- Published on

By Khalil Adis

Kuala Lumpur's city skyline. Photo by Khalil Adis.

“Where should one even begin?” I wondered.

As I navigated the complex property market and started speaking to various analysts and market leaders, I realised there are a few key cities that have seen consistent demand among both local and foreign investors.

I had also assumed that, like Singapore, high-rise residential apartments were the most popular property type in Malaysia.

This is a common mistake that many Singaporean investors make.

However, when you speak to locals, many would prefer living in a freehold landed terraced home.

These are just some of the nuances one must grasp when understanding the Malaysian property market.

Fast forward to 2025, these key cities for property investments remain the same—Johor (including Iskandar Malaysia), Selangor, Kuala Lumpur, and Penang.

Here is a quick review of each market, what happened in 2024 and the predictions for 2025.

Kuala Lumpur: A city of opportunities and challenges

The busy intersection of Bukit Bintang, Kuala Lumpur. Photo by Khalil Adis.

With its favourable exchange rate, exciting nightlife, unrivalled shopping experience, delicious local foods and tourist attractions, it is no wonder Kuala Lumpur remains a perennial favourite among Singaporean and local investors.

However, Kuala Lumpur also has its share of challenges, which many investors may not be aware of.

According to data from the National Property Information Centre (NAPIC), of the total 22,642 overhang units in Malaysia as of the first half of 2024, Kuala Lumpur had the third-highest residential overhang status in the country at 3,051 units.

In Kuala Lumpur, these unsold units are comprised mainly of condominiums and apartments.

According to NAPIC, in terms of value, Kuala Lumpur recorded the highest overhang value, with RM3.06 billion worth of unsold units.

Across Malaysia, properties priced at more than RM1 million contributed to 12.0 per cent (2,719 units) of the national total.

Since the minimum purchase price for a foreign investor in Kuala Lumpur is RM1 million, imagine the intense competition you may face in the resale market if you decide to offload your property.

The sheer number of unsold units compared to what Malaysians can generally afford (below RM300,000) means you might have to either sell your property at a loss or wait a long time for the right buyer.

The oversupply of condominiums and apartments also affects rental income.

Rental market trends in Kuala Lumpur

According to listings on PropertyGuru Malaysia, two-bedroom condominium units in KLCC have an average asking rental price of RM3,000 per month.

Assuming your mortgage payments amount to RM3,700, your rental income alone would not be sufficient to cover your property upkeep and other expenses.

Likewise, rental yields may not be as attractive.

For example, an RM1 million unit rented out at RM3,000 per month would generate a rental yield of 3.6 per cent.

For better rental yields, investors should consider buying near transportation hubs like the newly constructed Kajang MRT Line, Putrajaya MRT Line, LRT stations, and educational institutions.

These areas tend to have high foot traffic and excellent connectivity, making them desirable for renters.

Selangor: The heartland of Malaysia’s property market

Border crossing in Malaysia demarcating the state of Selangor and Kuala Lumpur. Photo by Khalil Adis.

Think of it as Kuala Lumpur’s heartland, similar to Singapore’s Punggol or Ang Mo Kio, where property prices are significantly lower than in the city centre.

Over the years, Selangor has benefited from several federal government-initiated transportation projects that have positively impacted the property market.

These include the Kajang MRT Line and Putrajaya MRT Line.

While property prices in Selangor are more affordable, there is a catch—the minimum purchase price for foreigners is RM2 million.

This presents a conundrum.

If offloading a RM1 million property in KLCC is already challenging, selling a RM2 million one further from the city centre becomes even more difficult.

To put it into Singaporean terms, it is like trying to sell a S$2 million condominium in Punggol and hoping a local buyer living in a S$500,000 four-room flat will upgrade.

Similarly, within Selangor, the price gap between what locals can afford and what foreigners must pay is substantial.

Also, most locals would prefer to buy a freehold landed property for the same price.

Rental market trends in Selangor

Selangor does, however, present a vast rental market.

According to NAPIC, all districts recorded modest growth in rental rates for terraced houses and high-rise units, particularly in Petaling, Klang, Hulu Langat, and Gombak.

Given the preference for landed homes, it is not surprising that such properties in select areas saw higher rental rates.

For instance, NAPIC data showed that double-storey terraces in urban centres such as Mutiara Damansara, Bandar Utama, Subang Jaya, and Bandar 16 Sierra had rental rates ranging from RM2,200 to RM2,800 per month.

Meanwhile, similar houses in Setia Eco Templer, Taman Alam Sari, and Setia Eco Glade recorded higher rental rates between RM2,500 and RM3,900 per month.

Notably, these are all township developments located away from the city centre in Rawang, Bangi, and Cyberjaya, respectively.

Johor: A promising start that fizzled out

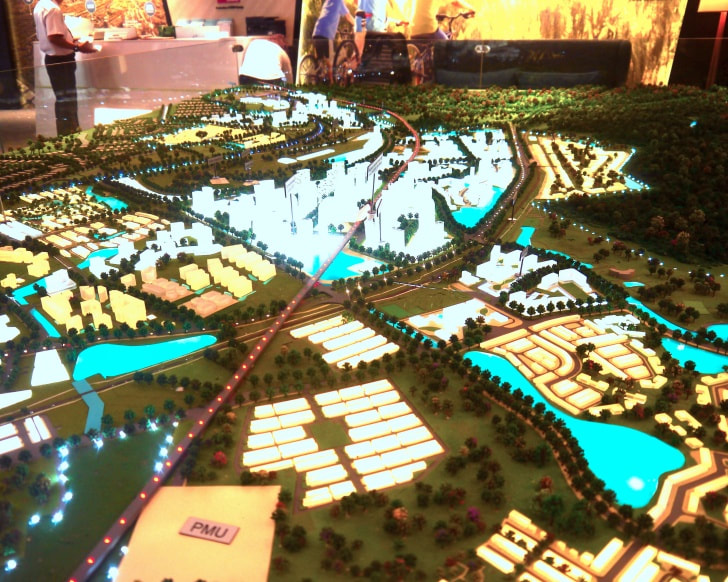

Scaled model showing the proposed High-Speed Rail station for Gerbang Nusajaya's master plan. Photo by Khalil Adis.

I recall attending a media site visit where officials from the Iskandar Regional Development Authority (IRDA) and Iskandar Investment Berhad (IIB) presented their master plan for Flagship B, showcasing catalytic industries such as Islamic finance, education, tourism, creative, and high-tech manufacturing.

At the time, the vision was impressive.

Yet, many Singaporeans I interviewed remained skeptical.

By 2013, however, interest in Iskandar Malaysia surged among Singaporean investors, especially after Temasek Holdings announced its investment in Danga A2 Island through CapitaLand Malaysia Pte Ltd.

However, somewhere along the way, the master plan changed beyond recognition.

Massive high-rise developments sprang up along Danga Bay and near the Second Link, particularly with the introduction of Forest City.

Market analysts began sounding alarms about oversupply, questioning the sustainability of Johor’s property market.

Fast forward to 2025, and the numbers from the National Property Information Centre (NAPIC) paint a concerning picture. Johor recorded the second-highest number of overhang units in Malaysia, with 3,219 unsold residential properties valued at RM2.80 billion—mostly condominiums and apartments.

That equates to an average price of RM869,835 per unit, a figure far beyond the reach of most Johoreans.

Johor Housing and Local Government Committee Chairman Datuk Mohd Jafni Md Shukor recently reported that Johor experienced over 15 per cent growth in overall property sales, including sales of previously overhung properties.

As of December 2024, Johor has 102,438 serviced apartment units, with 11,810 remaining unsold.

Despite these challenges, NAPIC data showed strong growth in serviced apartment transactions, with a 47.4 per cent increase in volume (6,804 transactions) and a 68.5 per cent rise in value (RM4.94 billion) in the first half of 2024 compared to the same period in 2023.

By state, Johor and WP Kuala Lumpur led the market, capturing 36.2 per cent (2,465 transactions) and 33.0 per cent (2,245 transactions) of the national total, respectively.

Yet, the 11,810 unsold units will continue to impact the resale and rental markets in the foreseeable future.

Rental market trends in Johor

Data from NAPIC revealed that Johor’s rental market remained stable, with mixed movements in urban centres such as Johor Bahru, Kulai, and Batu Pahat.

Due to their limited supply, landed terraced homes continue to perform better in the rental market.

For instance, double-storey terraced homes in Horizon Hills and Taman Laguna fetch between RM2,200 and RM3,000 per month.

With the upcoming Johor-Singapore Special Economic Zone (JS-SEZ) and the RTS Link, areas like Bukit Chagar, JB Sentral, and the Ibrahim International District may experience renewed investor interest.

However, legal complications in Medini and continued concerns over the oversupply of high-rise units remain as cautionary factors.

Penang: The island effect

Waterfront developments against a hilly backdrop near Gurney Drive. Photo by Khalil Adis.

I remember spending nearly a week on the island, photographing developments and interviewing key developers, including SP Setia and IJM Land (which was then developing The Light).

Previously governed by the United Malays National Organisation (UMNO), Penang’s development accelerated under the Democratic Action Party (DAP).

A small but significant change caught my eye—Penang had started cleaning up its act.

For instance, Gurney Drive, once littered with rubbish, is now clean and well-maintained.

With George Town being recognised as a UNESCO World Heritage Site in 2008 and the launch of the George Town Festival in 2010, Penang’s appeal among tourists and investors has skyrocketed.

There is an unmistakable sense of pride among Penangites in preserving the historic city of George Town.

Similar to Singapore, Penang faces land scarcity and pent-up housing demand, which have driven up property prices—commonly referred to as the “island effect.”

However, unlike Singapore which is relatively flat, Penang has a hilly inner terrain making most parts of it unsuitable for development.

This, together with local regulations that prohibit developments from taking place on these hilly terrains, has resulted in very little land available for housing developments.

The scarcity of land versus the increase in demand for homes in Penang has brought about a spike in prices.

As a result, property prices are increasingly out of reach for locals, while foreign investors view Penang as an affordable retirement destination due to the lower cost of living.

According to NAPIC, recent easing of Malaysia My Second Home (MM2H) requirements has helped attract more foreign investors to Penang.

Key investment hotspots in Penang

Menara KOMTAR in George Town. Photo by Khalil Adis.

- Tanjung Bungah

- Tanjung Tokong

- Batu Ferringhi

- George Town

- Queensbay

- Gurney

Property overhang in Penang

Luxury condominiums along Gurney Drive. Photo by Khalil Adis.

With 8,168 units in the supply pipeline (including overhang, unsold under construction, and unsold not constructed), high-rise residential resale and rental markets are expected to remain competitive.

