areas may continue to command premium prices. What’s in store for tenants  A mix of high-end and low cost residential homes in Kuala Lumpur. Photo: Khalil Adis Consultancy. Tenants can expect a more competitive rental market in 2024, particularly in urban areas where demand for rental properties is high. Affordability remains a key concern for tenants, and they may seek out properties with flexible lease terms and inclusive amenities. What’s in store for landlords  Bird's eye view of Kuala Lumpur. Photo: Khalil Adis Consultancy. Landlords may need to be more proactive in managing their rental properties, offering competitive rental rates and investing in property maintenance and upgrades to attract and retain tenants. Those with properties in growth areas may continue to enjoy strong rental yields and capital appreciation. Conclusion  Brickfields, Kuala Lumpur. Photo: Khalil Adis Consultancy. Overall, the Malaysian property market is expected to continue evolving in 2024, with a focus on affordability, sustainability, and innovation.

While challenges such as oversupply and affordability concerns may persist, there are also opportunities for growth and investment in emerging sectors and growth areas. By staying informed and adaptable, stakeholders in the property market can navigate these changes and capitalise on new opportunities in the year ahead.

0 Comments

The COVID-19 pandemic has wreaked havoc in the already muted real estate market. We summarise roundups for 2020 and what market trends to expect in 2021. By Khalil Adis  Expect a very subdued year in the office and retail property sectors in Malaysia for 2021. Photo: Khalil Adis Consultancy. 2020 will go down as an unprecedented year as countries around the world are faced with a global pandemic. Malaysia is no different as the Movement Control Order (MCO) and travel restrictions have adversely affected an already dampened market. According to the National Property and Information Centre (NAPIC), the property market contracted sharply in March and April due to the implementation of the MCO before picking up again in May as restrictions were eased during the Conditional Movement Control Order (CMCO) period. Here are the highlights for 2020: #1:. Steep decline in the volume of property transaction across the board  Major property markets like Kuala Lumpur, Selangor, Johor and Penang will be severely impacted. Photo: Khalil Adis Consultancy. NAPIC’s first half of 2020 data showed that the volume of property transaction declined 27.9% with 115,476 units in the first of the year compared to 160,165 units during the same period last year. Out of this, 75,318 units were those in the residential property sector which recorded a decline of 24.6%. The steepest decline was recorded in the commercial property sector which saw a 37.4% drop followed by the industrial, agricultural and development land and others at 36.9%t, 32.8 per cent and 28.6% respectively. It is hardly surprising that the Bank Negara Malaysia revised the Overnight Policy Rate (OPR) four times in 2020 itself to bring down interest rates in order to encourage consumer spending and to facilitate the application of new loans. #2: Residential overhang continued to increase  Serviced apartments in Medini, Iskandar Malaysia. Johor had the most number of overhang for high rise units. Photo: Khalil Adis Consultancy. The COVID-19 pandemic has seen the oversupply situation in the residential property sector worsening. According to data from NAPIC, there was a 3.3% (31,661 units) increase in the overhang in residential properties. Out of this, 31.7% are priced below RM300,000. 53.2% comprises high-rise units followed by landed terraced homes (29%), semi-detached & detached (12.4%), low-cost housing (1.6%) and others (3.8%). High rise units within the price range of RM500,000 to RM700,000 form the bulk of the unsold inventory at 4,144 units. Johor had the highest overhang at 19.5% followed by Selangor at 16.4%. Meanwhile, serviced apartments (which is classified as commercial property by NAPIC) recorded a 26.5% or 21,683 units increase in overhang. 