- Published on

By Khalil Adis

#1: Ocean Financial Centre is a 43-storey Grade A office tower

Ocean Financial Centre is strategically located near to Raffles Place MRT station. Photo: Keppel Land

It is accessible via the Raffles Place MRT station.

#2: Singapore’s office market is experiencing strong rental growth

View of office towers in Singapore's downtown area. The Lion City's office market is doing well compared to the private residential and HDB markets. Photo: Khalil Adis Consultancy.

"The Singapore office market is experiencing strong rental growth. From an occupational cost and efficiency perspective it continues to be favourable vis-a-vis other comparable markets like Hong Kong,” said Mr Rushabh Desai, CEO Asia Pacific at Allianz Real Estate,.

#3: The divestment is worth S$537.3 million

Ocean Financial Centre is a Grade A office tower designed by world-renowned architectural firm, Pelli Clarke Pelli. Photo: Keppel Land

The divestment by Keppel REIT of a 20 per cent minority stake in its subsidiary, Ocean Properties LLP which holds Ocean Financial Centre, to Allianz Real Estate has an agreed property value S$537.3 million.

This is 16.8 per cent above Keppel REIT’s historical purchase price of S$460.2 million.

#4: Divestment has a target completion date by end December 2018

The Ocean Financial Centre Green Wall. Photo: Keppel Land.

Keppel REIT said the divestment is expected to be completed by end December 2018

With Allianz now holding a 20 per cent a minority stake in Keppel REIT’s subsidiary, Ocean Properties LLP, will continue to maintain a majority interest in Ocean Financial Centre through its 79.9 per cent interest in Ocean Properties LLP.

Additionally, Keppel REIT said it will continue to be the asset manager for Ocean Properties LLP in relation to Ocean Financial Centre.

#5: Unitholders of Keppel REIT set to benefit from the divestment

The divestment will see Keppel REIT realising approximately S$77.1 million of capital gains. Graphics: Shutterstock.

"The partial divestment of Ocean Financial Centre is a unique opportunity for unitholders to realise part of the capital gains from this premium Grade A office building, while maintaining exposure to the strengthening Singapore office market. Despite this being a divestment of a non-controlling stake, the agreed property value reflects the asset's quality and underlying value,” he said in a statement.

The divestment will see Keppel REIT realising approximately S$77.1 million of capital gains.

This translates to an attractive net asset-level return of 8.3 per cent per annum over the holding period.

- Published on

By Khalil Adis

Condominiums located in Tanjong Pagar. The private property market has experienced a strong rebound for the past five quarters. Photo: Khalil Adis Consultancy.

Figures from the Urban Redevelopment Authority (URA) showed that the Lion City's PPI surged by 11.0 points from 138.7 in the fourth quarter of 2017 to 149.7 points in the third quarter of 2018.

However, the market softened from July onwards post the new property cooling measures.

Here are the top five property market roundups for 2018 and our top five outlooks for 2019.

Roundups:

#1: En-bloc fever

Old estates in Singapore tend to go under en-bloc as part of the city's rejuvenation. Photo: Khalil Adis Consultancy.

They included the iconic Pearl Bank Apartments which was sold for S$728 million sales to CapitaLand and Park West which was sold for S$840.89 million to SingHaiyi Gold Pte Ltd.

Data from Cushman & Wakefield Inc showed that the collective sales market recorded S$3.8 billion of en-bloc transactions in the second quarter.

#2: New property cooling measures introduced

This included increasing the Additional Buyer's Stamp Duty (ABSD) rates and tightening loan-to-value (LTV) limits on residential property purchases.

The new ABSD rates and LTV limits are as above.

As a result, the collective sales market declined with S$353 million worth of transactions recorded in the third quarter, data from Cushman & Wakefield Inc showed.

#3: Industrial property market picks up steam

View of the Tanjong Pagar Container Terminal and the industrial properties surrounding it. The industrial property market has seen in increase in investment this year. Photo: Khalil Adis Consultancy.

According to data from Cushman & Wakefield Inc, industrial property deals soared 73 per cent to S$1.2 billion in the third quarter while office sales increased by 54 per cent to S$2.1 billion.

Meanwhile, Jones Lang Lasalle Singapore, citing data from JTC statistics said islandwide all-industrial rental correction stayed modest at 0.1 per cent quarter-on-quarter for three consecutive quarters since the fourth quarter of 2017, while the second quarter of 2018 all-industrial price index flat-lined for the first time since trending down in the third quarter of 2014.

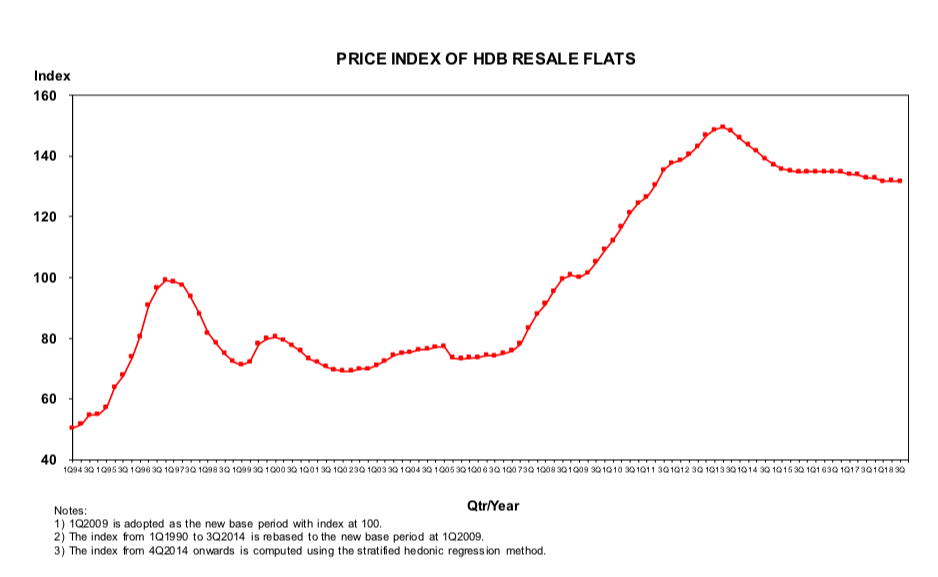

#4: HDB resale values are declining

Screen grab of the HDB Resale Price Index courtesy of the Housing & Development Board (HDB).