Penang’s rental market

Data from NAPIC shows Penang’s rental market has remained stable, with mixed movements in various districts.

Notably, single and double-storey terraced houses in Southwest Penang saw rental increases of 4.5 per cent to 10.0 per cent, with rentals reaching up to RM2,000 per month.

Moving forward, landed residential properties in Penang are likely to outperform high-rise units, given the strong local demand and limited land supply.

What happened in 2024?

Low cost housing project in Kuala Lumpur called Program Perumahan Rakyat (PPR). Photo by Khalil Adis.

According to data from the National Property and Information Centre (NAPIC), homes priced at RM300,000 and below accounted for 53.1 per cent of all residential transactions.

Overall, the residential sector recorded 121,964 transactions worth RM49.43 billion in the first half of 2024.

Compared to the same period in 2023, this marks a 6.1 per cent increase in volume and 10.4 per cent growth in value.

The boost in transactions can be attributed to various government incentives under Budget 2024 aimed at promoting homeownership, especially for first-time buyers.

One such initiative is the Housing Credit Guarantee Scheme (HCGS), which saw its funding increase from RM5 million in 2023 to RM10 million in 2024, helping up to 40,000 borrowers—particularly freelancers and gig workers—secure housing loans.

Another key measure was the RM2.47 billion budget allocation for the People’s Housing Project (PPR), also known as Program Perumahan Rakyat. This included RM546 million to continue 36 PPR projects, including a new development in Kluang, Johor.

Lastly, the government introduced a full stamp duty exemption on the instrument of transfer and loan agreements for first-time homebuyers purchasing properties priced up to RM500,000.

This exemption remains in effect until 31 December 2025.

Nationwide market performance

Landed terraced homes in Petaling Jaya, Selangor. Photo by Khalil Adis.

Johor followed, with 15.3 per cent of total transactions (18,648) and 18.2 per cent of total value (RM9.02 billion).

Together, Kuala Lumpur, Johor, Selangor, and Penang accounted for about 50 per cent of all residential transactions in Malaysia.

It is no surprise that landed terraced homes remained the most sought-after property type, making up 43.0 per cent of total transactions.

This was followed by vacant plots (15.3 per cent), high-rise units (14.3 per cent), low-cost houses/flats (10.8 per cent) and semi-detached homes (7.9 per cent)

Kuala Lumpur: Where rental growth thrives

The Oval in KLCC. Photo: Khalil Adis.

According to NAPIC, demand for double-storey terrace homes in premium areas like Damansara Heights, Desa Park City (Casaman), and Desa Sri Hartamas pushed monthly rentals beyond RM5,000.

Similarly, luxury condominiums in prime locations such as U Thant Residence, The Oval, 10 Mont Kiara, and Sunway Vivaldi recorded monthly rentals exceeding RM11,000.

Selangor: A landlord’s market

Cyberjaya in Selangor. Photo by Khalil Adis.

NAPIC data showed modest rental growth across Petaling, Klang, Hulu Langat, and Gombak, particularly for double-storey terraces in urban areas.

For example, Mutiara Damansara, Bandar Utama, Subang Jaya, and Bandar 16 Sierra saw monthly rental rates between RM2,200 and RM2,800.

Meanwhile, Setia Eco Templer, Taman Alam Sari, and Setia Eco Glade commanded even higher rentals, ranging from RM2,500 to RM3,900 per month.

Notably, these are township developments located outside central Kuala Lumpur, in Rawang, Bangi, and Cyberjaya.

Johor: A market under scrutiny

Medini in Iskandar Malaysia, Johor. Photo by Khalil Adis.

At the time, it seemed like a groundbreaking initiative, but over the years, bureaucratic and administrative setbacks began to surface.

In November 2024, I received a tip-off from a Singaporean buyer at Iskandar Residences who revealed shocking issues regarding property ownership in Medini.

In the documents seen, the individual strata titles that was issued nearly a decade later, showed that instead of the buyer being the legal owner, the title was still under Iskandar Investment Berhad (IIB).

This has now escalated into a legal battle, with 63 plaintiffs suing the developer, Distinctive Resources Sdn Bhd and the landowner, IIB, for fraudulent misrepresentation.

According to the source, around 10,000 homes within Medini do not have any strata title.

Given the Johor-Singapore Special Economic Zone (JS-SEZ) is being actively promoted, this controversy could shake investor confidence in Johor’s property market.

Johor’s rental market

An advertisement for a unit at 1 Medini. Photo by Khalil Adis.

Limited supply helped double-storey terraces in Horizon Hills and Taman Laguna fetch RM2,200 to RM3,000 per month.

Penang: Stability in the face of change

Charming shophouses in George Town, Penang. Photo by Khalil Adis.

According to NAPIC, Southwest Penang saw rental increases of 4.5 per cent to 10.0 per cent, with single and double-storey terraced houses fetching up to RM2,000 per month.

Moving forward, landed homes are expected to outperform high-rise units due to strong local demand and limited land supply.

Predictions for 2025: Where should you buy in Malaysia?

Kajang MRT station along the Kalang Line. Photo by Khalil Adis.

Why? This is because history has shown us that when new train lines, highways or economic zones are introduced, property prices in those areas tend to skyrocket.

It has happened before in places like KL Sentral and even parts of Iskandar Malaysia.

However, knowing where to buy is the tricky part.

Some areas will see real growth while others may remain stagnant for years.

That is why I have put together this guide—to help you cut through the noise and make a smart, informed decision.

Let us start with Johor.

Johor: Can it deliver?

Sultan Iskandar CIQ. Photo by Khalil Adis.

Needless to say, while I enjoyed it, it was a frustrating and exhausting experience.

Sometimes, it can take up to five hours just to cross the border.

It also made me wonder—will Johor ever become more than just a commuter town?

Fast forward to today, things are finally starting to change.

For example, the Johor-Singapore Rapid Transit System (RTS) Link is finally taking shape (like finally!), promising to slash travel time between JB and Singapore to just five minutes when it launches in 2026.

No more endless border queues that I used to endure!

If this were to actually happen as planned, areas like Bukit Chagar, JB Sentral, and the Ibrahim International District could see a huge surge in demand —for both homes and businesses.

The Land Transport Authority (LTA) estimates that it will carry up to 10,000 commuters per hour, in each direction, during peak times.

That means a massive boost for businesses, rental demand and home values in the surrounding areas.

Meanwhile, there is another interesting development: a new data center in Iskandar Puteri.

Telekom Malaysia and Singapore’s Nxera are working together to build this next-generation facility, which is set to be completed by 2026.

If Iskandar Puteri positions itself as a tech hub, we could see more high-paying jobs in the area—and with that, a stronger property market.

Broken promises?

The former Pinewood Iskandar Malaysia Studios. Photo by Khalil Adis.

For example, the much hyped about Bus Rapid Transit (BRT) has now been canceled.

Let us also not forget the high-profile government-to-government project, the Kuala Lumpur-Singapore High-Speed Rail (HSR) which has been scrapped (for now).

Finally, the Iskandar Malaysia much anticipated boom has delivered very mixed results.

Remember Sanrio Hello Kitty Town, Lat’s Place at Puteri Harbour and Pinewood Iskandar Malaysia Studios?

They are all gone.

What about the dismal footfall at Mall of Medini and eerily quiet neighbourhoods in certain parts of Iskandar Puteri and Medini when night falls?

Speaking of Medini, the ongoing court case involving Iskandar Residences in Medini has some buyers worried about whether the area is as investment-friendly as once promised.

Should you invest in Johor?

Gated and guarded landed homes called Estuari by UEM Sunrise in Iskandar Puteri. Photo by Khalil Adis.

If you are willing to bet on Johor’s long-term potential, focusing on areas near the RTS Link and major commercial projects could pay off.

Owner-occupied landed terraced homes (particularly gated and guarded) could also provide good capital gains over the long-term.

However, if you’re looking for a safe, guaranteed investment, you might want to wait out until the whole Medini debacle is resolved.

Kuala Lumpur: Is it still worth buying?

KL Sentral Monorail station. Photo by Khalil Adis.

Why? First, property prices here are high, with a median resale price of RM610,000—a steep entry point for most young buyers.

Second, KL is already a mature market, meaning there is limited room for rapid price appreciation compared to up-and-coming areas.

That said, if you are an investor looking for rental opportunities, certain areas—especially those along new MRT lines—still have potential.

My advice? Follow the infrastructure.

Where to look: The Putrajaya Line

Kepong Sentral: A hidden gem with industrial demand

This isn’t just another train stop—it is an interchange for the KTM Komuter Port Klang Line and serves one of KL’s most well-connected suburban hubs.

With plenty of industries (plastics, printing, electronics), demand for rental housing is strong.

Expect to find a mix of medium-cost apartments, terraced homes, and semi-Ds—good for both investors and homeowners.

Kampung Batu: Affordable & well-connected

One of the most underrated areas along the MRT line!

This interchange for the KTM Batu Caves-Gemas Line links multiple townships (Kampung Batu, Sentul, Taman Kok Lian).

Housing is mostly affordable (low to mid-cost apartments and terraced homes), but there is solid demand due to amenities like Victoria International College and local eateries.

Titiwangsa: The ultimate transit hub

If there is one place in KL that is a connectivity powerhouse, this is it.

Titiwangsa is an interchange for MRT, LRT, KL Monorail, and the Pekeliling Bus Hub, making it a commuter’s dream.

It is also a prime location for short-term rentals with nearby hospitals (Hospital Sentosa, Damai Service Hospital) and MICE venues (PWTC and major hotels).

If you are eyeing serviced residences and condos, Titiwangsa could be a long-term winner.

Ampang Park: The OG prime area

Ampang Park MRT is an interchange for the LRT Kelana Jaya Line, sitting right next to KLCC.

The skyline here is packed with luxury condos like The Troika and Binjai Residency—meaning it’s great for high-end investors but not first-time buyers.

Tun Razak Exchange (TRX): Malaysia’s Wall Street?

TRX is not just a MRT stop—it is Malaysia’s answer to Hong Kong’s Central or Singapore’s Marina Bay Financial District.

With a GDV of RM40 billion and major banks setting up HQs here, commercial demand is booming.

Residential property here will not be cheap, but if you can afford to buy early, you could ride the wave of appreciation.

Sungai Besi: Future-proof or a planning nightmare?

While Sungai Besi links to the upcoming KL-Singapore HSR station, the area has serious urban planning issues—limited walkability, poor pedestrian access, and scattered development.

Connectivity here is a nightmare!

How do I know this? Because I used to live there.