61.8% are priced above RM700,000. A whopping 73.7% are located in Johor followed by 11.6% in Kuala Lumpur. #3: Majority of new launches were in the mass market segment  Low cost housing in Kuala Lumpur. Photo: Khalil Adis Consultancy. Despite the muted property market, developers continued to launch projects, particularly in the mass market segment. NAPIC’s data showed that 13,294 units of new launches were recorded in the first half of 2020. Of this, 50.1% are priced below RM300,000 while 33.7% are priced between RM300,000 to RM500,000. Landed properties dominate new launches making up 69.7% of the figure while the remaining 30.3% are stratified properties. Negeri Sembilan recorded the most launches in the entire country during the period with 2,797 units. This was not surprising as properties that are located away from Kuala Lumpur and Greater Kuala Lumpur are more affordably priced for local home buyers. #4: Steep decline in office and shopping centre occupancy rates  The MCO had a detrimental effect on office and shopping centre occupancy as many Malaysians are forced to work from home. Private office building saw their occupancy rate plunging 74.3% with only 12.70 sq m of space occupied out of the total space of 17.09 sq m. Meanwhile, shopping centres experienced the most decline at 76.7% occupancy rate. Only 9.62 sq m of space were occupied out of the total space of 12.55 sq m. #5: Malaysian House Price Index records first-ever decline, corrected slightly in Q2 2020  High-end homes in KLCC. Photo: Khalil Adis Consultancy. The mismatch between what Malaysians can afford versus what is being offered in the market, combined with the pandemic has further worsened the overhang situation resulting in an extremely muted year for developers. According to data from NAPIC, the Malaysian House Price Index stood at 198.3 percentage point in Q2 2020 after hitting a peak of 199.7 percentage point in Q12020 – the 0.7% decline is the first-ever one recorded since 2010. Nevertheless, when compared to Q1 2010 (97.25), the price index recorded an increase of 102.5 to reach 199.7 percentage point during the same period in 2020. This suggests house prices across Malaysia have been skyrocketing over the past 10 years before moderating slightly in the second quarter of 2020. Moving forward, here are the property market trends we can expect in 2021 #1: Affordable homes priced below RM500,000 will rule the market  Albury @ Mahkota Hills located in Semenyih. Photo: Khalil Adis Consultancy. As seen from data from NAPIC, majority of the new launches in the first half of 2020 are mass market homes priced below RM500,000. This trend will likely continue in 2021 especially for homes that are located in Greater Kuala Lumpur. Pricing aside, several Budget 2021 initiatives to further promote homeownership, especially for first-time buyers will spur demand for such homes. For example, the full stamp duty exemption on instruments of transfer and loan agreement for first time home buyers will be extended until 31 December 2025. The stamp duty exemptions for first residential home has been capped for homes priced RM500,000 and below. This exemption is effective for the sale and purchase agreement executed from 1 January 2021 to 31 December 2025. As such, we can expect the mass market segment to pick up momentum. #2: Rent-to-Own Scheme in the private and public housing sectors  Epic Residence offers rent-to-own scheme. Photo: Khalil Adis Consultancy. High house prices in Malaysia has resulted in both the private and public housing sectors to roll out innovative measures to make it easy for first-time home buyers. With developers under pressure to move unsold units, many will likely continue to offer attractive discounts, rent-to-own schemes and zero down payments to draw buyers. Meanwhile, in the public sector, the government will implement a Rent-to-Own Scheme by collaborating with selected financial institutions under Budget 2021. This programme will be implemented until 2022 involving 5,000 PR1MA houses with a total value of more than 1 billion ringgit and is reserved for first-time home buyers. #3: Occupancy rates for office will continue to decline  Office buildings in KLCC. Photo: Khalil Adis Consultancy. The high daily cases of COVID-19 in the country will have an adverse effect on the office occupancy rate as many companies continue to adopt a work from home policy. As such, we are likely to see their occupancy rates continue to decline until a nationwide vaccination is rolled out. Data from NAPIC showed that as of the first half of 2020, Kuala Lumpur had the highest purpose-built office existing stock at 9,266,687 units followed by Selangor and Putrajaya at 4,030,791 and 2,525,253 units respectively. Meanwhile, there will be an incoming supply of 1,465,441, 244,290 and 208,391 units in Kuala Lumpur, Johor and Selangor respectively. Collectively, this will result in downward pressure for the office market. Landlords are likely to lower their asking price to continue securing tenants. Meanwhile, corporate tenants will be spoilt for choice as there will be many good deals in the market. #4: Uncertain time for shopping centres  Pavilion Bukit Bintang. Photo: Khalil Adis Consultancy. In Q42020, several COVID-19 cases have been detected at notable shopping centres in Kuala Lumpur/Greater Kuala Lumpur such as at Nu Sentral, 1 Utama, The Gardens Mall (TGM), Mid Valley Megamall (MVM) and Bangsar Shopping Centre.