Public interest in HDB dominated the headlines in 2018 as government officials warned that their values could decline, especially those that are more than 40 years with around 50 years left on their 99-year lease.

This marked a stark contrast during Lee Kuan Yew's era when he assured Singaporeans that HDB flats are an asset.

Property agents who specialise in HDB flats in mature estates such as Toa Payoh say they are already seeing prices of older resale flats declining as many buyers are staying clear from such properties following the ongoing debate.

For example, according to the third quarter data from the HDB in 2018, a 3-bedroom flat in the estate was transacted for S$279, 000.

In contrast, the median price during the same period in 2016 was transacted for S$300,000.

Having said that, other factors do come into play such as the supply of new Built-to-Order (BTO) flats which has influenced the resale price.

However, until the government addresses the uncertainty surrounding older estates, we are likely to see the values declining as it is very much influenced by market sentiment.

#5: Widening price gap between a private property and an HDB flat

View of an HDB flat in downtown Singapore surrounded by towering condominiums and commercial buildings. Photo: Khalil Adis Consultancy.

According to data from the HDB, the RPI has been on a decline since the second quarter of 2013 as it continues to launch BTO flats in the market.

This is the biggest price gap in over 10 years and will likely be a contentious issue when the general election is expected to be called in 2019.

Predictions:

#1: HDB to become a hot-button issue

HDB flats located in the mature estate of Toa Payoh. Photo: Khalil Adis Consultancy.

As such, HDB will be a hot-button issue as 80 per cent of the population lives in HDB flats.

As we have discussed above, HDB resale prices are already on the decline while the price gap between a private property and an HDB flat has widened considerably.

The government will need to address the ongoing debate on the value of older HDB flats moving forward.

#2: Fewer BTO flats to be launched

A Built-To-Order (BTO) flat being built in the Matilda district in Punggol. Photo: Khalil Adis Consultancy.

This comprises 3,802 BTO units and 3,412 SBF units across various towns estates such as Sembawang, Sengkang, Tengah, Yishun and Tampines.

However, there will be fewer units being offered in the next BTO launch exercise in February 2019.

The HDB said it will offer about 3,100 flats in Jurong West, Kallang Whampoa and Sengkang.

#3: A sellers' market

An HDB flat located in Taman Jurong. Fewer BTO flats in the market could push buyers to buy resale HDB flats instead. Photo: Khalil Adis Consultancy.

As such 2019 could likely be a sellers' market.

Sellers should watch the market closely while buyers should opt for a BTO quickly.