Residents from 1 Petaling and Petaling Indah Condo already struggle to access transit.

Unless major infrastructure upgrades happen, investing here is a risky bet.

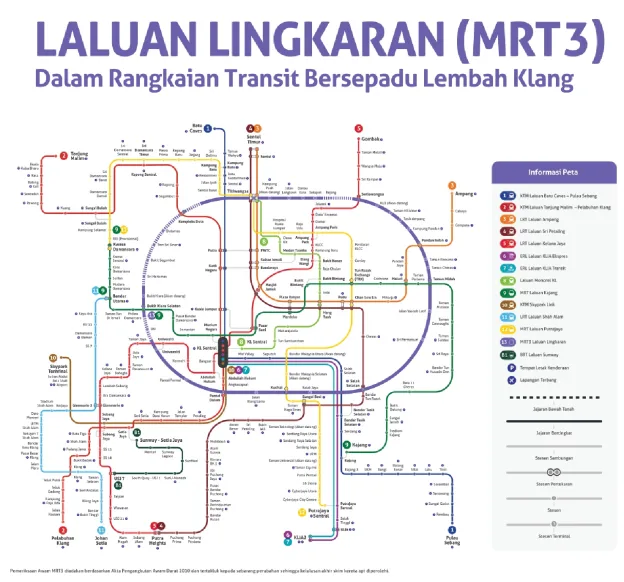

MRT 3 Circle Line: The game changer?

Screengrab showing the Circle Line taken from MRT Corp's website.

Hotspots along MRT 3 include:

- Bukit Kiara Selatan

- Kompleks Duta

- Titiwangsa

- Setiawangsa

- Pandan Indah

- Taman Midah

- Salak Selatan

- Kuchai

- Pantai Dalam

- Universiti

Why these areas?

Properties near transit hubs and educational institutions historically appreciate faster and attract strong rental demand.

Selangor: Shifting my 2025 predictions

Stadium Kajang MRT station. Photo by Khalil Adis.

However, due to delays in the KL-Singapore HSR and Malaysia Vision Valley, I am revising my forecast.

Thus, the new key growth areas will be along the Kajang Line, Putrajaya Line and LRT Shah Alam Line.

Kajang Line: Where are the investment hotspots:

Kwasa Damansara: The next KL Sentral?

This 2,330-acre township is KL’s next big mixed-use hub.

Think KL Sentral… but at a much earlier (and more affordable) stage of development.

With 30 per cent designated for housing and 70 per cent for commercial, prices here are still reasonable—but this will not be for long.

Kwasa Sentral: TOD living at its best

Part of Kwasa Damansara, but expect higher property premiums due to its centrality.

Meanwhile, its Park N’ Ride integration will attract car-owning professionals who commute to KL.

Bukit Dukung: The smart investor’s choice?

With Universiti Putra Malaysia (UPM) and the German-Malaysian Institute (GMI) nearby, this area attracts students and working professionals.

Savvy investors should look into auction properties (BMV), which can go for as low as RM100,000–RM200,000.

Stadium Kajang: Rising property demand

Stadium Kajang MRT station serves several townships, including Taman Sri Kantan, Taman Sri Jambu, Taman Bunga Raya, Taman Sri Kajang, and Taman Kajang Baru.

With enhanced connectivity, land here has become highly sought after.

As a result, developers like Gamuda and Country Heights have launched medium- to high-end township developments in the area.

Some notable projects include Jade Hills, Prima Paramount and Country Heights.

The Kajang MRT Line has significantly improved access to Kuala Lumpur, making Kajang an attractive location for both homeowners and investors.

Putrajaya MRT Line

Sungai Buloh MRT Station: A key interchange hub

Sungai Buloh MRT station is a major interchange for MRT Kajang Line, MRT Putrajaya Line KTM Komuter & KTM Intercity

This station is conveniently located near ELC International School, serving upscale neighbourhoods like Bukit Rahman Putra, Damansara Damai, Bandar Sri Damansara, Valencia, Sierramas and Taman Villa Putra. With seamless connectivity to Kuala Lumpur, these areas are seeing increased demand from homebuyers and investors.

Serdang Raya South: A vibrant commercial hub

Located along the Kuala Lumpur-Seremban Highway, this station is right across South City Plaza and close to Mines Resort City.

It serves mature townships like Kampung Baru Seri Kembangan, which has a thriving commercial scene.

Established amenities here include AEON Equine Park, Giant, Maybank and McDonald's. A large overseas student population (Middle East & Africa) provides great potential for student accommodations provides strong rental demand.

UPM: A student-focused market

Located near Universiti Putra Malaysia (UPM), this station caters to a student population of over 24,000. UPM specialises in agricultural sciences and research, attracting both local and international students.

It is a good rental market as the station is near the Faculty of Medicine and Health Sciences, making it highly convenient for student.

There is a strong demand for rental properties among students and staff If you are considering investing in a unit for rental, UPM is a prime spot for student housing.

Sierra: A township with strong growth potential

Sierra MRT station is part of Bandar 16 Sierra, a township by IOI Properties located at the southern tip of Puchong.

This area is expected to benefit from two major government projects, namely KLIA Aeropolis and Cyberjaya City Centre.

The former is a multi-billion ringgit logistics and aviation hub while the latter is a smart city development in Cyberjaya

With good connectivity via the SKVE, MEX, and LDP highways, Sierra has one of the best capital appreciation potentials in Klang Valley.

Cyberjaya City Centre: The next KL Sentral?

Developed by Malaysian Resources Corp Bhd (MRCB), Cyberjaya City Centre will be a transit-oriented development (TOD) integrated with the MRT station.

Phase one is expected to generate a gross development value (GDV) of RM5.35 billion.

It will feature a 200,000 sq ft convention centre, a 300- to 400-room business hotel, low and high-rise office buildings and a retail podium.

With a 20-year master plan, Cyberjaya City Centre aims to become a major commercial and tech hub, strengthening Cyberjaya’s position as Malaysia’s Silicon Valley.

The MRT station is located just opposite Lim Kok Wing University of Creative Technology.

Putrajaya Sentral: A fully integrated transport hub

Putrajaya Sentral MRT station will be an interchange station to the Putrajaya Sentral Express Rail Link (ERL) station that links it to KLIA and KLIA2.

This station will be served by multimodal transports which include Putrajaya Monorail, a taxi centre and a bus hub, making it a fully integrated station.

As the seat of Malaysia’s government, Putrajaya has always been well-planned, but this new MRT connection will make commuting far easier for its residents.

LRT Shah Alam Line

BU11: Affluent suburban living

BU11 LRT station is located at Merchant Square, serving Tropicana and its surrounding high-end neighbourhoods.

Originally a landed residential zone, of late, however, luxury condominiums are now on the rise due to strong demand from nearby Bandar Utama and Kota Damansara.

Top developers here include Tropicana and Thriven. There is also a strong rental market as it is close to The British International School & First City University College.

Kerjaya: Industrial growth and rental demand

Located in Glenmarie, this station serves two major industrial parks.

Firstly, Hicom Glenmarie Industrial Park which is Home to Kawasaki Malaysia, DHL and other major corporations.

Secondly, Batu Tiga Industrial Park which is a light industrial zone surrounded by residential areas.

With a mix of local and expatriate professionals, there is strong demand for rental properties in Glenmarie.

Stadium Shah Alam: More than just a sports venue

Stadium Shah Alam LRT station will be built near to Shah Alam Stadium car park and will serve the Shah Alam Stadium, Stadium Malawati, the Management and Science University (MSU) campus, AEON Mall Shah Alam and the township of Taman Batu Tiga. MSU will provide a ready pool of potential tenants.

UiTM Shah Alam LRT Station: A student housing hotspot

UiTM Shah Alam LRT Station is located between Petronas and Shell petrol stations near the Federal Highway.

When completed, it will serve the Universiti Teknologi MARA (UiTM) campus and parts of Seksyen 2, specifically the nearby landed homes at Jalan Topaz 7/4.

There is a huge demand among students wanting to live off campus but within proximity to the university’s grounds.

In fact, the college management has established a Non-Resident Management Unit to help students find accommodations in Shah Alam. This presents a good opportunity if you are thinking of renting out your unit to students here.

Bukit Raja Selatan: Industrial park potential

Bukit Raja Selatan LRT Station is located within the vicinity of Bukit Raja Industrial Park and Lebuh Keluli.

The industrial area is home to multinational companies such as Nestle, Tamco Switchgear and Pharmaniaga Pristine, just to name a few.

Bukit Raja Industrial Park features modern-looking properties catering to light to medium industries.

Buying a property here means you can capture potential tenants working at the various multinational companies at the industrial park.

Pasar Jawa: The gateway to Klang and beyond

Pasar Jawa LRT Station is an interchange station that will be integrated with the Klang KTM Komuter Station serving the Port Klang Line.

When completed, it will serve Klang and its surrounding areas comprising Kampung Keretapi and Kampung Kastam. Port Klang is a shipping hub and a gateway to Malaysia.

This is the place to live if you prefer a laid-back environment. Here, you can hop onto the train and then hop off to the ferry terminal to explore Pulau Ketam or Tanjung Balai and Dumai in Indonesia. You can also find the original Little India here offering masala tea to sarees at a fraction of the price than that is offered at Brickfields.

Penang: An island that is moving up the big league

The Light by IJM Land. Photo by Khalil Adis.

There’s something magical about the island — the way George Town’s heritage charm blends with modern developments, and the undeniable pride Penangites have for their home.

It is a city that is constantly evolving, and over the years, I’ve been impressed by its rapid development.

Much like Singapore, Penang has so much untapped potential.

And finally, we’re seeing it come to life.

Would I recommend It for first-time homebuyers?

Not really.

The main island is expensive, with even far-flung areas like Balik Pulau commanding an average residential price of RM600,000.

For first-time buyers, that is a hefty sum.

However, if you’re an investor, there are some exciting growth areas—especially along new transport routes—that could see strong capital appreciation and rental demand.