Consumer precaution will trickle into 2021 and this will have an impact on footfall as many stay away from shopping malls while the tourism market continues to suffer due to travel restrictions, further limiting footfalls from tourists and holiday-makers. Similar to the office sector, the shopping centre market will be very challenging. We will likely see the further closure of some outlets resulting in increasing vacancy rates. NAPIC’s data showed that as of the first half of 2020, Selangor had the highest shopping complex existing stock at 3,712,375 units followed by Kuala Lumpur and Johor at 3,131,431 and 2,452,258 units respectively. Meanwhile, there will be an incoming supply of 639,508, 480,125 and 167,779 units in Kuala Lumpur, Selangor and Melaka respectively. This article was first published on iProperty Malaysia. Pakatan Harapan witnessed its fourth defeat in the Tanjung Piai recent by-election suggesting Malaysians are not satisfied with the performance of the incumbent government. Against this political backdrop, here are our top five predictions for Malaysia’s property market next year. By Khalil Adis  A bird's eye view of KLCC. 2020 will be full of challenges for the property market due to the ongoing trade wars and overhang situation. Photo: Khalil Adis Consultancy. If the recently concluded by-election in Tanjung Piai is anything to go by, the mood on the ground is clear - Malaysians are frustrated with the lack of reforms, election manifestos that were rescinded, high cost of living, in-fighting among its leaders and a society that appears to be increasingly divided along race and religion fault lines. Indeed, the Tanjung Piai by-election witnessed Barisan Nasional candidate Datuk Seri Wee Jeck Seng winning by a landslide with a 15,086-vote majority. In total, he garnered 25,466 votes. In contrast, Pakatan Harapan’s candidate from Bersatu, Karmaine Sardini obtained 10,380 votes. The by-election is particularly significant as Tanjung Piai has a sizable Chinese and Malay voters. Collectively, this does not bode well as the property market is very much sentiment-driven. In addition, the latest trade data from Bank Negara showed that Malaysia’s economic growth had slowed down from 4.9 per cent in the second quarter of 2019 to 4.2 per cent in the third quarter. With a lacklustre economy, a looming global recession and job retrenchments, here are our top five predictions for Malaysia’s property market in 2020. #1: Kuala Lumpur: High-end properties in KLCC will be the first to be affected  Luxury condominiums in the KLCC area. Photo: Khalil Adis Consultancy. KLCC is a good barometer of the global economy as it attracts foreign investors, speculators and wealthy locals. It also attracts a sizeable expatriate community who are renting properties here either under a corporate or personal lease. As such, this is the first sector that will be hit once the economy comes to a grinding halt and they are sent packing home. This is because landlords who own high-end properties here are hardly able to cover their mortgage even with such tenants secured, resulting in negative cash flow. Should retrenchments occur, the exodus of the expatriate tenant pool will be a double whammy as landlords are faced with a loss of income and still having to service their mortgage. Those who face difficulties will be forced to offload their properties. Historically, the 2008 crisis witnessed the resale values of properties here declining by around 15 to 20 per cent. One solution for landlords is to convert their homes into Airbnb units. Then and again, the short-term lease market is extremely competitive and no longer as lucrative as before. There is currently a price war among online hotel booking sites and Airbnb resulting in a very low-profit margin for such property owners. #2: Kuala Lumpur: Supply glut makes renting even more attractive  A scaled model of a high-end property in Kuala Lumpur. Photo: Khalil Adis Consultancy. According to the first half of 2019 data from the National Property and Information Centre (NAPIC), entire Malaysia has a total of 54,0078 overhang units worth RM37, 229 million. Kuala Lumpur has 4,731 such units worth RM4,599.30 million. With so much supply in the market, those who are struggling to purchase their first home may want to rent instead. Alternatively, you may want to opt for the Rent-To-Own (RTO) scheme. This is specifically for those who are unable to afford the initial 10 per cent deposit and access to financing in purchasing their homes. Here’s how it works, you sign a tenancy agreement with the developer where part of your rental will be converted to your deposit. After five years, the developer will then ask you to sign a Sales & Purchase Agreement. Recently, the government announced that for Budget 2020, it will be collaborating with financial institutions for this scheme for the purchase of first home up to RM500,000 property price. Under this scheme, the applicant will rent the property for up to five years and after the first year, the tenant will have the option to purchase the house based on the price fixed at the time the tenancy agreement is signed. The government will provide stamp duty exemptions on the instruments of transfer between the developer and financial institution, and between financial institutions and the buyer in this scheme. #3: Iskandar Malaysia, Kuala Lumpur and Penang: Flight to safety among Hong Kong investors  The Light in Penang. Photo: Khalil Adis Consultancy. One man’s loss is another man’s gain. In Malaysia’s case, we have seen Hong Kong investors snapping up medium to high-end properties from Iskandar Malaysia to Penang due to the ongoing unrests happening in Hong Kong. This will also help to reduce the overhang in the property market resulting in improved cash flow among developers. These investors are cash-rich which is music to the ears for property developers. So amid the gloom and doom, the protests in Hong Kong has given a flicker of hope for the real estate sector which has been in the doldrums. The result is a positive trickle-down effect for the Malaysian economy and helping to create jobs in the property, law and finance sectors. #4: Iskandar Malaysia, Kuala Lumpur, Selangor and Penang: Affordable homes will continue to be in demand  Low-cost flats in the Pudu area. Photo: Khalil Adis Consultancy. While the government has announced various initiatives such as Fund for Affordable Homes and Youth Housing Scheme, I believe that young Malaysians should instead focus on buying from private developers through the Home Ownership Campaign (HOC). This is because land is a state matter and the federal government may have difficulty implementing such homes across Malaysia. We have already seen from the previous budgets how homebuyers were left stranded when PR1MA was not able to deliver the 1 million units that were promised. The lack of a single government agency to spearhead the affordable home segment also complicates the matter and may mean one government agency may not be communicating with another. In addition, the limitations that are imposed on low-cost housing built by either the state or federal government may impact your capital appreciation in the future. Private developers are in the business and have to means to deliver such homes. Take advantage of the HOC as you can get a 10 per cent discount for qualified properties that will be matched with stamp duty exemptions. You may also want to apply for a home jointly with your spouse or another single. This will enable you to combine your finances leading to a higher chance of getting your loans approved. This is for those who do not want to take part in the RTO scheme but instead come up with the 10 per cent deposit on your own. When choosing for a home, apply the 5CS. Check the masterplan: A masterplan would typically define a township’s development in the next one to two decades. Check the transport masterplan Generally, properties close to transportation hubs such as MRT or LRT stations can command a premium of between five and 10 per cent over the long term. Check budget allocation from the government Government policies do have an indirect impact on a property. For example, budget allocation for improvements in public infrastructure and new economic drivers will have an impact on new and existing homes in and around the vicinity of an area. So check where the government is building new hospitals or schools. Check for economic drivers You should study an area before buying your property. The best strategy is to buy in an area that is not yet developed but where there are plans for various economic drivers. A government-mooted economic corridor or a reputable developer that has experience in building townships are great indicators if the area will ‘succeed’ or not. Check for job creation This is like feeling someone’s pulse. You need to check if the township you are eyeing is going to be a ghost town or a happening place. If it is the former, perhaps you should stay away. If it is the latter, more and more workers will be drawn there, becoming a magnet for people and a hive of activity. People are the lifeblood of a neighbourhood. As the area becomes highly desirable, people will naturally want to live and work in and around the vicinity. As there is an increase in demand, property prices in that area will also rise. That is how property prices appreciate. #5: Confusing message from the government may result in a “wait-and-see’ situation among foreign investors  Pavilion Bukit Bintang is popular among the well-heeled foreigners. Photo: Khalil Adis Consultancy. Recently, the federal government had announced that it was reducing the minimum purchase price from RM1 million to RM600,000 to reduce the overhang in Malaysia’s property market.