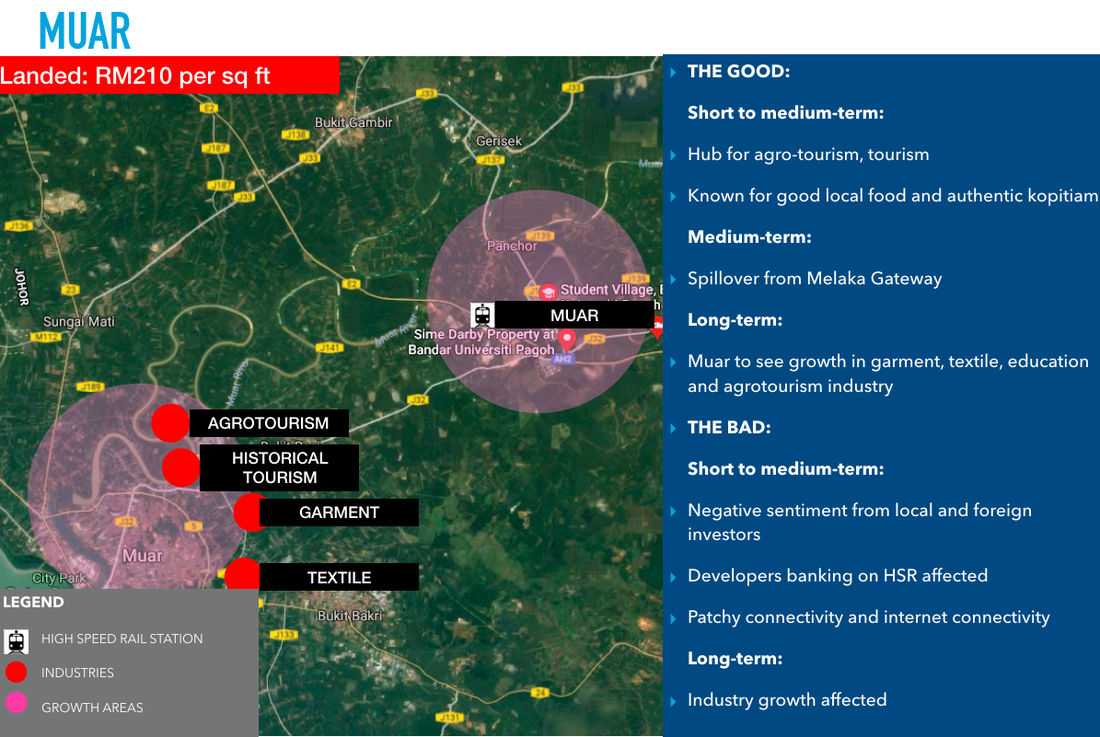

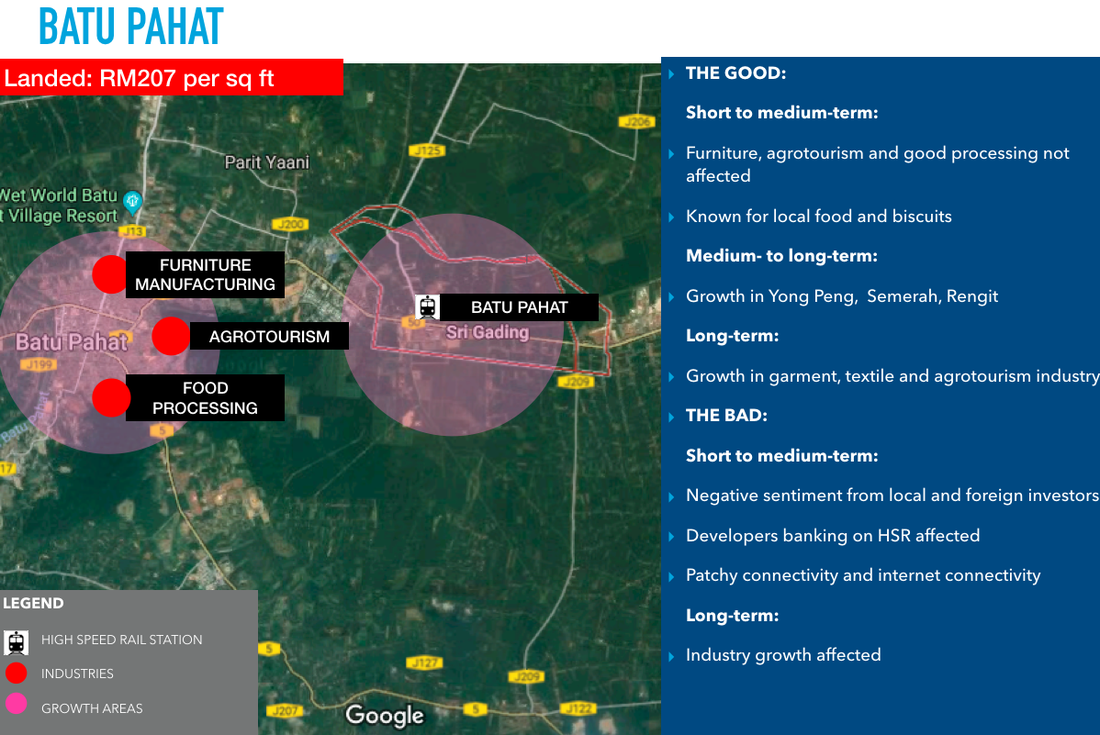

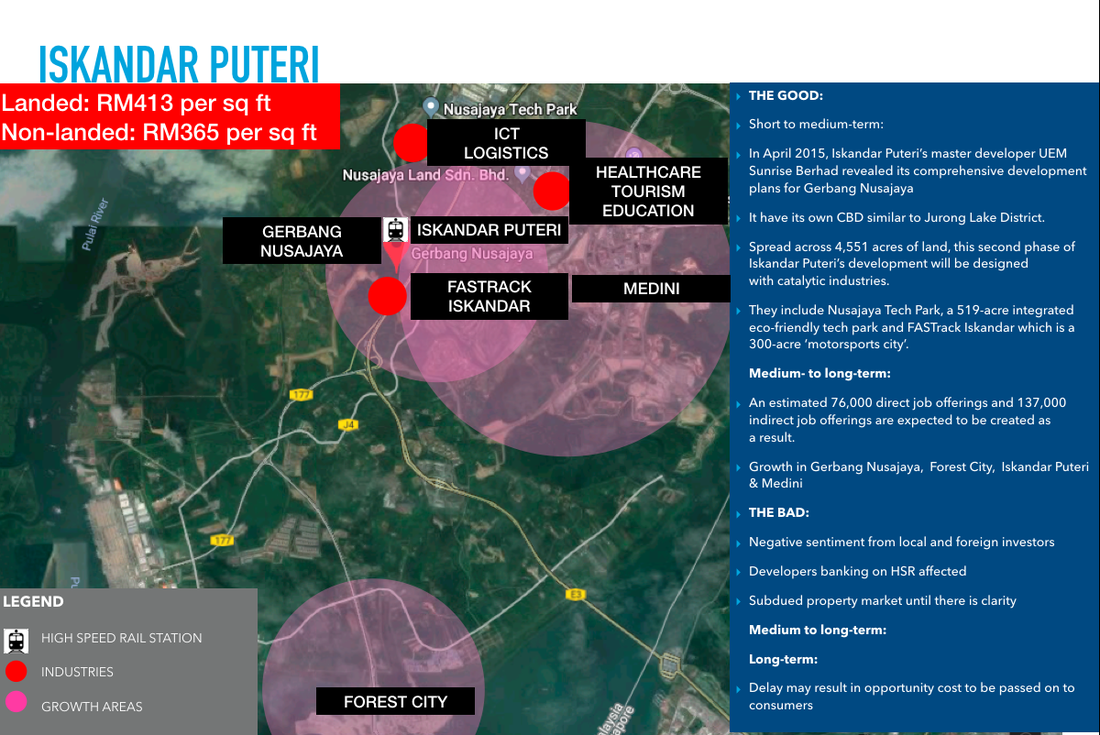

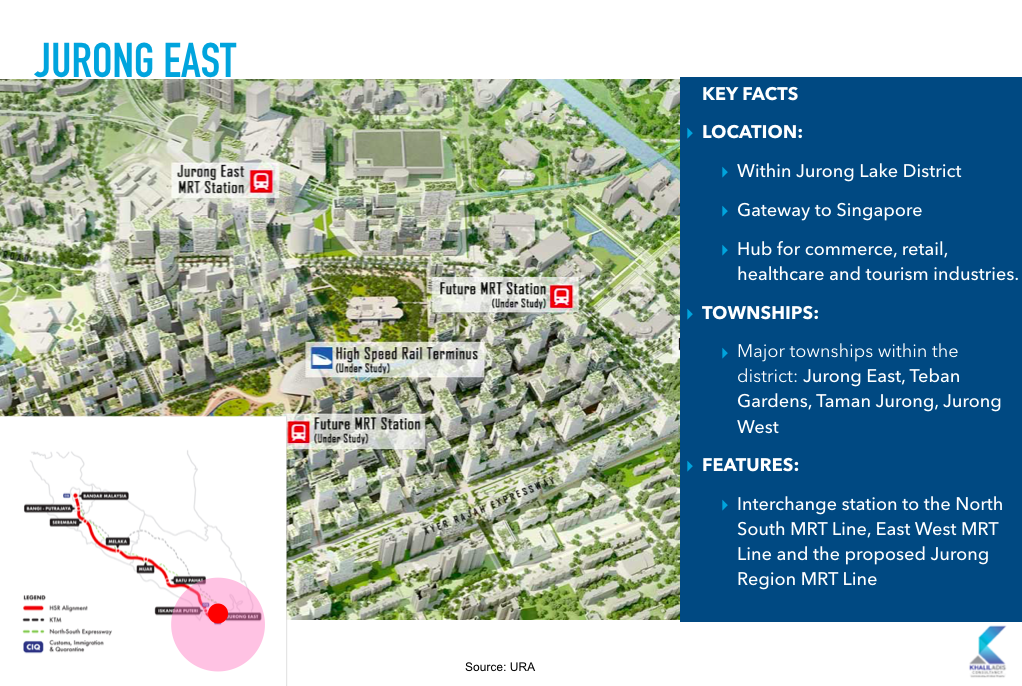

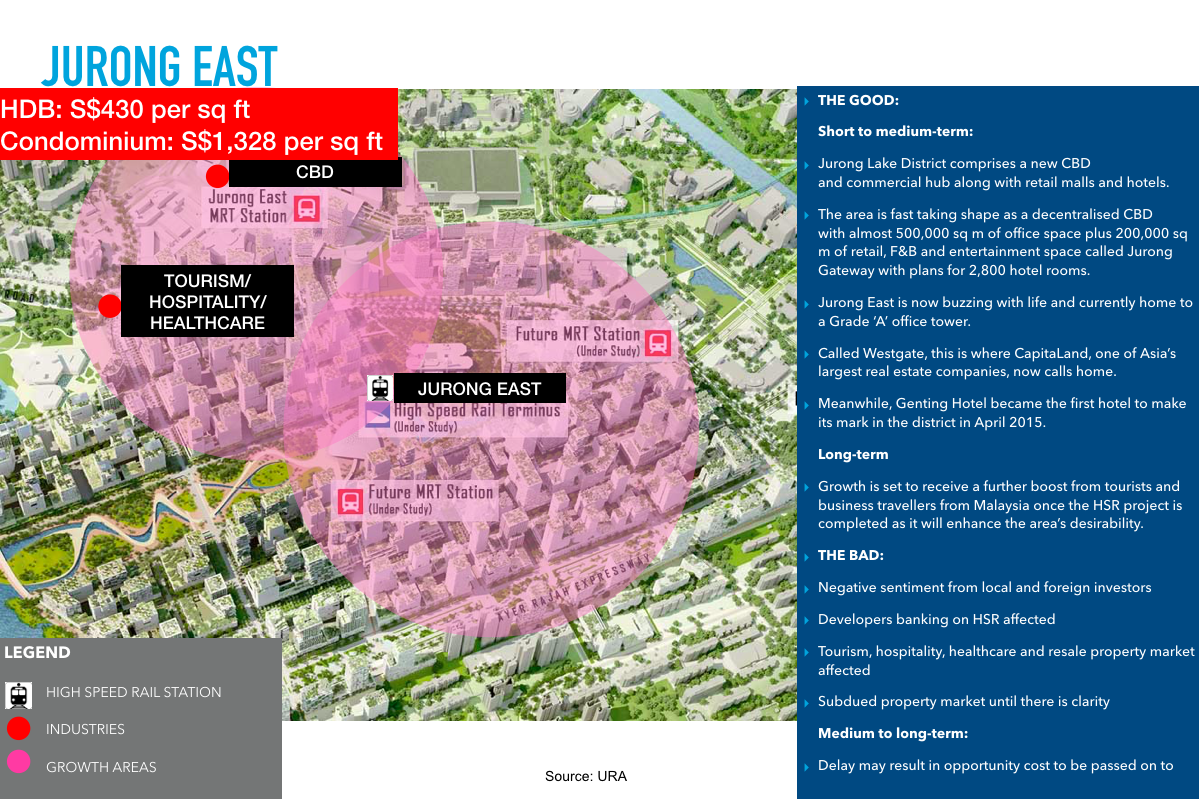

#4: Five growth areas

Scale model of the URA Draft Master Plan 2014 showing Woodlands Regional Centre at the URA Building. Photo: Khalil Adis Consultancy.

Woodlands Regional Centre will be a transportation hub which will connect the Thomson-East Coast Line (TEL) to the Johor-Singapore Rapid Transit System (RTS) via Woodlands North MRT station.

Meanwhile, Jurong Lake District will house the High Speed Rail station linking Singapore to Kuala Lumpur in 90 minutes flat.

The development of the project has been postponed to two years and will now commence construction in 2020 instead of 2018.

Meanwhile, the express service will only commence by 1 January 2031 instead of 31 December 2026, as originally planned.

You can read more about URA Master Plan 2014 here.

#5: Opening of TEL will provide a price booster for properties along the line

Construction of the Woodlands North MRT station next to Republic Polytechnic. Photo: Khalil Adis Consultancy.

It will link to the East-West Line, North-South Line, North-East Line, Circle Line and the Downtown Line.

Spanning from Woodlands North to Sungei Bedok, the line will be opened in stages next year.

Stage one will comprise stations from Woodlands North to Woodlands South.

As such, properties in the Woodland Regional Centre as highlighted above will be among the first to enjoy the price booster when the stations commence service next year.

This will definitely be much to cheer about in the north amid the muted HDB resale market.

- Published on

By Khalil Adis

Our former home in Taman Jurong where my mom and I used to live. Photo: Khalil Adis Consultancy

This psychological horror drama thriller film tells a story of how a mom and her two daughters were ambushed in their home by murderous intruders.