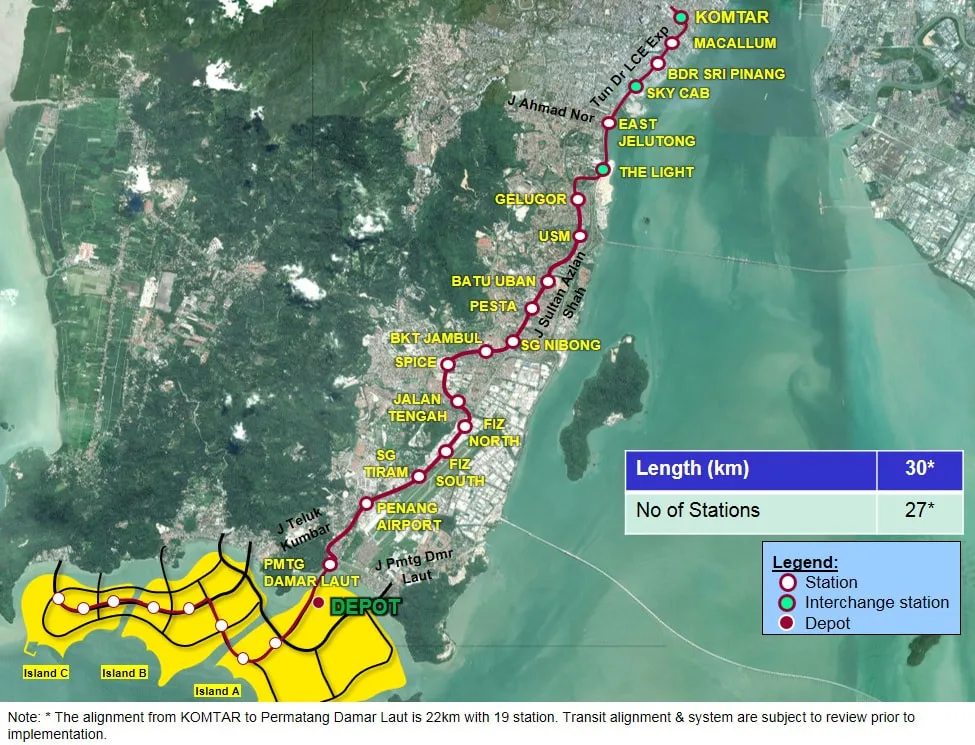

One of the key projects driving this change is the Mutiara Line (previously the Bayan Lepas LRT), which the federal government took over in 2024.

The Mutiara Line: A game-changer for Penang

The Mutiara Line will span 29.5 km with 21 stations, running from Penang South Reclamation Island A (PSR-A) to Penang Sentral and KOMTAR.

Construction kicks off in early 2025 and once completed, it will drastically improve connectivity across the island.

Here are some potential hotspots along the route:

FIZ South: Silicon Valley of the East

This station serves the Bayan Lepas Free Industrial Zone, home to major multinational corporations like Osram and Bosch.

With a strong tenant base of professionals and expats, rental demand here is expected to remain high.

Bukit Jambul: A transportation hub in the making

Bukit Jambul station will connect to the Rapid Penang Bus Hub and Bukit Jambul Complex, making it a key residential and commercial interchange.

Sungai Dua: The link to the mainland

Sungai Dua station will be an interchange to the Sungai Nibong Bus Terminal, which connects Penang to major cities like Kuala Lumpur, Singapore and Ipoh.

This makes it a prime area for rental properties catering to travelers and working professionals.

Penang Waterfront: The future Sentosa of Penang?

This station will be located within The Light development by IJM Land—think Singapore’s HarbourFront meets Sentosa.

The master plan includes luxury waterfront homes, a convention center, and even a proposed interchange for the Georgetown-Butterworth Line, connecting Penang Island to Seberang Perai.

Sungai Pinang: The Future of sky transport

Although the exact location is not confirmed, it is likely to be near Karpal Singh Drive, where it will connect to the Penang Sky Cab system.

Developed by MRCB, the Sky Cab will carry 1,000 passengers per hour, per direction, reducing ferry dependency and improving cross-strait connectivity.

KOMTAR: The beating heart of George Town

KOMTAR is Penang’s equivalent of Singapore’s City Hall MRT station (albeit a more laid-back one)—a major transport hub.

Not only does it house the Rapid Penang bus interchange but there are also plans to upgrade it into a major MRT interchange for future monorail lines connecting Tanjong Tokong and Ayer Itam.

Seberang Perai & Batu Kawan: Affordable alternatives for first-time buyers

If you are buying your first home, I would recommend looking across the strait at Seberang Perai or Batu Kawan instead.

Since the Second Penang Bridge was announced in 2006, land prices in these areas have surged—but they are still relatively affordable with plenty of upsides.

According to data from Brickz, the entry price for residential properties in Seberang Perai and Batu Kawan is RM236,500 and RM467,000 respectively.

Seberang Perai: Growth in progress

View of Seberang Perai from George Town Ferry Terminal. Photo by Khalil Adis.

In 2015, property prices averaged RM56 per sq ft.

By 2024, that figure skyrocketed to RM327 per sq ft.

There are also state-led affordable housing projects in the pipeline. You can check them out here: LPNPP

Penang Sentral: The mainland's major transport hub

Seberang Perai is home to Penang Sentral Station, which links the island to mainland Malaysia. It will serve as an interchange for KTM Butterworth, Butterworth Ferry Terminal and Rapid Penang Bus Terminal

Penang Port: A future halal logistics hub

The mainland is also positioning itself as a logistics powerhouse, with Penang Port emerging as Malaysia’s leading halal logistics hub.

There is also a proposed RM27 billion Raja Uda - Bukit Mertajam Monorail Line connecting the port to Permatang Tinggi.

Batu Kawan: The next urban hub

Once a sleepy town, Batu Kawan is now home to IKEA and township developments by EcoWorld and Mah Sing.

In 2019, property prices were RM219 per sq ft. By 2024, they had risen to RM367 per sq ft.

A Bus Rapid Transit (BRT) system is also in the works.

The BRT Permatang Tinggi - Batu Kawan Line will have 15 stations, running from Permatang Tinggi through IKEA before terminating at Bandar Cassia Industrial Park.

Should you invest in Penang?

It depends on what you’re looking for.

For first-time homebuyers, consider Seberang Perai or Batu Kawan for affordability and growth potential.

For investors, the Mutiara Line will be a key driver of capital appreciation on the island.

Areas near transport hubs like FIZ South, KOMTAR,and Penang Waterfront are promising for rental demand.

With these upcoming infrastructure projects, Penang is no longer just a cultural hotspot—it is fast becoming one of Malaysia’s most exciting property markets.

- Published on

By Khalil Adis

Kuala Lumpur city skyline. Photo courtesy of Pok Rie via Pexels.

The huge mismatch between what Malaysians can afford to buy versus what developers are building has become increasingly apparent, leading to a shift in consumer behaviour towards renting instead of buying.

With affordable housing in short supply, especially in highly urbanised areas like Kuala Lumpur, Johor, Penang, and Selangor, demand for rental properties surged in 2023.

This increased demand for rental properties has led to a notable shift in the market dynamics, with renters seeking affordable and well-maintained units in desirable locations.

In response to the changing market dynamics, developers in Johor, Selangor and Kuala Lumpur focused on catering to the mass market segment by launching new residential projects priced below RM300,000.

These mass-market homes aimed to address the growing demand for affordable housing options among Malaysian buyers.

On the other hand, the overhang market in Johor, Selangor, Kuala Lumpur and Penang was dominated by residential properties priced between RM500,000 to RM1 million.

This suggests that there is a surplus of mid-range properties in these areas, which may take longer to sell due to affordability constraints and oversupply issues.

Johor

Johor Bahru as seen from the Straits of Johor. Photo courtesy of Alix Lee via Pexels.

The mass market segment, which saw an abundance of new launches priced below RM300,000 in 2023, may experience slower growth as developers adjust to the changing demand landscape.

However, growth areas such as within Iskandar Malaysia may still present opportunities for investors, especially in well-planned integrated developments that cater to both residential and commercial needs.

Selangor

Petaling Jaya in Selangor. Photo courtesy of Deva Darshan via Pexels.

While the demand for affordable housing is likely to remain strong, developers may shift their focus towards more sustainable and inclusive development strategies.

Growth areas such as Cyberjaya, Shah Alam and Subang Jaya are expected to continue attracting interest from both buyers and developers, with a focus on mixed-use developments and transit-oriented projects.

Kuala Lumpur

Merdeka 118 tower in Kuala Lumpur. Photo courtesy of Jackson Tee via Pexels.

However, affordability concerns may lead to a greater emphasis on the development of affordable housing and innovative financing solutions.

Growth areas within the city centre and its surrounding suburbs, such as KL Sentral, Bangsar and Mont Kiara, are expected to remain attractive to both investors and homebuyers.

Penang

George Town, Penang. Photo: Khalil Adis Consultancy.

However, affordability concerns and oversupply in certain segments may lead to a slowdown in the high-end property market.

Developers may focus on niche markets and alternative housing options to cater to changing consumer preferences.

The growth areas to watch out for on the main island are mainly along the proposed Bayan Lepas LRT.

Growth areas

The growth areas in Malaysia are mainly those located near high-impact projects like MRT and transit-oriented developments. Photo: Khalil Adis Consultancy.

These areas offer opportunities for sustainable development and investment diversification, while also addressing issues such as urban sprawl and congestion.

Johor

Bukit Chagar will be located next to the Sultan Iskandar CIQ. Photo: Khalil Adis Consultancy.

One such area is Bukit Chagar which will serve as an interchange station Johor Bahru – Singapore Rapid Transit System (RTS) Link.

Slated to commence passenger service by end-2026, the RTS Link can serve up to 10,000 commuters during peak periods, for every hour and in each direction.

The RTS Link will also have a spillover impact in the nearby JB Sentral area which is home to malls, hotels and the upcoming Ibrahim International District.

Selangor

Growth areas in Southern Kuala Lumpur. Infographics: Khalil Adis Consultancy.