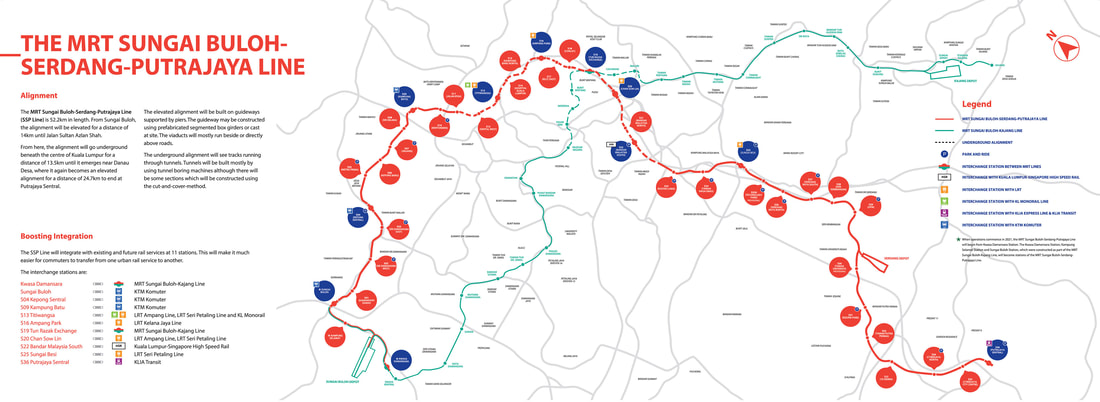

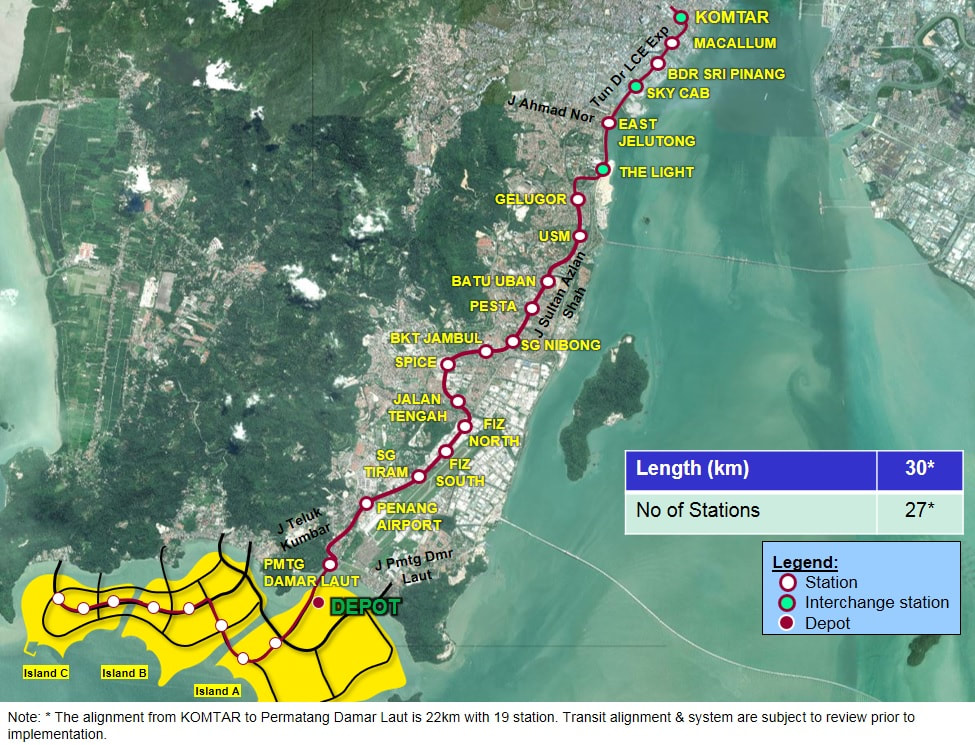

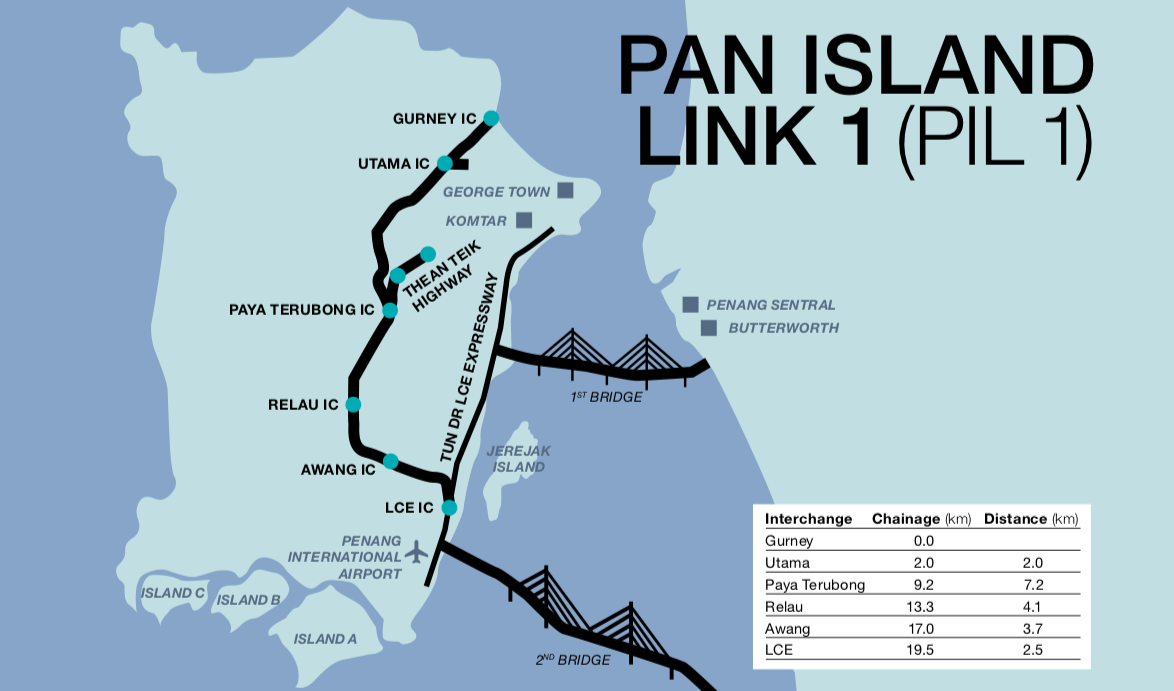

To reduce the overhang, Budget 2020 now allows foreigners to buy completed and unsold units that are priced above RM600,000. Subsequently, Housing and Local Government Minister Zuraida Kamaruddin clarified that will be implemented only for a year starting from 2020. However, each state has the right to implement its own minimum purchase price which makes the implementation difficult. In addition, Malaysian My Second Home (MM2H) applicants now can no longer import a car according to MM2H agents who are involved in such applications and will require additional approval from the Housing Ministry This, they said, results in longer processing time and sends a confusing signal to foreign investors on Malaysia’s intention to lure foreign investors. So, except for Hong Kong investors, the rest may likely adopt a wait-and-see” approach until they see some clarity. 2018 is a watershed moment for Malaysia's politics and the subsequent impact on the property market. We list down the key highlights in our 2018 property market roundups and our outlook for 2019. By Khalil Adis  The Malaysian flag, also known as Jalur Gemilang ("Stripes of Glory") against the backdrop of the recently completed Sungai Buloh - Kajang Line (SBK Line) which is a project of national importance. Photo: Khalil Adis Consultancy May 10 2018 was a watershed moment in Malaysia as it marked the first change of government in the country's history. Since 1957, it had enjoyed an uninterrupted reign from the ruling Barisan Nasional (BN) coalition. However, the high cost of living, falling Ringgit, the lack of affordable homes in the market, high unemployment among fresh graduates, the unfettered check on power and the 1MDB scandal proved to be the undoing for BN as Malaysians far and wide casted their protest vote in the ballot box The message from Malaysians is clear - they have had enough and want a new, clean government to lead the way. With the Pakatan Harapan government now in power, all eyes are on the newly elected old Prime Minister Tun Mahathir Mohamad and his team to solve the pressing bread and butter issues. Here are the top five property market roundups for 2018 and our top five outlooks for 2019. Roundups #1: Demand-supply mismatch has resulted in an increasing number of unsold homes  Luxury condominium developments surrounding the iconic Petronas Twin Towers. Malaysia is facing a housing glut in the medium to the high-end segment and a severe undersupply of affordable homes. Photo: Khalil Adis Consultancy. According to Bank Negara, 80 per cent of homes or 146,196 units priced above RM250,000 remained unsold as of end March 2018. In comparison, 130,690 units were unsold during the same period last year. "Imbalances observed in the property market continue to persist," Bank Negara had said in a statement. #2: Rent-to-own scheme being rolled out  Bukit Puchong Sales Gallery by Ayer Holdings. The developer is among one of the few offering a rent-to-own scheme for their Foreston and Epic Residence projects. Photo: Khalil Adis Consultancy To help ease the entry for the first time property buyers, the private sector has come up with a few initiatives. Some private developers like Ayer Holdings have introduced a ‘Stay & Own' scheme for their Epic Residence and Foreston projects whereby part of the rent will be converted to the downpayment. This not only provides a temporary solution for those who urgently need a home but also a form of security. Meanwhile, Maybank has rolled a similar initiative called HouzKEY which they have called as "a rent-to-own solution that helps you to own your dream home." The scheme involves zero per cent downpayment with