One of her daughters, Beth, conjured up a dream while being physically abused by her sadistic captors in a bid to escape her trauma.

Still being held captive by the intruders, she would go on to write a bestselling book of the same title in the imaginary world that she had created.

For me, however, the abuse that my mom and I had encountered was not a work of fiction.

As a way to deal with it, I wrote a book called Property Buying for Gen Y which would then go on to become a bestseller and was a turning point in my career.

While my story is nothing like Incident in a Ghostland, the physical, psychological and emotional scars still remain until today.

History of abuse

A police patrol car in Taman Jurong. The abuse was so bad we had to lodge a police report. Photo: Khalil Adis Consultancy

My parents had divorced and as a result, we were living with our guardians.

My mom and I lived with an uncle while the other family member, was sent to live with another uncle, owing to her very difficult behaviour.

We then got a flat together in Taman Jurong where I was living my mom and this other family member when I was around 18-years-old.

I remember thinking - “Finally! We have a place to call our own.”

However, little did I know this family member would turn out to become a monster.

The first instance of abuse occurred when I was kicked out of home at 21-years-old.

I recall having my bag thrown out of the house and living temporarily at the police station where I was posted at for my national service.

Back then, I did not know any property laws and did not know any better.

I then rented a place for a while near to Admiralty MRT station.

To pay for my rent, I would give tuition.

The subsequent abuse happened in 2014 when the family member came back with her family after having lived overseas.

My mom and I were on the constant receiving end of abuse, bullying and threats to kick us out of our family home.

Mind you, I was paying for the mortgage and taking care of my mom.

Things got so bad that my mom and I had to lodge a police report and sought help from my MP Tharman Shanmugaratnam.

Thankfully, I now have my own home and a safe place for my mom and I away from the abuser.

I subsequently dedicated Property Buying for Gen Y to my MP.

Complications of joint tenancy

A joint tenancy agreement can lead to a sink or swim situation for property owners. Photo: Shutterstock

This is especially so if the property is held jointly as in the case of my mom and this family member.

Under a joint tenancy agreement, two individuals agree to jointly hold a property.

While this is the most common method of ownership as it is less costly, a joint tenancy exposes one family member to the financial risks, liabilities and other problems created by the other family member.

In my case, since moving to another country, this family member has not been paying for her mortgage since 2011.

My uncle had intervened with the agreement that I pay for the mortgage until I got my own home.

However, once I received the keys to my home, the other family member became uncontactable.

The HDB subsequently contacted us and told us this family member cannot pay for the house and wants my mom to take over the mortgage.

As a result, my mom now bears the burden.

We then decided to put up the home for rental as my mom is not working and is ill.

The rental income is now helping to cover the mortgage as well as for my mom’s savings.

We also paid the other family member her portion less expenses.

However, the constant threats from the abuser still remain.

If you are among the unlucky few who happen to own a property jointly with a toxic family member, this is what you should do.

#1: Have proper documentation

Ensure you have all your documents in black and white so it can be tendered as evidence in court. Photo: Shutterstock

Therefore, you need to have proper documentation in case it does end up in court.

This includes whatever payments that you have been paying for the upkeep of the home, property tax and so on.

Other useful documents including emails detailing a pattern of abuse, police reports and other documents to show that the other party has not been paying their home mortgage.

Having all these documents will help bolster your case should it end up in court.

#2: Speak to a lawyer

This can be very problematic when you are dealing with a family member who has not been paying and is abusive.

Speak to a lawyer on what your options are so that you are fully prepared should a death occur in your family.

#3: Do not react

Instead of reacting, choose how to respond to the situation in a tactful manner. Image: www.keepcalm-o-matic.co.uk

While it can be very difficult to not react when the other person is shouting and accusing, you need to realise that the other person is not acting rationally

By not reacting, you have taken away their power to push your buttons.

Stay cool and take the high road all the way.

#4: Minimise contact

Focus only on the points concerning the house and steer clear from any arguments.

Do not get sucked into the drama.

#5: Learn to forgive

The lotus flower symbolises love, courage and the practice compassion. Photo: Khalil Adis Consultancy

When I speak about forgiveness, it is not for the other person but more for yourself.

By learning to forgive, the other person no longer holds any power on you.

I remember how empowering it was when I moved to my own home as the other family member now can no longer bully my mom and I.

You have the right to be treated with respect, to be safe and to have a wonderful life away from the abuser.

Seek help

The Ministry of Social and Family Development have various branches in Singapore. Photo: Khalil Adis Consultancy.

My mom and I have experienced some of those forms of abuse described.

While it is hard to believe that your own flesh and blood can turn their back against you, family violence is very real.

In closing, it is my hope by sharing this cautionary tale that others in a similar situation will be spared the agony of what my mom and I have had to endure.

If you have a family member who is abusive or know a family who is being abused, do not hesitate to call the authorities. You can find out more at Break The Silence.

- Published on

Pinnacle @Duxton is an HDB project that was mooted by the late Lee Kuan Yew. It is located in downtown Singapore. Photo: Khalil Adis Consultancy

Ask any young Malaysians and chances are many are still unsure if they can buy their first home.

Their lack of knowledge, financial literacy, inability to get a loan and the lack of supply of such homes across Malaysia are further exacerbating the Malaysian housing issue.

From Johor to Kuala Lumpur, there is currently a demand-supply mismatch whereby most new launches in the market are priced above RM500,000.

This is far beyond what the average Malaysian can afford.

According to the first quarter of 2018 data from the National Property and Information Centre (NAPIC), Selangor has the highest number of existing stock of residential units followed by Johor and Kuala Lumpur at 1,516,960, 795,363 and 471,475 units respectively.

With Budget 2019 to be announced in November, perhaps the Malaysian government can take a cue from Singapore how the city-state is able to house 80 per cent of its population.