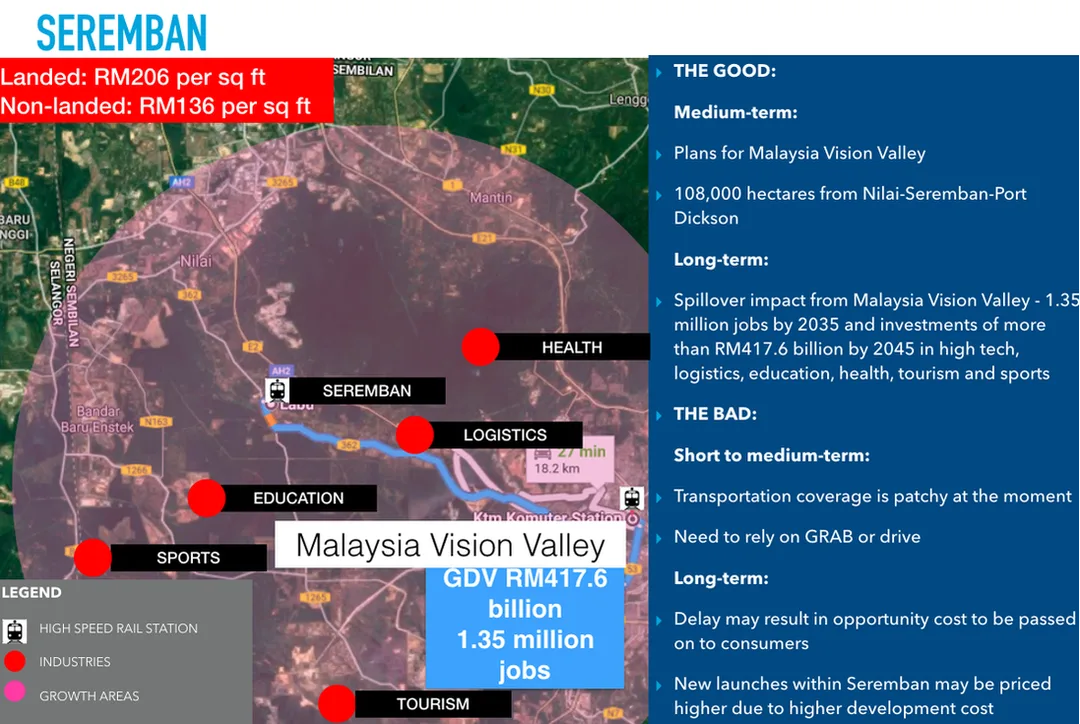

Nilai and Seremban are areas to watch out for.

Nilai is poised for further growth as it is located within the Malaysia Vision Valley. Covering Nilai to Port Dickson, it will have a proposed area of 108,000 hectares.

The upcoming industries include high-tech, logistics, education, health, tourism and sports.

The Malaysia Vision Valley is expected to create some 1.35 million jobs by 2035 and investments of more than RM417.6 billion by 2045.

To support the Malaysia Vision Valley, the Seremban HSR station will be situated in Nilai within the Labu and Kirby estates.

Major townships in the vicinity include Bandar Enstek, Bandar Ainsdale Property and S2 Height.

Seremban will be an interchange station for the Seremban Komuter Line and KTM Electric Train Service.

Kuala Lumpur

Bangsar Shopping Centre. Bangsar is one of the growth areas once the Circle Line is completed. Photo: Khalil Adis Consultancy.

Titiwangsa MRT station which will serve as an interchange station with the Ampang and Sri Petaling Line, KL Monorail Line and Putrajaya Line.

As the Circle Line is still under construction, this presents a good opportunity for genuine homebuyers to start looking in and around the station.

Homes in the secondary market will be the most ideal as they are priced cheaper than new launches.

Penang

Screen grab of the Bayan Lepas LRT line. Source: http://pgmasterplan.penang.gov.my

Since the opening of the Second Penang Bridge, Batu Kawan has seen rapid developments from several renowned developers such as EcoWorld and Tropicana as well as the opening of IKEA.

While connectivity remains patchy at Batu Kawan, there is a planned Bus Rapid Transit (BRT) system for Batu Kawan as part of the Penang Transport Master Plan.

In Seberang Perai, the growth areas will be along the planned Raja Uda-Bukit Mertajam Line to connect the northwestern region to the southeastern region.

For those who can afford to buy a property on the main island, areas along the Bayan Lepas LRT line will be the new growth corridor.

What’s in store for buyers

Landed homes are popular among Malaysians. Photo: Khalil Adis Consultancy.

Innovative financing schemes and incentives may also be introduced to encourage homeownership and address affordability concerns.

What’s in store for sellers

Aerial view of Medini and Iskandar Puteri. Photo: Khalil Adis Consultancy.

Those with properties in oversupplied segments may need to offer incentives or value-added services to attract buyers, while those in high-demand areas may continue to command premium prices.

What’s in store for tenants

A mix of high-end and low cost residential homes in Kuala Lumpur. Photo: Khalil Adis Consultancy.

Affordability remains a key concern for tenants, and they may seek out properties with flexible lease terms and inclusive amenities.

What’s in store for landlords

Bird's eye view of Kuala Lumpur. Photo: Khalil Adis Consultancy.

Those with properties in growth areas may continue to enjoy strong rental yields and capital appreciation.

Conclusion

Brickfields, Kuala Lumpur. Photo: Khalil Adis Consultancy.

While challenges such as oversupply and affordability concerns may persist, there are also opportunities for growth and investment in emerging sectors and growth areas.

By staying informed and adaptable, stakeholders in the property market can navigate these changes and capitalise on new opportunities in the year ahead.

- Published on

By Khalil Adis

Taman Connaught MRT station along the Sungai Buloh - Kajang MRT Line (SBK Line). Photo: Khalil Adis Consultancy

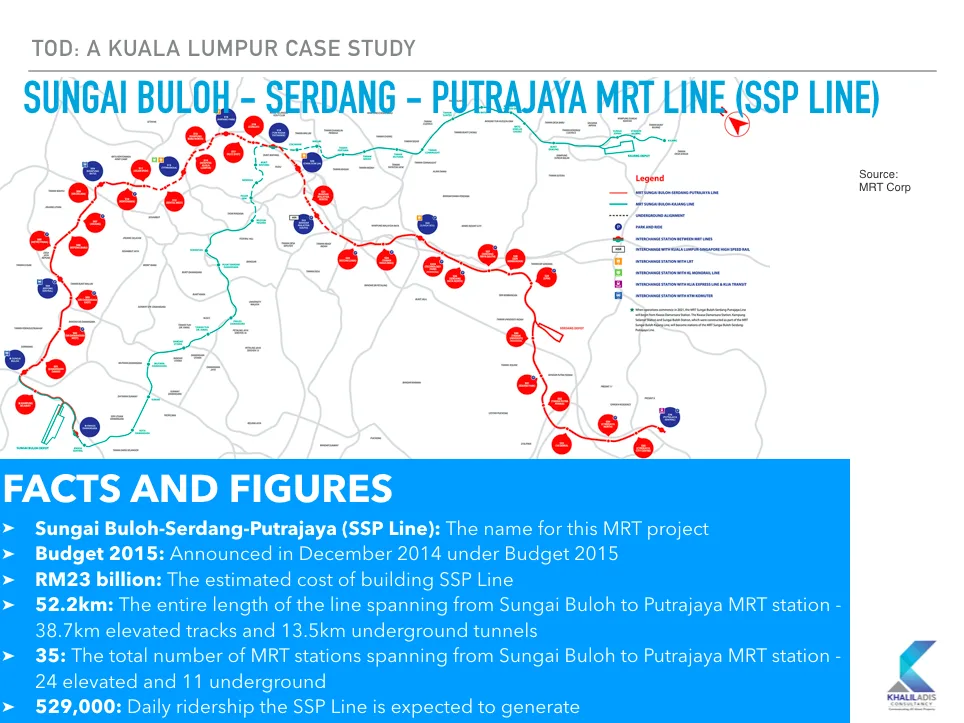

With the completion of iconic projects like the Merdeka 118 Tower and the Sungai Buloh-Serdang-Putrajaya (SSP Line) over the past three years, there are exciting opportunities in the market.

However, affordability remains a key concern for first-time homebuyers in Kuala Lumpur and Greater KL.

Data from the National Property and Information Centre (NAPIC) reveals that 48.2 per cent of the 8,226 new residential units launched in the third quarter of 2023 were priced below RM300,000.

This indicates a strong demand for affordable properties.

High-rise developments make up 67.8 per cent of these units, while 32.2 per cent are landed properties.

Selangor and Kuala Lumpur accounted for 1,062 and 1,236 units respectively.

To address these concerns and help first-time homebuyers make informed decisions, I will be covering one of the 5Cs of property buying - checking for the transport masterplan - in greater detail during my upcoming talk on July 16 at the iProperty Bumiputera Home & Property Fair 2023.

Here are five things you can expect to learn:

#1: Learn how to do map reading

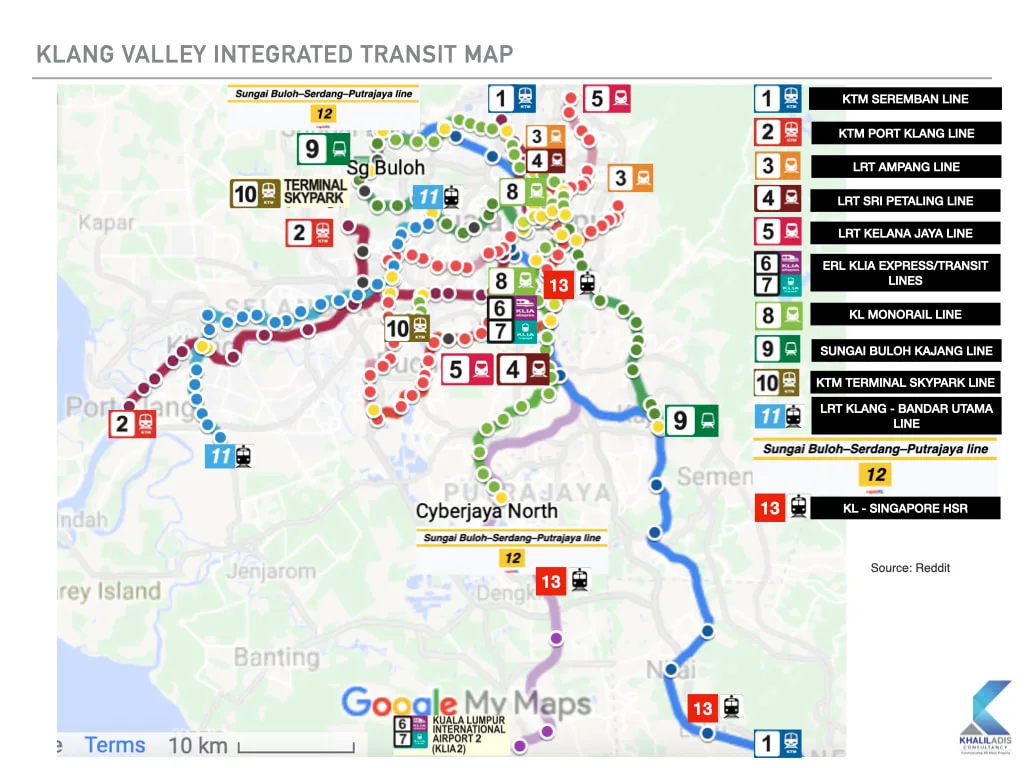

The Klang Valley Integrated Map. Source: Reddit.

In this talk, we will learn the art of map reading to understand the different train lines that serve these areas.

By gaining a grasp of the overall growth areas, we can then dive deeper into the newly completed SSP Line.