the monthly rental forming part of the home financing. #3: Ministry of Housing and Local Government studying Singapore's HDB model  A Built-to-Order (BTO) project in Punggol, Singapore by the Housing & Development Board (HDB). Photo: Khalil Adis Consultancy. In July, Zuraida Kamaruddin, the Minister of Housing and Local Government paid an official visit to Singapore to study the HDB model. Singapore has succeeded to build demand driven homes under its Built-to-Order (BTO) scheme to house 80 per cent of the Singapore population. This is especially useful in Malaysia where there is currently a demand-supply mismatch as in point number one. #4: Malaysia looking into having a single housing government agency  The HDB Hub located in Toa Payoh. The HDB is a government housing agency that aims to provide affordable homes for all Singaporeans. Photo: Khalil Adis Consultancy In Malaysia, there are so many affordable housing programmes being rolled out by the state and federal governments such as Rumah Milik Mampu, Rumah Selangorku, PR1MA, My First Home, Program Perumaha Rakyat and the list goes on. This confuses the public. The Malaysian government is currently looking into having a single housing agency to streamline the whole process much like the HDB model. If implemented, this could solve the current Malaysian housing woe. #5: More help for the B40, M40 and first-time homebuyers under Budget 2019  Malaysians shopping for fresh produce at Pudu Wet Market in Kuala Lumpur. Budget 2019 will provide financial assistance to the targetted groups. Photo: Khalil Adis Consultancy. More help is on the way for these group of property buyers as announced under Budget 2019. The measures included the Real Estate and Housing Developers' Association (Rehda) agreement to cut prices by 10 per cent for new launches, the exemption of the Real Property Gains Tax (RPGT) for properties that are priced below RM200,000 and the stamp duty exemption for properties priced in the first RM300,000 up to RM500,000 as well as those priced from RM300,000 to RM1 million. Outlook for 2019 #1: Affordable homes to continue driving the market  Low cost housing near to Cochrane MRT station. There continues to be strong pent-up demand for affordable homes in Malaysia. Photo: Khalil Adis Consultancy. There is currently a strong pent-up demand for affordable homes but where the supply is lacking. As such, the affordable home segment will continue to be in strong demand for 2019. However, there needs to be concerted efforts from both the government and private developers. Under Budget 2019, the federal government has pledged to spend RM1.5 billion on such homes via the 1Malaysia People's Housing (PR1MA) and Syarikat Perumahan Negara Bhd (SPNB). Meanwhile, Rehda has agreed to cut prices as stated above. #2: South KL to be the growth area  The Leafz condominium located next to the Sungai Besi Highway. Southern KL is the next growth area in Kuala Lumpur. Photo: Khalil Adis Consultancy. There are many infrastructure projects and economic drivers that are in the pipeline that will further boost property prices in Southern KL. One such project is Bandar Malaysia will serve as the terminus station for the Kuala Lumpur-Singapore High Speed Rail (KL-Singapore HSR) project linking both cities in 90 minutes flat. The development for the project has been postponed to two years and will now commence construction in 2020 instead of 2018. Meanwhile, the express service will only commence by 1 January 2031 instead of 31 December 2026, as originally planned. Bandar Malaysia has been designated as a site for the Digital Free Trade Zone (DFTZ) initiative by Jack Ma. Home to the Satellite Services Hub, DFTZ is expected to create some 60,000 direct and indirect jobs. It will also possibly serve as