Step 1: Have a single affordable housing agency

The Singapore government's housing agency's The HDB Hub is located at Toa Payoh. Photo: Khalil Adis Consultancy

In comparison, in Malaysia, there are so many affordable housing programmes being rolled out by the state and federal governments such as Rumah Milik Mampu, Rumah Selangorku, PR1MA, My First Home, Program Perumaha Rakyat and the list goes on.

This confuses the public.

The government should consolidate the affordable housing segment under one single government agency much like the HDB model.

Recently, Zuraida Kamaruddin, the Minister of Housing and Local Government, was in Singapore to study the HDB model.

By having it under one government agency umbrella, this will enable the federal government to better gauge demand from the public.

This leads to the next point.

Step 2: Build demand-driven homes

Applicants who have successfully balloted for their flats are then invited to choose their units at the HDB Hub. Photo: Khalil Adis Consultancy

The public is then invited to apply for the various homes that are on offer in different parts of Singapore.

By doing so, this enables the HDB to gauge demand from the public and allocate homes using a balloting system.

The balloting system will then inform applicants of the status of their application.

If Malaysia were to follow such a system, this will help to solve the current demand-supply mismatch in the market and build homes according to demand.

Step 3: Introduce grants and subsidies

Singapore's Central Provident Fund (CPF) operates very much like Malaysia's EPF where there are various schemes for housing applicants to enjoy subsidies. Photo: Khalil Adis Consultancy

To qualify for the AHG, applicants must apply for a 2-room flat or larger with an income ceiling of S$5,000 per month,

Applicants must also be employed at the time of application and be at least in employment for the past one year during the housing application.

On top of that applicants must not be an owner of any other properties in Singapore or overseas.

Applicants can also qualify for additional grants under the SHG here or if they live close to their parents.

By introducing such grants, it lowers the entry price to buy a home.

Likewise, if similar grants are introduced in Malaysia, it will mean more Malaysians can afford to buy their first home.

You can read more about the scheme here:

Think about it.

Step 4: Introduce housing loans direct from the housing ministry

Singaporeans viewing the masterplan for an upcoming HDB township called Tengah. In Singapore, its citizens can get a housing loan direct from the HDB. Photo: Khalil Adis Consultancy

This means, regardless of the economy, the interest rate will remain the same unlike taking a bank loan.

In addition, the HDB is more compassionate if say, one is unable to service their loans.

The HDB will still require you to pay your monthly mortgage but will work out a plan that will ensure you will still have a roof over your head.

However, banks are less forgiving when you take a bank loan and will not hesitate to repossess your flat if you do not pay your mortgages on time.

In Malaysia, applicants must apply for a bank loan.

However, due to non-payment of PTPTN as well as bad credit, some applicants find their loans being rejected.

Perhaps, a way to get around it is to have a housing loan disbursed by the housing ministry with its own set of rules similar to the HDB.

Step 5: Introduce a rent-to-own scheme (for those who can't afford downpayment)

Ayer Holdings, formerly known as TAHPS Group, has introduced the ‘Stay & Own' scheme for their Epic Residence and Foreston projects to help first time home buyers. Photo: Khalil Adis Consultancy

For example, Ayer Holding introduced a ‘Stay & Own' scheme for their Epic Residence and Foreston projects whereby part of the rent will be converted to the downpayment.

This not only provides a temporary solution for those who urgently need a home but also a form of security

You can read more about the scheme here:

- Published on

By Khalil Adis

GSK Asia House headquarters for Asia located at 23 Rochester Park, Singapore. Photo: GSK Asia

“At GSK, we often ask ourselves, “do we have the right properties?” In Asia, it is all about growth. Asia is a huge piece of our future,” said Simon French, GSK’s Workplace and Design Director, Worldwide Real Estate and Facilities, United Kingdom.

French was speaking at the CoreNet Global Summit 2018 held in Singapore in March.

Titled Beyond the Horizon – The 2030 Workplace, GSK’s Asia headquarter office at Singapore’s research & development hub at one-north features intuitive workspaces that promote human interaction and collaboration while being culturally sensitive.

For example, its food offerrings at the premises are halal, keeping in mind the city-state’s multi-racial and multi-religious society. “Bacon & eggs won’t work in Singapore,” quips French.

The design process behind its GSK Asia House at Rochester Park in one-north involves looking at commercial drivers, behaviours & culture and design thinking

What results is an open office space spanning four floors of 14,330 sq m with plenty of natural light and ventilation.

In addition, it also has four layers of invisible security barriers before you get to see the actual work space.

Indeed, the ground floor is open to the public while the entire building is designed to bring in natural light.

“In Singapore, outdoor areas are under- utilised. We, therefore, have used the outdoor space in the western part of the building as

it affects employees’ behaviour - happy staff equals a more engaged people,” says French.

Commerce and value creators

GSK Asia House has been designed with plenty of light and natural ventilation. Photo: GSK Asia

GSK estimates that the Asia Pacific region will become its largest regional market by 2020. As such, greater emphasis has been placed on those who bring value or are generating revenue.

“We call this smart working where no leaders and directors have an office. It is about transparency, being able to see leaders and seeing them working. Constant sharing of ideas is relevant to the scientific industry,” explains French.

To make the workspace conducive to allowing open communication, seeing different perspectives and the exchanging of ideas, GSK Asia has created ‘neighbourhoods’ where there are no specific desks for anyone.

“There are no specific desks for anyone with fluid sitting areas and workspaces. This means you can work anywhere while promoting the exchange of ideas,” notes French.

Even the ground floor, which is not considered GSK’s working space, has created revenue.

“By having a concierge, we realised ownership of open space increases quickly. As such, Google is using the space and leasing from us,” reveals French.

GSK Asia features flexible, open spaces to encourage collaboration and the exchange of ideas. Photo: GSK Asia

“We are in the process of developing this whereby your laptop is recognised, and your presentation will automatically come out. In short, the building knows who you are,” he declares.

A record 740 corporate real estate professionals attended the CoreNet Global Summit 2018 which features more than 40 thought leaders shedding light on the critical relationship between an organisation’s productivity, bottom line, and effective CRE management.