#2: Understand the transportation master plan

The Sungai Buloh -Serdang - Putrajaya MRT Line (SSP Line). Graphics: Khalil Adis Consultancy

Understanding the transportation master plan will enable you to uncover the budget allocation from the federal government.

We will analyse how this budget allocation can potentially have a positive spillover impact on properties along the line.

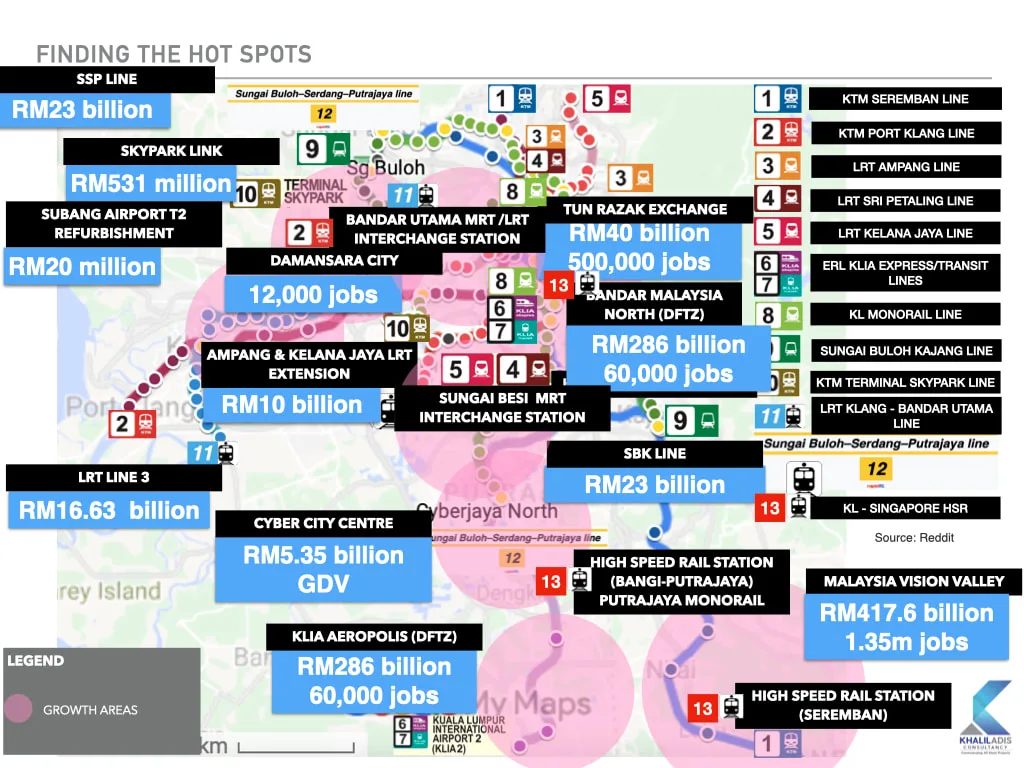

#3: Learn where the growth areas are

There are many growth areas within Klang Valley and Greater KL. Graphics: Khalil Adis Consultancy.

By studying case studies like the Cyber City Centre and the KLIA Aeropolis Digital Free Trade Zone (DFTZ), we can gain insights into the areas with promising development potential.

#4: Find the sweet spot in terms of distance to train stations

Commuters taking the LRT at Bandar Tasik Selatan LRT station. Photo: Khalil Adis Consultancy.

Additionally, developers need to adhere to certain requirements to qualify for transit-oriented development (TOD).

Learn about the sweet spots that strike the right balance and how they can impact your property's resale and rental value.

#5: Identify affordable properties along the SSP Line

One of the growth area is Cyberjaya. Photo: Khalil Adis Consultancy.

To find truly affordable properties, we need to identify areas with new or upcoming train stations and government-announced plans for upcoming economic zones.

These areas should be situated away from the city centre but close enough to train stations and dedicated hubs, ensuring long-term price appreciation.

Discover the income-to-mortgage ratio and identify areas along the SSP Line that won't burn a hole in your pocket, offering the greatest potential for capital appreciation.

iProperty Bumiputera Home & Property Fair 2023

Don't miss out on this opportunity to learn about navigating the Klang Valley and Greater KL areas, understanding the transport masterplan, identifying growth areas, finding the sweet spot in terms of distance to train stations and discovering affordable properties along the SSP Line.

See you there!

- Published on

By Khalil Adis

Cars entering Johor Causeway from Woodlands in Singapore. Photo: Khalil Adis Consultancy.

This surge in prices has prompted investors and homebuyers to search for alternatives and Malaysia has emerged as a popular choice.

However, before you pack your bags and head south, let us dive into whether Malaysia truly offers a viable solution to Singapore's escalating property prices.

The latest data from the Housing & Development Board (HDB) and the Urban Redevelopment Authority (URA) paints an intriguing picture.

The HDB Resale Price Index (RPI) and Private Property Index (PPI) for the first quarter of 2023 reached unprecedented levels of 173.6 points and 194.8 points, respectively.

These figures indicate a strong demand for properties in Singapore, driving prices to new heights.

Analysts say they are witnessing resale transactions decreasing from April to March 2023, which could explain the marginal increase in the RPI.

“In April 2023, HDB resale volumes decreased month-on-month by 4.3 per cent, following a 23.7 per cent surge in transaction activities in March,” said Luqman Hakim, chief data & analytics officer at 99.co..

But it is not just rising property prices that pose a concern.

Rental rates have also skyrocketed, leaving tenants grappling with the search for affordable accommodations.

Rising rentals

Even far-flung HDB estates such as in Jurong West are witnessing an increase in rental. Photo: Khalil Adis Consultancy.

“I am lucky that my tenants have continued to stay on despite the steep increase in rental,” said Marwani.

Her agent was the one who negotiated the lease renewal.

The private property rental market also experienced a steep climb, with a 7.2 per cent increase in the first quarter of 2023.

These exorbitant prices and soaring rentals have left many individuals, like Edward (not his real name), a tenant in Singapore, seriously considering buying a resale HDB flat as a more financially viable option.

“I signed a 2-year lease which had averted a rental hike. However, I am pretty sure it will go up next year,” said Edward who lives close to the city centre.

Edward believes that owning property might be more cost-effective in the long run, particularly with the prospect of rising rents.

“It makes more financial sense to buy now rather than rent as I foresee it will be cheaper to pay my monthly mortgage should my rent increase,” he said.

Analysts have also observed this growing trend, noting that tenants are increasingly turning to purchasing resale flats amidst high rental prices.

“Resale prices increased by 1.1 per cent compared to March 2023, with 5-room flats rising the most at 1.9 per cent. It is possible that with rent prices remaining high, many tenants are opting to buy resale flats instead. Subsequently, with the revised ABSD rates from 27 April 2023 onwards, there is expectant pressure on rental demand (and prices), prompting spillover demand from tenants as they reinvest and buy HDB resale flats,” said Hakim.

With the demand for properties in Singapore remained robust, the government has stepped in to cool the market.

The recent increase in Additional Buyers Stamp Duty (ABSD), which affects second-timer Singaporeans and first-time foreign property owners, aims to rein in property speculation.

Push factor to Malaysia?

Mega projects like Country Garden Danga Bay have seen asking prices in the secondary market selling at below launch price. Photo: Khalil Adis Consultancy.

Not quite.

Yusoff (not his real name) is among one of the few Singaporeans who is packing his bags after recently selling his 2-room HDB flat in Woodlands for slightly above $300,000.

“My wife recently passed away while my relatives are all in Malaysia. It makes sense for me to retire there,” said Yusoff.

Indeed, the first quarter data of 2023 from HDB showed that such flats were transacted at a median price of $330,000, $325,000 and $315,000 in Punggol, Sembawang and Yishun respectively.

That is almost enough to buy a private property in Malaysia where the minimum purchase price in most states is at RM1 million, including in Johor.

However, not everyone is in the same predicament as Yusoff.

Edward, for instance, is staying put.

Despite these cooling measures, the idea of buying properties across the causeway in Malaysia may not be as enticing as it seems.

“There are many push factors such as the lack of liberal values in a predominantly Muslim country. Also, Malaysia appears to be unstable both politically and economically,” said Edward.

While the affordability factor in Malaysia's property market may initially catch the eye of potential buyers, it is worth noting that property overhang for residential properties continues to be a serious issue.

Johor, for instance, continues to be the leading state for residential overhang at 5,348 units, the third quarter of 2023 data from the National Property and Information Centre (NAPIC) showed.

This would put pressure on the secondary market causing investors to suffer a loss as in the case of Country Garden Danga Bay.

Additionally, concerns surrounding political and economic stability in Malaysia may deter investors who prioritise stability and predictability in their investments.

Ultimately, while the ABSD increase may lead some investors to explore opportunities outside of Singapore, it seems that the challenges and limitations associated with investing in Malaysia may outweigh the potential benefits.

As always, conducting thorough research and seeking expert advice before making any investment decisions is crucial.

Conclusion

R&F Princess Cove is another mega project that is contributing the oversupply situation in Johor. Photo: Khalil Adis Consultancy,

The answer may not be as straightforward as it seems.

While Malaysia offers some advantages in terms of affordability, potential buyers need to carefully consider factors such as political stability and the severe oversupply issue which may impact their investment.

- Published on

While recent official visits from both Singapore’s and Malaysia’s foreign ministers will see both sides committed to completing the Johor Bahru–Singapore Rapid Transit System (RTS Link) and improve connectivity, more needs to be done to resolve its chronic property overhang.

By Khalil Adis

Buying activity is picking up in Malaysia fuelled by local buyers. Photo: Yulia.

Combined with its weakening ringgit, they have had an impact on the perceived political stability of the country and affected investors’ confidence.

While Singapore’s and Malaysia’s foreign ministers have recently reaffirmed ties and announced the completion of the Johor Bahru–Singapore Rapid Transit System (RTS Link), buying activity among Singaporeans particularly in Iskandar Malaysia remains muted.

Nevertheless, demand for the mass market housing segment will continue to be robust across Malaysia in 2023 judging by the volume of new launches for affordable homes in the third quarter of 2023, data from the National Property and Information Centre (NAPIC) showed.

According to NAPIC, of the 8,226 units launched during the quarter, 48.2 per cent (3,996 units) were priced below RM300,000 suggesting that they were geared towards local buyers.

Of this, 67.8 per cent (5,581 units) comprised high-rise development while 32.2 per cent (2,645 units) are landed properties.

Despite this, property overhang continues to be a serious issue across Malaysia that appears to have been further exacerbated by the impact of Covid-19.