the interchange to the MRT Line 3, which has now been postponed. Another economic driver in the vicinity is Tun Razak Exchange (TRX). TRX will be a mixed-use development comprising a Grade A office space as well as residential and commercial precincts. To be developed in several phases over a period of 15 years, the first phase will comprise four investment grade A office towers, a lifestyle retail mall, two 5-star hotels and up to six luxurious residential towers with a target completion date by 2019. In addition, Bandar Malaysia will house two MRT stations - Bandar Malaysia North and Bandar Malaysia South which will form part of the alignment for the Sungai Buloh - Serdang - Putrajaya Line (SSP Line). #3: Properties along Sungai Buloh - Serdang - Putrajaya Line (SSP Line) will be sought after  The alignment of the station along the SSP Line. Map: MRT Corp. Speaking of the SSP Line, properties along the alignment, particularly those situated in the growth areas of Sungai Besi, Bandar Malaysia and Cyberjaya City Centre are worth looking into. Bandar Malaysia will house two MRT stations as stated above and located a few stops away from Tun Razak Exchange MRT station. Meanwhile, Sungai Besi MRT station is an interchange station to the Sungai Besi LRT station. It will serve as an interchange to the upcoming High Speed Rail station located in Bandar Malaysia, also in Sungai Besi. Last but not least, Cyberjaya City Centre MRT station is a transit-oriented development (TOD) project to be developed by Malaysian Resources Corp Bhd (MRCB). With its experience in building the transport hub in KL Sentral, MRCB will be developing a new city that will be integrated with the MRT station. Phase one is expected to generate a gross development value (GDV) of RM5.35 billion. It will feature a 200,000 sq ft convention centre, a 300- to 400-room business hotel, low and high-rise office buildings and a retail podium. Cyberjaya City Centre will have a development plan spanning 20 years. The MRT station is located just opposite Lim Kok Wing University of Creative Technology. #4: Penang to get a boost from Phase 1 of Penang Transport Master Plan (PTMP)  Ferry service from Georgetown to Butterworth. Soon, there will be more transportation options on the island. Photo: Khalil Adis Consultancy. With Lim Guan Eng as Malaysia's Finance Minister, Penang's property market will get a further boost. Just this month, Phase 1 of PTMP was approved. It will comprise the Bayan Lepas Light Rail Transit (LRT) project, Pan Island Link 1 (PIL1) project and several main highways. The proposed Bayan Lepas LRT line will be about 30 km in length with 27 stations running from KOMTAR to the future reclaimed islands in the south. There will be three interchange stations - KOMTAR, Sky Cab Station linking it to the Sky Cab line across the Malacca Straits and The Light Station linking it to the George Town-Butterworth LRT line. The LRT Line will also be integrated with the Sungai Nibong Express Bus Terminal at the Sungai Nibong Station. Meanwhile, PIL 1 is a new 20km highway that will be aligned along the mountainous terrain of the island and will take around 15 minutes from between Gurney Drive to the Second Bridge. There will be six interchanges in all - Dr Lim Chong Eu Expressway (LCE), Awang, Relau, Paya Terubong, Utama and Gurney. #5: Johor Bahru to get a boost from the Rapid Transit System (RTS) Link  View of the Woodlands Checkpoint from the KTM service playing the Johor Bahru - Woodlands route. Soon, commuters can take the MRT from Bukit Chagar to Woodlands North MRT station instead. Photo: Khalil Adis Consultancy. Meanwhile, over in the southern state of Johor, Iskandar Malaysia's muted property market will get a boost as the RTS Link will commence construction next year.