The two-day summit revolved around nascent and current developments such as geopolitical shifts and technological disruption, which have complicated decision-making in many organisations across the Asia Pacific.

This story was first published by Asian Property Review in its July-August 2018 issue

- Published on

#1: Impact:

Infographic: Khalil Adis Consultancy

#2: Impact:

#3: Impact

#4: Impact

#5: Impact

#6: Impact

#7: Impact

#8: Impact

#9: Impact

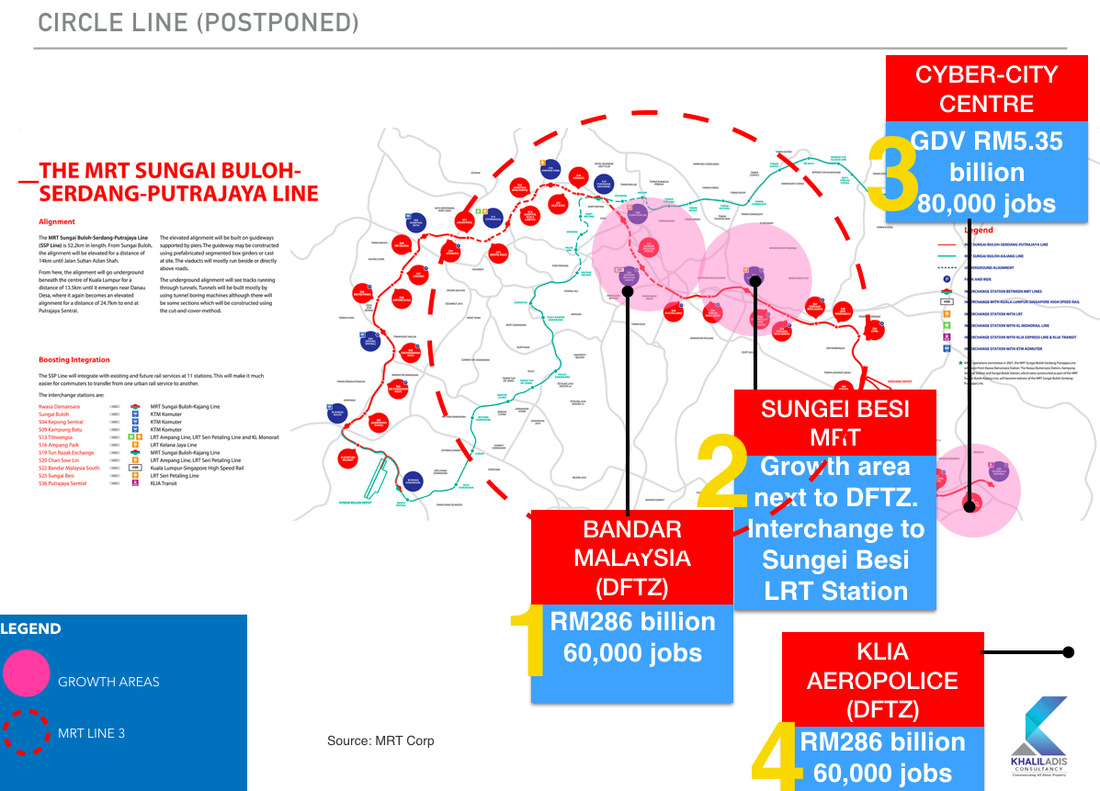

The impact for this postponement will be marginal as this MRT Line will still need to be constructed to connect the SBK Line and SSP Line.

We will most likely see speculators staying away from the market.

This presents good opportunity for genuine homebuyers to start looking in and around the station.

Homes in the secondary market will be the most ideal as they are priced cheaper than new launches.

- Published on

DUO, a joint-venture project between the Singapore and Malaysian government located in the Outside Central Region (OCR). Photo: Khalil Adis Consultancy

By Khalil Adis

The Urban Redevelopment Authority’s (URA) flash estimate of the price index for private residential property for the second quarter of 2018 showed that Singapore’s private property index has increased 4.9 points from 144.1 points in the first quarter 2018 to 149.0 points in the second quarter.

This represents an increase of 3.4 per cent, compared to the 3.9 per cent increase in the previous quarter.

URA’a data showed that private properties in the Rest of Central Region (RCR) increased the most in Singapore - by 5.7 per cent, after registering an increase of 1.2 per cent in the previous quarter.

Meanwhile, those in the Core Central Region (CCR) increased by 1.4 per cent compared to the 5.5 per cent increase while those in the Outside Central Region (OCR) increased by 2.9 per cent after registering a 5.6 per cent increase in the previous quarter respectively.