From Johor to Kuala Lumpur, the number of unsold residential units has continued to remain consistently high with no sign of relief, since NAPIC started tracking the data.

Nevertheless, buying activity has rebounded strongly from 61,283 units transacted in the third quarter of 2021 to 105,204 units transacted in the same quarter in 2022, suggesting a recovery in the property market.

Of the 105,204 units transacted, 64,989 units or 61.8 per cent are in the residential sector followed by commercial and industrial at 8,570 units (8.1 per cent) and 2,213 units (2.1 per cent) respectively.

Johor

Bungalows at East Ledang in Iskandar Puteri, Johor. Photo: Khalil Adis Consultancy.

In the serviced apartment sector, Johor also had a whopping 14,780 overhang units followed by Kuala Lumpur and Selangor at 5,346 and 2,586 units respectively in the same period.

This suggests there is a severe mismatch between what buyers can afford versus what developers are offering.

In Johor, the supply glut has affected prices in the secondary market.

For example, at the peak of the market, condominium units in Iskandar Puteri, Danga Bay and Medini were launched at an average price of around RM1,000 per sq ft.

Country Garden Danga Bay, for instance, is now listed on property portals with an asking price of around RM600 per sq ft.

Over Iskandar Puteri, Teega @ Puteri Harbour was launched at around RM600 per sq ft and is now asking for around RM630 per sq ft.

Similarly, Meridin @ Medini is now asking for around RM580 per sq ft.

The only exception is Ujana which was launched at around RM250 per sq ft and is now asking for around RM450 per sq ft.

Nevertheless, the data suggest that the oversupply situation has stunted capital appreciation for residential properties.

With many good deals to be sought in the resale market, this may favour first-time homebuyers who are looking for a completed property in move-in condition.

The auction market is also another place that investors may want to look into for below-market-value (BMV) as such deals at public auctions have become ubiquitous due to the impact of Covid-19.

While such properties may offer good deals, due diligence is important as there are inherent risks involved.

Still, there are bright spots in Johor once the RTS Link is scheduled to be operational by the end of 2026, following a meeting on 16 January 2023 with Singapore's Foreign Affairs Minister Dr Vivian Balakrishnan and Malaysia’s Zambry Abdul Kadir.

Connected to the Thomson-East Coast MRT line (TEL), properties around the Bukit Chagar and JB Sentral areas may see their resale value increase due to the enhanced connectivity that will spur cross-border investment in tourism, real estate and retail industries.

Unfortunately, we are unlikely to see the resumption of the Kuala Lumpur–Singapore high-speed rail (HSR) project anytime soon.

As such, the outlook for properties around the Gerbang Nusajaya, Iskandar Puteri, and Medini as well as around the planned areas in Batu Pahat and Muar will continue to be muted.

We are also unlikely to see robust buying activities for residential properties among Singaporeans and foreign investors like those seen in 2010.

Selangor

Selangor's real estate sector will benefit immensely from the Putrajaya Line. Photo: Deva Darshan.

The second line of the Klang Valley MRT Project to be developed, full service is expected to start in January 2023.

Kwasa Damansara, in particular, will be home to transit-oriented developments (TODs) that will include affordable homes, three shopping centres and a hotel.

Spanning 64 acres and with a gross development value (GDV) of RM8 billion, the township will be served by Kwasa Damansara and Kwasa Sentral MRT stations.

Another area to watch out for is around Sierra MRT station which is developed by IOI Properties.

Located on the southernmost tip of Puchong, Sierra is poised to enjoy the economic spillover benefits from three major government projects - KLIA Aeropolis, Malaysia Vision Valley and Cyberjaya City Centre in Cyberjaya.

Speaking of Cyberjaya City Centre, Cyberjaya City Centre MRT station is a TOD project to be developed by Malaysian Resources Corp Bhd (MRCB) with a development plan spanning 20 years.

Phase one is expected to generate a gross development value (GDV) of RM5.35 billion.

It will feature a 200,000 sq ft convention centre, a 300- to 400-room business hotel, low and high-rise office buildings and a retail podium.

Kuala Lumpur

The vibrant shopping enclave of Bukit Bintang, Kuala Lumpur. Photo: Khalil Adis Consultancy.

Like Johor, the good deals are in the secondary market where their prices are significantly lower compared to new launches.

This is partly due to the 5,346 overhang units for serviced apartments in Kuala Lumpur as NAPIC’s data showed.

Nevertheless, the rental yield for such properties will likely be below 3 per cent due to the high purchase price versus their asking rent on property portals.

Investors are also likely to face a negative cash flow as the rentals will not be able to cover the mortgage.

For example, a property priced at RM880,000 will have a mortgage of RM3,609 over 30 years at an interest rate of 4.6 per cent.

With an asking price of around RM3,000 in Kuala Lumpur, this means investors will have to top up the difference in cash.

Additionally, properties along the MRT3 Circle Line will be highly sought after.

Unfortunately, developers will continue facing difficulties in off loading their high-end developments in Kuala Lumpur unless high-impact transportation project like the HSR is implemented.

Penang

A charming colonial-era building in Georgetown, Penang. Photo: Khalil Adis Consultancy.

Since the opening of the Second Penang Bridge, Batu Kawan has seen rapid developments from several renowned developers such as EcoWorld and Tropicana as well as the opening of IKEA.

While connectivity remains patchy at Batu Kawan, there is a planned Bus Rapid Transit (BRT) system for Batu Kawan as part of the Penang Transport Master Plan.

In Seberang Perai, the growth areas will be along the planned Raja Uda-Bukit Mertajam Line to connect the northwestern region to the southeastern region.

For those who can afford to buy a property on the main island, areas along the Bayan Lepas LRT line will be the new growth corridor.

However, the LRT project has been hit with a series of delays since it was announced in 2015 as part of the Penang Transport Master Plan.

Comprising 19 stations along a 22 km line, the project was supposed to begin in 2018 but has yet to begin construction due to issues of funding between the state and federal governments.

So until this political issue is resolved, we are unlikely to see the full implementation of the Penang Transport Master Plan.

Conclusion

View of downtown Kuala Lumpur. Photo: Khalil Adis Consultancy.

Against a weakening ringgit and an RM1.5 trillion national debt, improving connectivity between Singapore and Malaysia may resolve its woes, particularly in Johor.

Unfortunately, Malaysia also has a history of flip-flopping on its policies such as having a rival special economic zone in Forest City (as opposed to the one that was initially planned for Medini) and the cancellation of the HSR project.

As we speak, the Johor state government recently announced that it is exploring the possibility of ferry services between Puteri Harbour international terminal and Singapore.

However, according to local sources who were involved in the development of Puteri Harbour, this idea had been in the pipeline since 2010 but was shelved as Singapore did not see a viable need for the ferry service.

With Malaysian Prime Minister Anwar Ibrahim now in Singapore making an official visit, we could perhaps see the ferry service and HSR project being discussed.

“Connectivity, some long-standing issues, which we think are ripe for resolution, hopefully, and opportunities for the future in both the digital and green economy space. I expect it will be a very useful, significant meeting. As I said, it will set the agenda, set a timetable for the ministers and the respective ministries to follow up,” concluded Dr Balakrishnan on his recent bilateral trip to Malaysia on 17 January 2023.

In addition, Malaysia also needs to resolve its severe oversupply of residential properties by regulating the market to prevent a mismatch in demand and supply.

The government could also offer incentives to local developers to build affordable homes.

To learn from Singapore's case study, the Local Government Development Ministry is inviting experts from the Housing & Development Board (HDB).

"The ministry will examine case studies for best practices on housing policies in other countries including neighbouring countries such as Singapore that have shown success in providing the public with affordable housing,” the ministry said in a statement.

However, as land is a state issue, implementing this will be a challenge for the federal government as they do not have a central government body like Singapore’s Urban Redevelopment Authority (URA) and HDB.

Such is the case for Medini whose special economic zone was planned by the federal government and Khazanah Nasional while the one in Forest City was mooted by the state government.

- Published on

By Khalil Adis

High-end properties in the KLCC area. Photo: Khalil Adis Consultancy.

Instead, Singaporean investors flushed with cash have been busy snapping up properties in the Lion City.

Data from the Urban Redevelopment Authority (URA) showed that in the third quarter of 2021, developers sold 3,550 private residential units, compared with the 2,966 units sold in the previous quarter.

This figure does not include Executive Condominiums.

So what gives?

With COVID-19 travel restrictions, it makes sense to buy a property within Singapore.

Amid the pandemic, news of Singaporeans having their homes broken into in Johor while they were away plus other developments from across the causeway may have spooked potential investors.

From the cancellation of the Kuala Lumpur-Singapore High Speed Rail (KL-Singapore HSR) project to the revision of the Malaysia My Second Home (MM2H) policy, such news is enough to rattle investors’ confidence.

After all, if a high-level government-to-government project like the KL-Singapore HSR could be terminated, what more for those involving the private sector like housing?

Thus, it came as no surprise that despite its higher property price, buying activity has remained robust within the Lion City with record prices seen in both the HDB and private property markets.

Malaysian developers are also closely watching Singapore’s property market.

Wanting a slice of the lucrative pie, some are considering launching projects in Singapore but are unsure if Singaporeans will bite.

Singapore: Record prices call for curbs to cool the property market

While properties in Singapore are notorious for being one of the most expensive in the world, it is also seen as a safe haven for property investment due to its political stability, efficiency and transparency.

This may perhaps explain why despite COVID-19, the local property market experienced a bull run.

Data from HDB showed that the Resale Price Index (RPI) for the third quarter of 2021 is now 150.6 points - a record high so far.

This was an increase of 2.9 per cent over that in the second quarter.

Meanwhile, data from the URA, showed that prices of private residential properties increased by 1.1 per cent in the third quarter of 2021, compared with the 0.8 per cent increase in the previous quarter.

Similarly, the Private Property Index (PPI) is also at a record high.

This had prompted the government to introduce a slew of cooling measures on 15 December 2021.