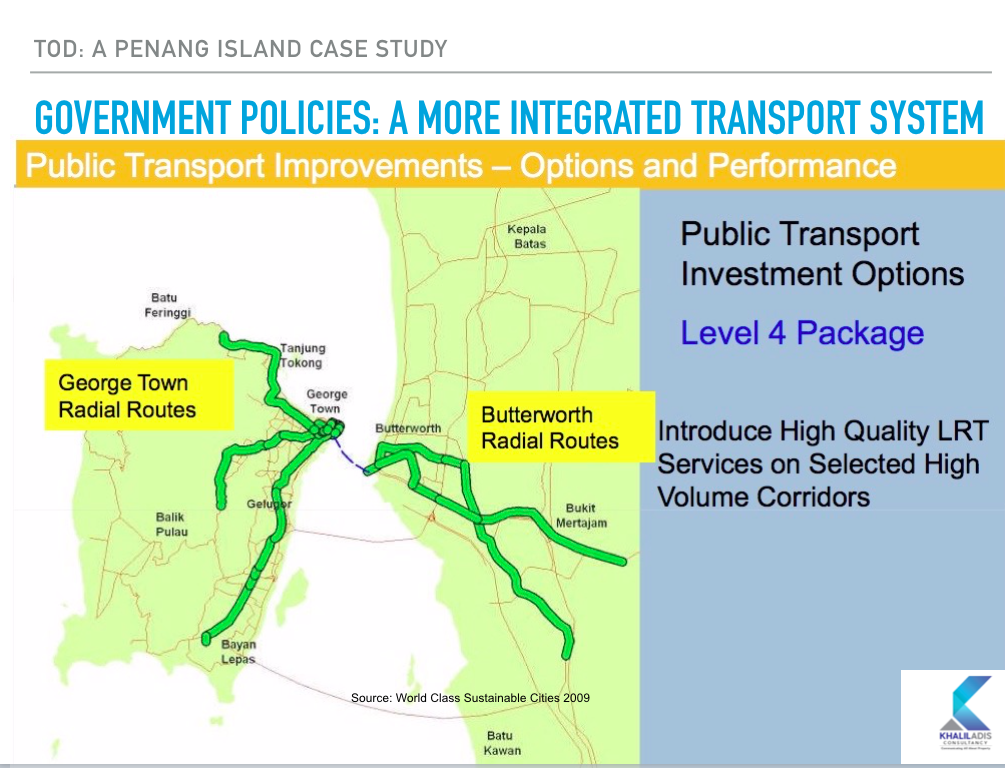

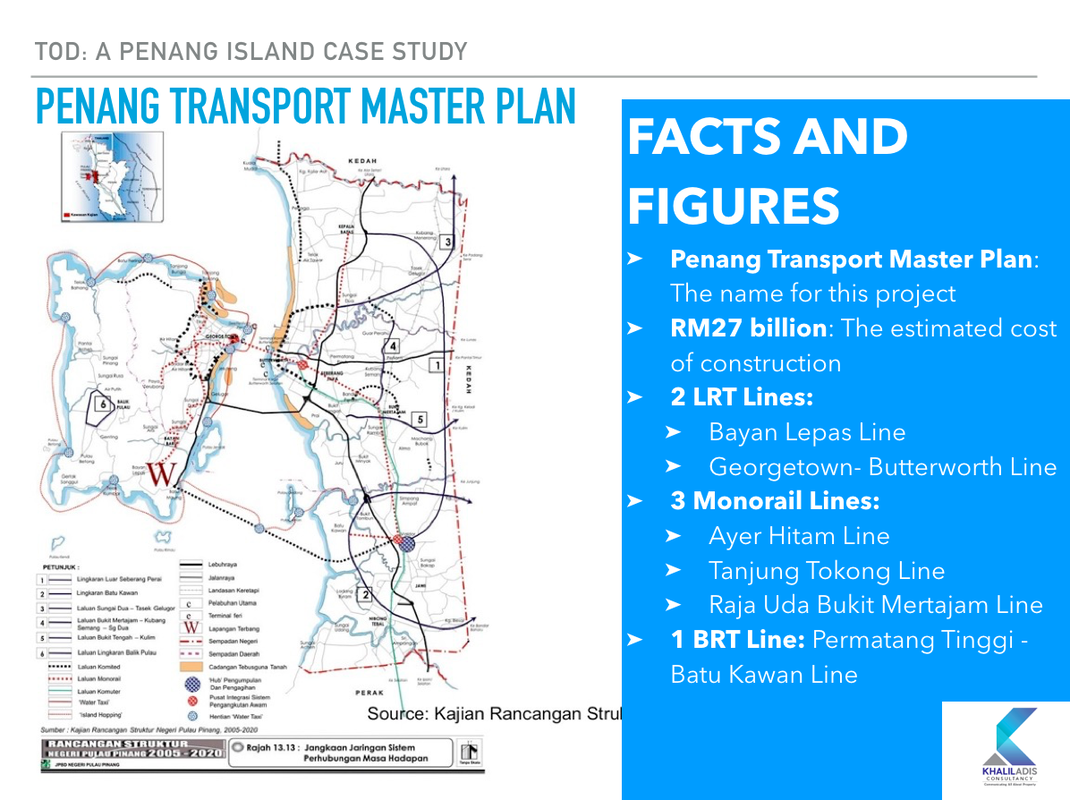

The RTS Link will link Bukit Chagar station in Johor Bahru to Woodlands North MRT station in Singapore when completed in 2024. There are also plans for a Bus Rapid Transit (BRT) system within Bukit Chagar station to link it to the different areas of Iskandar Malaysia. The BRT will feature a dedicated bus lane with three lines - BRT Line 1 will span from Bukit Chagar to Tebrau, BRT Line 2 from Bukit Chagar to Senai and finally, BRT Line 3 from Bukit Chagar to Iskandar Puteri. However, based on market talk in the ground, there is a possibility that the BRT system will be upgraded to an LRT system instead. Phase 1 of Penang Transport Master Plan (PTMP) is now approved. Here are the 6 key takeaways11/14/2018 You can soon hop onto the train from Penang International Airport to KOMTAR or take the highway to Gurney Drive in 15 minutes flat. By Khalil Adis  Rapid Penang bus service which runs from Penang International Airport to KOMTAR. Soon, you can hop onto the train instead to Georgetown. Photo: Khalil Adis Consultancy With the Phase 1 of Penang Transport Master Plan (PTMP) now approved, the Pearl of the Orient is set to scale to greater heights. Prior to the Malaysian general election, it looked as though the project will never see the light of day as Penang falls under the opposition state of the Democratic Action Party (DAP) while the federal government was run by Barisan Nasional (BN). However, now that its former Chief Minister Lim Guan Eng is the current Finance Minister under the Pakatan Harapan government, the project is finally gaining traction. Here are six interesting facts on Phase 1 of PTMP #1: PTMP exempted from major review  The Penang Transport Master Plan. Graphics: Khalil Adis Consultancy & World Class Sustainable Summit 2009. It is interesting to note that while other mega-projects such as the East Coast Railway Line (ECRL), High Speed Rail (HSR), Forest City, MRT Circle Line and Light Rail Transit Line 3 (LRT3) were under review, PTMP is the only one that managed to escape unscathed. This is definitely good news for Penangites and for the property market as such infrastructure project will further boost property prices on the main island and on the Seberang Perai and Batu Kawan areas. #2: Phase 1 to comprise an LRT line and several main highways  Phase 1 will comprise the Bayan Lepas LRT line from Penang International Airport to KOMTAR and several highways on the island. Graphics: Khalil Adis Consultancy The PTMP estimated cost is around RM46 billion and comprises two LRT Lines - Bayan Lepas Line and Georgetown- Butterworth Line, three Monorail Lines - Ayer Hitam Line, Tanjung Tokong Line and Raja Uda Bukit Mertajam Line and one BRT Line - Permatang Tinggi - Batu Kawan Line. Phase 1 of PTMP will comprise the Bayan Lepas Light Rail Transit (LRT) project, Pan Island Link 1 (PIL1) project and several main highways. #3: Bayan Lepas LRT line to have 27 stations (including three interchange stations)  Screen grab of the Bayan Lepas LRT line. Source: http://pgmasterplan.penang.gov.my The proposed Bayan Lepas LRT line will be about 30 km in length with 27 stations running from KOMTAR to the future reclaimed islands in the south. The line will pass through important landmarks such as KOMTAR, Bayan Lepas Free Industrial Zone (FIZ) and the Penang International Airport as well as several established and planned residential townships and employment hubs in Jelutong, The Light, Gelugor, Batu Uban, SPICE in Bayan Baru, Sg Tiram and Batu Maung. There will be three interchange stations - KOMTAR, Sky Cab Station linking it to the Sky Cab line across the Malacca Straits and The Light Station linking it to the George Town-Butterworth LRT line. The LRT Line will also be integrated with the Sungai Nibong Express Bus Terminal at the Sungai Nibong Station. #4: Pan Island Line 1 to have six interchanges  Screen grab of the Pan Island Link 1 showing the interchanges. Graphics: http://pgmasterplan.penang.gov.my Meanwhile, the PIL 1 is a new 20km highway to alleviate the heavy traffic load on the Tun Dr Lim Chong Eu Expressway (LCE) and adjacent arterials such as Pengkalan Weld, Jalan Masjid Negeri, Jalan Jelutong and Jalan Sultan Azlan Shah. According to the Penang state government's website, "it is designed with six interchanges to link highly-populated areas and transport hubs on the island from the Second Bridge and the Penang International Airport all the way towards George Town, Paya Terubong, Bayan Baru, and Relau." The six interchanges include LCE interchange, Awang interchange, Relau interchange, Paya Terubong Interchange, Utama Interchange and Gurney Interchange. #5: A travel time of 15 minutes  Aerial view of Penang island. The Pan Island Link will cut through the mountainous terrain of the island. Photo: Khalil Adis Consultancy Upon completion, PIL 1 will be aligned along the mountainous terrain of the island and will take around 15 minutes from between Gurney Drive and the airport, compared with the current 45 minutes under normal traffic conditions on the Tun Dr Lim Chong Eu Expressway (LCE). #6: Toll-free  Aerial view of the Second Bridge. Unlike this bridge, the Pan Island Link 1 will be toll-free. Photo: Khalil Adis Consultancy Good news for drivers as the the 20km highway will be toll-free with limited points of access.

This it to ensure certainty in speed and travel time over the entire length of the highway. The alignment along the mountainous terrain also avoids the possibility of congestions caused by future developments. Funding will be from the sale of reclaimed land owned by the Penang state government |

Khalil AdisAn independent analysis from yours truly Archives

July 2023

Categories

All

|

RSS Feed

RSS Feed

100 Peck Seah Street

|

|