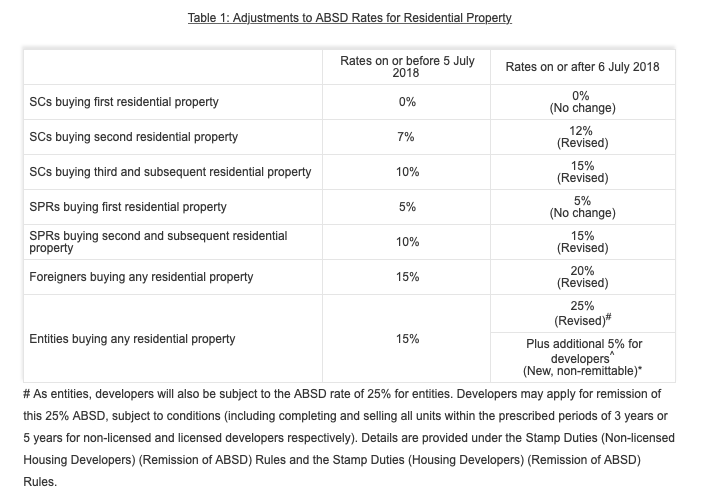

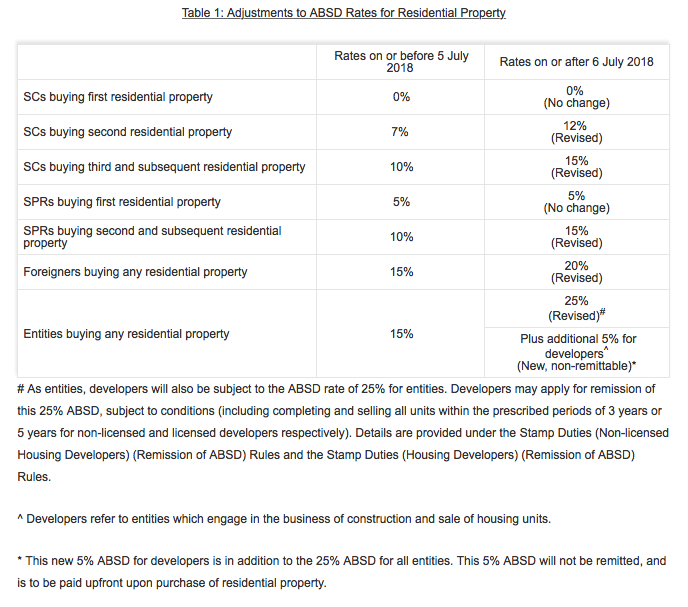

The Monetary Authority of Singapore (MAS) in a statement said the adjustments to the Additional Buyer’s Stamp Duty (ABSD) rates and Loan-to-Value (LTV) limits on residential property purchases were needed “to cool the property market and keep price increases in line with economic fundamentals.”

Additional, MAS said private residential prices have increased sharply by 9.1 per cent over the past year after declining gradually for close to four years.

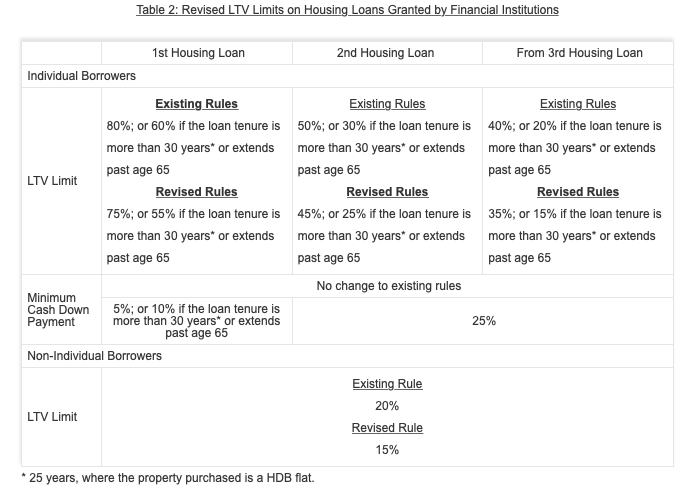

See table below for the summary:

#1: First time Singaporean private home buyers can heave a sigh of relief

The ABSD measures are aimed at second and multiple property owners to ensure they do not engage in excessive speculation which may bring property prices to unsustainable levels.

Therefore, first time private home buyers will not be penalised as they are deemed as genuine homeowners.

#2: However, bank loan margins for first-timers has been decreased

Be prepared to cough up more cash upfront.

The loan-to-value limit has been decreased from 80 per cent or 60 per cent if the loan tenure is more than 30 years or extends to more than age 65 to 75 per cent or 55 per cent if the loan tenure is more than 30 years or extends to more than age 65.

This means you will need to pay 5 per cent in cash upfront if your loan tenure is 30 years or 10 per cent if it extends to more than age 65. While the remaining will need to be paid in cash and/or CPF.

#3: Be prepared to pay an additional 5 per cent ABSD for second and/or subsequent properties for Singaporeans

ABSD rate for second property has been increased from 7 to 12 per cent.

Meanwhile, the ABSD rate for third and subsequent properties has been increased from 10 to 15 per cent.

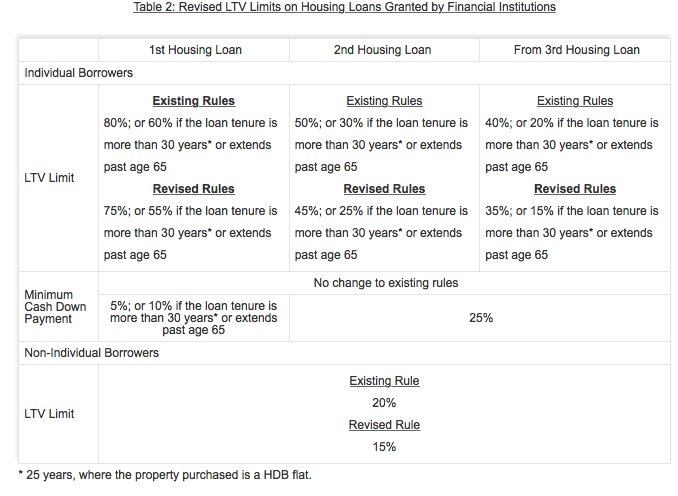

#4: Lower LTV ratio for a second property

The loan-to-value limit has been decreased from 50 per cent or 30 per cent if the loan tenure is more than 30 years or extends to more than age 65 to 45 per cent or 25 per cent if the loan tenure is more than 30 years or extends to more than age 65.

The minimum cash downpayment is now 25 per cent.

#5: More cash upfront makes buying in Iskandar Malaysia more attractive

You get more bang for your bucks investing in Iskandar Malaysia than in Singapore with the new ABSD rates.

Assuming you are buying a second property for your own occupation, that 25 per cent cash downpayment for an S$1 million condominium translates to S$250,000 which could easily buy you a freehold landed or condominium development across the causeway.

With a minimum purchase price of RM1 million and a 70 per cent loan margin, you might as well convert it to your RM300,000 downpayment, not including stamp duty, state levy, legal fees and so on.

The downside is you will have to make to with the daily commute and traffic congestions until the Johor-Singapore Rapid Transit System (RTS) is ready in 2024.