Malaysia: Pandemic fatigue saw lukewarm buying activity but housing prices continued to rise

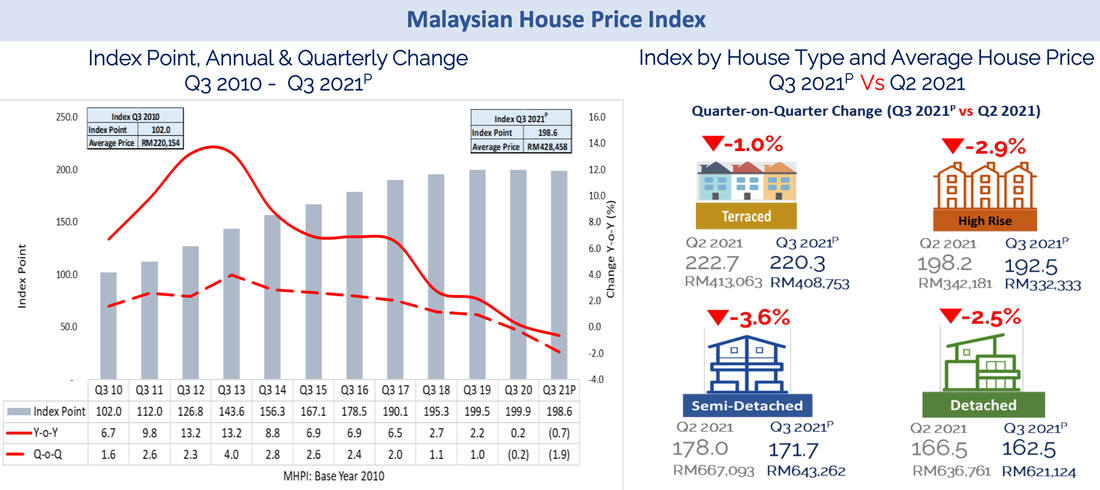

The Malaysian House Price Index. Screen grab from NAPIC.

By default, this should make Malaysia a highly sought after investment destination.

However, government data showed otherwise.

Data from the National Property and Information Centre (NAPIC) showed that the Malaysian House Price Index for the third quarter of 2021 was at 198.6 points.

On a year-on-year and quarter-on-quarter comparison, the index declined by 0.7 and 1.9 points respectively.

Meanwhile, house prices continued to increase from a median price of RM204,470 recorded in 2009 to RM428,458.42 in the third quarter of 2021.

This suggests that while the market has remained somewhat lukewarm, property prices have kept on climbing by a whopping 209.54 per cent in 12 years.

So while locals are priced out from the property market and are not buying, foreigners appear to be staying away too.

This is despite the strong Singapore dollar versus the Malaysian ringgit.

Severe oversupply of residential units in Malaysia

Developments in Medini Iskandar Malaysia, Johor. Photo: Khalil Adis Consultancy.

Of this, the majority of them (6,509 units) are located in Johor, just next to Singapore.

Nation-wide, the majority of them (10,262 units or 33.8 per cent) are priced between RM500,000 to RM1 million - a price point beyond the reach for most Malaysians.

Clearly, majority of the unsold units located in Johor are geared towards foreign buyers.

KL-Singapore HSR resumption is needed to bolster confidence

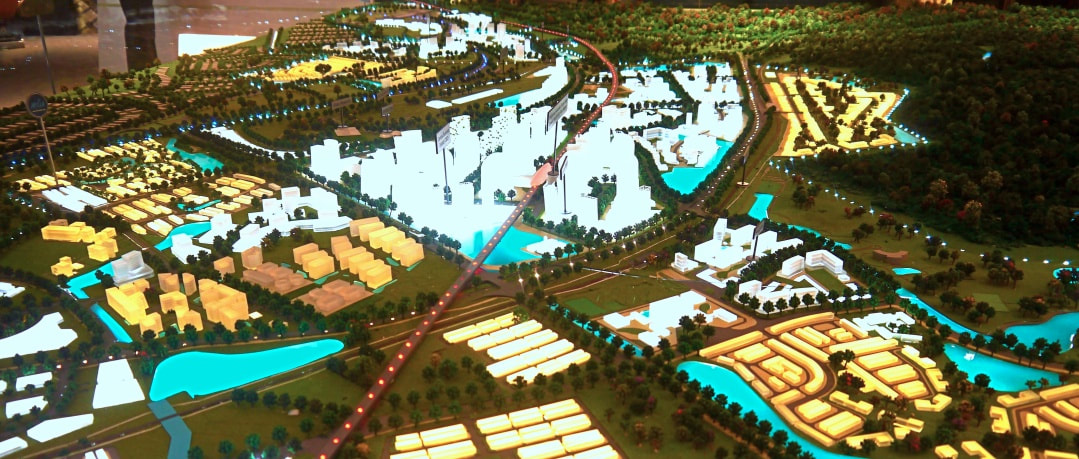

A scaled model showing the location of the HSR station in Garbing Nusajaya. Photo: Khalil Adis Consultancy.

Significantly, Malaysian Prime Minister Ismail Sabri is also suggesting reviving the terminated KL-Singapore HSR project during the launch.

As a key regional aviation hub, Singapore offers Malaysia direct access to affluent travellers and potential investors.

The Lion City also has among the highest concentration of high net worth individuals in the world.

With three stops in Johor, it seems almost impossible that the KL-Singapore HSR project could succeed without Singapore’s participation.

Look beyond local politics

View of Woodlands CIQ from Johor Bahru. Photo: Khalil Adis Consultancy.

Rather than viewing Singapore as a rival, Malaysia should see that the KL-Singapore HSR project is a win-win solution for both countries.

The spirit of good neighbourliness and gotong-royong must prevail.

After all, when Iskandar Malaysia was first mooted by former Prime Minister Abdullah Badawi, Singapore was meant to complement and not compete with Malaysia.

This is something local politicians need to be reminded of time and again.

For now, the only investors Malaysia can bank on are the permanent residents that are still holding Malaysian citizenships in Singapore

- Published on

By Khalil Adis

A Place in The Sun Live Property Exhibition held at London Olympia in 2018. Photo: Reconsult PLT.

The expo was held with a Malaysian consulting firm working together with the Tourism Ministry to attract foreign investors to buy a property and retire there.

For many British citizens wanting to escape from the cold London weather, Malaysia appears to be the ideal tropical getaway.

This is despite Malaysia being half a world away and not as well-known as Singapore.

In fact, during my various encounters with locals in London, many are surprised to learn that there are many reputable schools in Malaysia such as Marlborough College Malaysia, University of Reading and Newcastle University of Medicine, just to name a few.

Iskandar Malaysia, in particular, piqued their interest, as some had regularly attended the F1 Night Race in the Lion City.

Close to Singapore but with a relatively affordable cost of living, many had expressed interest in buying a property in Iskandar Malaysia where they have the option of living in Johor while sending their children for quality education in either Singapore or Iskandar Puteri.

Malaysia is seen as attractive due to strength of the British pound versus the ringgit, the affordable property price and one of the few places in the world where foreigners can own freehold property without any restrictions.

Sweeping changes

A Malaysian flag seen outside Berjaya Times Square. Photo: Khalil Adis Consultancy.

This has no doubt affected investor’s confidence as they try to make sense of what is going on.

With a change of government, there has also been various tweaks in policies including for the MM2H.

For example, previously, the minimum sum required for a fixed deposit was RM150,000 for those over 50 and RM300,000 for those under 50 years of age.

However, this has been increased overnight to RM1 million under the sweeping changes that were announced in August 2021.

That is almost a 600 per cent increase.

Foreigners must also prove to have liquid assets of between RM500,000 and RM1.5 million, depending on their age,

On top of that, they must have a monthly offshore income of at least RM40,000.

These policy changes are indeed tone deaf as many livelihoods have been upended since the pandemic started in 2020.

Those who have uprooted to Malaysia will have no choice but to leave the country if they cannot fulfil these new requirements.

It also reaffirms what investor’s already know - Malaysia is known for its flip-flop policy changes.

This may harm the country’s image, investors’ confidence and in turn, affect the property market.

Johor is the worst state in supply overhang

Landed terrace homes in Iskandar Puteri. Photo: Khalil Adis Consultancy.

Still, developers remained optimistic as they continue to bank on the Kuala Lumpur-Singapore High Speed Rail (KL-Singapore HSR) project.

With the project now terminated, the overhang situation in Johor will likely worsen.

According to data from the National Property Information Centre (NAPIC), as of the first quarter of 2021, Johor had the most number of unsold completed residential housing in the whole country at 6,001 units.

This was followed by Selangor and Penang at 3,679 and 4,447 units.

Most notably, homes ranging from RM500,000 to RM1 million made up the majority of the total overhang sector in Malaysia with 9,408 units (34.3 per cent) unsold worth a total of RM6.44 billion.

The serviced apartment sector in Johor fared even worse with 16,537 unsold units majority of which are within the RM500,000 to RM1 million range.

The revised policy changes for the MM2H appears to be the final nail in the coffin for the property market since many developers tie in this programme when marketing their projects overseas.

Some developers and stakeholders say the sweeping changes do not make any sense and will likely kill the property market since foreigners are likely to buy unsold homes ranging from the RM500,000 to RM1 million range.

Federal government needs to consult with stakeholders

Ominous dark clouds gathering over Legoland Theme Park. Photo: Khalil Adis Consultancy.

Figures from Iskandar Regional Development Authority (IRDA) showed that as of June 2021, Iskandar Malaysia saw the completion of investment projects worth RM7.33 billion between January to April 2021 with 20 per cent involving domestic investors and the other 80 per cent from foreign investors.

According to Datuk Ismail Ibrahim, IRDA’s chief executive, the projects that were approved to be developed in the region in 2020 included those from China, Japan and Singapore.

Overall, IRDA said Iskandar Malaysia’s total cumulative recorded investment reached RM341.4 billion since 2006 to date with 61 per cent of this has been realised.

As we speak, the Sultan of Johor had expressed his displeasure on the flip-flop in policy and requested an immediate review.

For this to be effective, the federal government needs to consult with the local authority, developers, MM2H agents, applicants and real estate agencies as they are closer to the ground.

They also need to sit down with developers and stakeholders in Iskandar Puteri and Medini as they rely heavily on foreign purchasers and investors, especially those from Singapore.

For now, the policy is doing more harm than good.

- Published on

By Khalil Adis

Scaled model of Gerbang Nusajaya showing the site of the proposed High Speed Rail station. Photo: Khalil Adis Consultancy.

On the one hand, it has deeply polarised Malaysians in what they perceive as a ‘back-door government’.

On the other hand, it has caused seasoned investors and political watchers do a double-take to decipher what is really going on.

Against a backdrop of a pandemic, reports of political infighting, defections and ongoing corruption court cases from the previous administration, Malaysia’s political landscape appears to be a fractured one.

From across the pond though, it looks like Malaysia has it all - a warm, tropical climate, rich in natural resources, a melting pot of different races and cultures and one of the very few countries where you can own freehold property.

However, a quick glance on social media shows that Malaysians are tired about the constant politicking which they feel have hindered the country’s progress.

Foreign direct investment affected by pandemic

SiLC Nusajaya located in Iskandar Puteri, Johor. Photo: Khalil Adis Consultancy.